Cannabis Pharmaceutical Market Size, Share, Trends, and Industry Forecast by 2032

Other |

2026-06-03 12:10:06

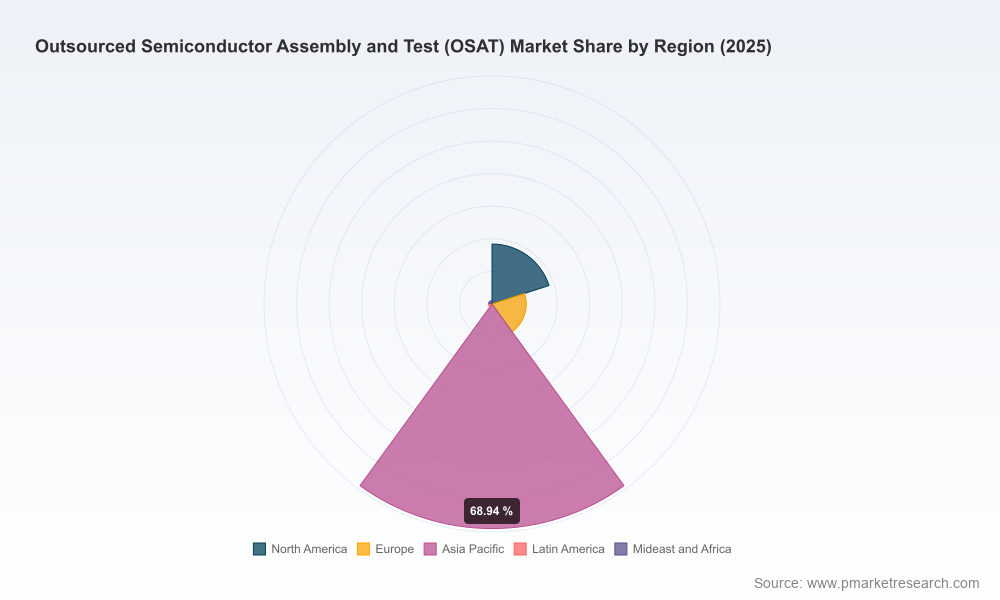

PW Consulting’s latest Outsourced Semiconductor Assembly and Test (OSAT) Market briefing frames the fast‑evolving competitive, regulatory, and capacity landscape that senior leaders must master in 2026. Our independent macro view shows an industry that expanded from the mid‑30s (USD billion) in 2020 to USD 47.1 billion in 2025 and is modeled to reach roughly USD 84.1 billion by 2032 — an annualized expansion consistent with an 8.8% CAGR across the 2026–2032 forecast window. Behind that headline growth lies a complex mix of structural demand (AI, HPC, automotive), acute capacity constraints, geopolitical regulation, and input‑supply frictions. This introduction explains why those dynamics matter for boardroom decisions in 2026, what the full report contains, and how to use it to turn uncertainty into advantage.

Outsourced Semiconductor Assembly and Test (OSAT) Market

Investment timing and scale. With near‑term utilization rates driving price elasticity and multi‑year capacity projects under way, executives must align capex cadence to not only demand growth but also to regulatory timelines and incentives. The difference between on‑time delivery and delayed scale can change payback profiles materially.

Outsourced Semiconductor Assembly and Test (OSAT) Market

Supplier selection and contract design. The market is concentrated: the top three OSAT players control roughly 45% of market share and the top five roughly 50%. That structure creates both bargaining power for leading suppliers and strategic fragility for customers who lack diversified access to advanced packaging and test capacity.

Outsourced Semiconductor Assembly and Test (OSAT) Market

Regulatory and input‑risk mitigation. New export controls, critical‑minerals export restrictions, and country‑level incentives each reshape where and how complex IC assemblies may be produced. Companies that integrate regulatory control gates into sourcing decisions avoid costly retrofit or compliance‑driven process changes.

M&A, joint ventures and alliance strategy. As incumbents expand advanced packaging footprints and new campus builds come online, there are windows for bolt‑on acquisitions, strategic alliances, and capacity partnerships that accelerate time‑to‑market for differentiated packaging solutions.

Demand concentration and technology transition. AI and high‑performance computing have shifted a meaningful portion of OSAT demand toward high‑bandwidth memory, advanced fan‑out and multi‑die integration solutions. This is driving structural premium pricing for specialized memory packaging and wafer‑level advanced packaging services.

Price inflation and utilization. Across 2026 the industry experienced material pricing pressure: service pricing rose broadly (5–20%), with memory packaging surcharges substantially higher where utilization approached capacity limits. Such price moves compress time horizons for investment recovery while improving near‑term cash conversion for capacity owners.

Input‑supply constraints. Export controls on critical minerals have increased procurement complexity for key process inputs, raising the cost and risk of single‑source supply chains. Procurement teams must adopt multi‑tier hedging and substitute planning to preserve throughput for high‑value products.

