Global Chloroform Market Size, Strategic Product End-Uses, and Global Industry Forecast [2026–2034]

Other |

2026-06-11 12:20:41

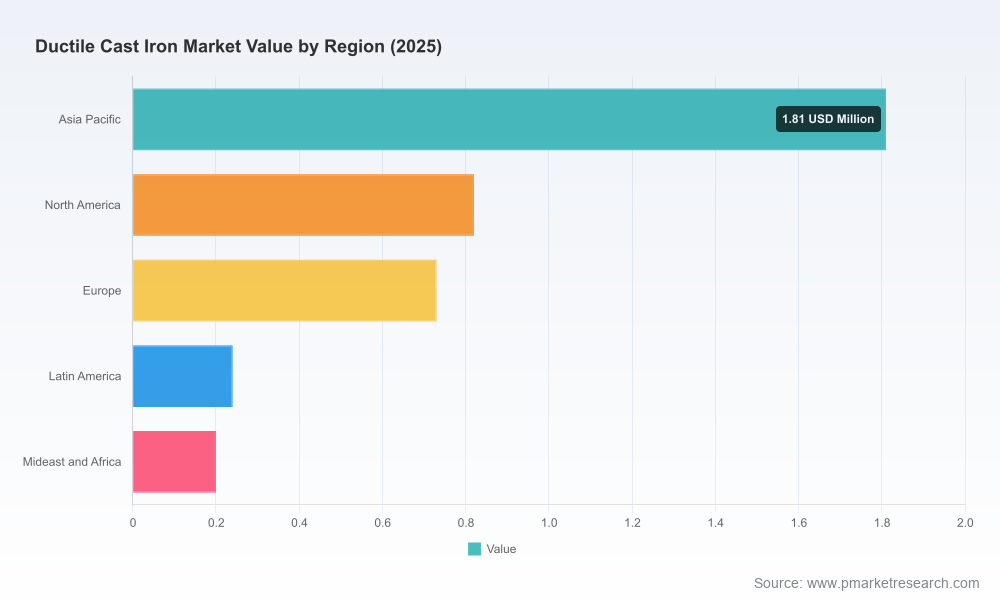

The global ductile cast iron market is entering a phase of measured expansion and structural transition. Our base-year analysis (2025) places the market size at USD 3.8 Million (revenue unit: Million), with a compounded annual growth rate (CAGR) of 5.4% projected over the 2026–2032 forecast window. This introduction distills the strategic implications of those macro trajectories and explains why the full PW Consulting study should be on every executive desk planning capital allocation, supply-chain resilience, or product strategy for 2026.

Ductile Cast Iron Market

From CapEx timing to supplier selection, manufacturing and infrastructure firms will need high-confidence signals about demand durability and margin pressures. The market’s steady mid-single-digit growth requires different strategic choices than a volatile boom—decisions that hinge on understanding supply elasticity, regulatory compliance costs, and the pace of technology-driven efficiency gains.

Ductile Cast Iron Market

Procurement and operations teams must reconcile rising input cost volatility with sustainability targets. The industry’s transition pathways—electrification of melting processes, energy efficiency retrofits, and circular-material strategies—have multi-year paybacks and regulatory tailwinds. Our report quantifies scenarios and break-even boundaries for those investments.

Ductile Cast Iron Market

For M&A and corporate development, the combination of moderate growth and fragmented manufacturing footprints creates selective consolidation opportunities. The study maps where scale captures are most accretive and where bolt-on capabilities (e.g., hydraulics castings, waterworks fittings) unlock cross-selling potential.

Across the 2020–2025 historical window we tracked recovery and stabilization after supply chain shocks and demand swings. With a base of USD 3.8 Million in 2025 and the 5.4% CAGR through 2032, the sector is poised for steady expansion rather than breakout growth. That profile favors operational optimization, targeted capacity investments, and disciplined product innovation over broad speculative expansion.

Infrastructure renewal continues to be a bedrock demand engine. Municipal water and wastewater projects, network rehabilitation, and resilience investments underpin sustained volumes of ductile pipe and fittings.

Industrial equipment and heavy machinery demand remains cyclical but anchored by replacement cycles and performance requirements where ductile cast iron’s mechanical properties are preferred (wear resistance, tensile strength, fatigue life).

Automotive applications face a dual dynamic: electrification changes component architectures, yet structural and load-bearing applications continue to value ferrous castings. The net effect is nuance by subcomponent—an area the full report models with scenario-based volumetrics.

Specialized sectors (construction, oil & gas) provide episodic upside tied to project pipelines and commodity cycles. Understanding the correlation of ductile cast iron demand to these upstream cycles is essential for capacity planning and working-capital management.

Foundry capacity and melting technology choices will shape cost curves and CO2 intensity for the next decade. We document real-world capital projects that signal strategic direction—most notably investments to replace traditional cupola furnaces with electric induction technology that simultaneously increase melt capacity and reduce emissions intensity. For manufacturing executives, these projects illustrate the economic logic and regulatory read-across that justify electrification investments.

Raw material and alloy feedstock volatility remains an operational risk. Recent industry signals show upward pressure on pig iron and grey cast iron inputs as foundry demand normalizes in some regions. Procurement teams must therefore model multi-scenario price paths, hedge strategies, and alternative alloy formulations to preserve margins without sacrificing specification compliance.

Ductile cast iron products used in potable water systems are subject to robust standards and certifications. Compliance with workplace safety, emissions, and product safety frameworks is both mandatory and a market differentiator. Regulatory regimes and certification frameworks (covering drinking water safety and manufacturing emissions) create compliance cost floors and introduce preferred-supplier advantages for producers who invest early in certification and environmental performance.

Electrification and decarbonization investments are now table stakes for forward-looking producers. Projects transforming melt shops demonstrate meaningful CO2 reduction potential and often improve energy efficiency—metrics that corporate buyers and public procurement increasingly value.

Process control, metallurgical precision and digital foundry practices (predictive maintenance, process simulation, and scrap optimization) are proven margin levers. Our report breaks down the expected payback intervals for different technology stacks and highlights supplier partnerships that reduce integration risk.

On the product side, incremental alloy and finishing innovations are enhancing lifetime performance and reducing maintenance costs, which can justify premium pricing in infrastructure and industrial accounts.

The market remains composed of specialized foundries, regional leaders, and niche castings providers. Below we synthesize observable strategic moves and their implications for competition and partnership opportunities.

AMERICAN Ductile Iron Pipe (Birmingham, Alabama): Recent activity includes targeted M&A to broaden piping system capabilities and a headline investment program to modernize melting facilities. These moves reflect a two‑pronged strategy—expand addressable systems and reduce unit carbon intensity via electrification. For competitors, this signals selectively aggressive capacity modernization and downstream integration.

McWane Ductile (Coshocton, Ohio): Continued execution on customer-facing infrastructure projects underscores a capability in delivering complex municipal works. The firm’s project completions are a reminder that operational reliability and project execution remain compelling differentiators in waterworks and municipal procurement.

U.S. Pipe (Birmingham, Alabama): As a long-standing supplier to water and wastewater segments, U.S. Pipe’s positioning speaks to the enduring scale advantages of established brands in regulated procurement environments. Their approach emphasizes material conformity, service-level reliability, and engagement with public-sector project cycles.

Canada Pipe Company, LTD. (Hamilton, Ontario): A regional leader with deep expertise in piping solutions for Canadian infrastructure markets; their footprint demonstrates how local regulatory and procurement regimes favor domestic or regionally proven suppliers.

Ferroloy, Inc. (Wichita, Kansas): Focused on ductile iron castings across agriculture, construction, hydraulics and valves, Ferroloy’s product breadth highlights the attractiveness of diversified end-market exposure as a hedge against cyclical downturns in any single sector.

Collectively, these firms illustrate the competitive bottlenecks—project execution capabilities, compliance and certification, decarbonization investments, and trusted local service networks. The PW Consulting study maps these competitive dimensions to opportunity windows for buyers, suppliers and potential acquirers.

The full PW Consulting publication is designed as an operational playbook, not only a market narrative. Key deliverables include:

Historical market sizing and forward projections (2026–2032) with scenario analyses tied to demand shocks and raw material volatility.

Segment-level demand drivers (by region, process type and end application) with qualitative implications for pricing, margin and inventory strategy—presented in an executive-friendly matrix to support board- and C-suite decision-making.

Supply-chain stress-testing tools that model input-price pass-through, lead-time disruptions and supplier concentration risk.

CapEx and modernization playbooks, with IRR thresholds and sensitivity analyses for electrification and automation investments.

Competitive intelligence dossiers on leading producers and a tracker of announced capacity projects, M&A activity and major infrastructure contracts.

Procurement and commercial tactics tailored to buyers of ductile iron components, including tender design, supplier qualification checklists and specification negotiation levers.

Regulatory and certification roadmap outlining required standards for potable water applications and emissions compliance across primary markets.

Capital planners: Use the market growth profile and payback frameworks to sequence modernization projects—prioritize investments with the quickest emissions and cost benefits under mid-case demand scenarios.

Procurement leads: Implement multi-scenario procurement models that stress raw material prices and lead-time spikes; prepare alternate alloy strategies and multi-sourcing arrangements flagged in our sensitivity analysis.

Business development teams: Target infrastructure procurement windows and industrial replacement cycles identified as near-term opportunity clusters; leverage the competitive profiles to position value propositions and partnership offers.

Corporate development: Use the M&A and capability-gap mapper to prioritize targets that offer scale in project execution, geographic coverage, or decarbonized melting capacity.

The ductile cast iron market in 2026 is not a high-growth breakout; it is a sector where disciplined strategy and operational execution will compound advantage. Our market sizing (USD 3.8 Million in 2025) and the 5.4% CAGR to 2032 indicate an industry offering steady returns for informed incumbents and opportunistic new entrants with clarity on costs, certification, and technology pathways. PW Consulting’s full report offers the detailed segment-level data, supplier scorecards, and scenario tools you need to convert this strategic preview into executable plans.

For decision-ready intelligence, including the granular segmentation, pricing curves, and proprietary supplier assessments referenced here, access the complete PW Consulting Ductile Cast Iron Market report.

For detailed analysis of this topic, please visit the official page:Ductile Cast Iron Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com