Regulatory controls on exports. Policy changes introducing worldwide license requirements for select advanced logic ICs mean that OSATs and their customers must implement verified‑conditions workflows or risk transactional friction. Compliance architecture now sits at the intersection of legal, operations and supply chain functions.

Capacity expansion and geographic reshaping. Large greenfield initiatives and modular campus builds are reshaping the global footprint of advanced packaging. These investments create opportunities for offshoring/nearshoring decisions influenced by incentive programs, labor availability, and geopolitical risk.

The OSAT field is diverse: a handful of global leaders combine scale and breadth of service offerings, while regional champions and specialized players compete on niche capabilities and customer intimacy.

Scale incumbents: Leading global OSATs combine high‑volume assembly/test operations with rapid deployment of advanced packaging lines (e.g., wafer‑level packaging, SiP, 2.5D/3D integration). These players leverage scale to serve AI, HPC, automotive, and communications segments, and their capital programs are pivotal moving pieces for industry capacity planning.

Large U.S. projects and incentives: Strategic campus developments backed by incentives are altering the global map for advanced packaging capacity. Such projects accelerate domestic capabilities for advanced packaging and test, but they also require multi‑year execution discipline and skilled labor deployment.

China‑based consolidation and specialization: Regional leaders have strengthened wafer bumping, SiP and test capabilities — especially for AI accelerators, power devices and industrial chips — making them essential partners for local and global OEMs seeking cost or access advantages.

Specialized memory and high‑reliability niches: Some OSATs concentrate on memory (HBM, DRAM, NAND) and high‑reliability markets (aerospace, defense, medical). These specialists command differentiated price points and must be considered separately when modeling product‑level margin trajectories.

Recent industry events underscore these themes: several firms have announced major greenfield builds and capacity ramp plans, and market pricing reactions reflect near‑term tightness. Leaders are pursuing a mix of organic capacity additions, targeted partnerships, and selective downstream integration to secure access to critical packaging competencies.

Macro and bottom‑up market sizing and scenarios — three demand paths (baseline, constrained, accelerated) with spend, unit and ASP modeling through 2032. Note: detailed subsegment tables (regional, service, packaging type, application) are reserved for the full report to preserve investigative value.

Supplier heat maps and scorecards — capacity, technology readiness, customer mix, margin bands and execution risk for leading and mid‑tier OSATs, informed by primary interviews and proprietary plant‑level data.

Pricing and profitability toolkit — models to test contract structures (spot, LTAs, capacity reservation), pass‑through clauses, and sensitivity analysis for input price shocks and utilization swings.

Regulatory and compliance playbook — step‑by‑step controls mapping for export‑license impacted flows, verified‑conditions checklists, and organizational governance templates to reduce transactional friction.

Supply‑chain resilience maps — critical‑input dependency matrices, alternative supplier pathways, and inventory/obsolescence rules optimized for product criticality and margin.

Strategic options and transaction pipeline — prioritized M&A themes, JV structures, and capex partnership models calibrated to different risk appetites and time‑to‑market objectives.

Executive briefing packs — board‑level one‑pagers, CFO ROI templates, and procurement negotiation playbooks designed to accelerate decision cycles.

Chief Strategy Officers: Use our scenario outputs to stress‑test growth plans, evaluate alternative sourcing geographies, and define trigger points for M&A or alliance pursuits.

Chief Financial Officers: Leverage the pricing toolkit and capex templates to model payback under multiple utilization and pricing regimes; align treasury and hedging strategies to procurement exposure for critical minerals.

Procurement and Supply Chain Leads: Adopt the supplier heat maps and resilience playbooks to redesign sourcing lanes, implement multi‑tier risk monitoring, and negotiate capacity reservation terms tied to service level KPIs.

R&D and Product Leadership: Map product roadmaps to available packaging primitives; prioritize features that align to available capacity and long‑lead packaging technologies to shorten commercialization cycles.

Secure prioritized capacity for high‑value products through blended contracting (short‑term spot + long‑term capacity reservations) to combine flexibility with certainty in tight markets.

Diversify critical‑input sourcing and build a minerals risk register; establish secondary suppliers and qualified substitution processes for gallium/germanium sensitive operations.

Embed export‑control compliance early in supplier selection and design‑transfer processes; adopt verified‑conditions workflows to avoid transactional hold‑ups.

Consider strategic partnerships with specialized OSATs for memory and high‑reliability segments rather than full ownership; speed to market often favors capacity agreements over greenfield timing risk.

Align incentives and funding opportunities with capex plans — leverage public incentive programs where appropriate, but model the full economics including long lead times for workforce and qualification.

The OSAT market in 2026 is a growth story underpinned by structural demand from next‑generation compute and edge markets, but it is also a high‑friction environment where policy, raw materials, and capacity timing create real operational and strategic risk. With a base market of USD 47.1 billion in 2025 and modeled expansion to approximately USD 84.1 billion by 2032 at an 8.8% CAGR, the headline opportunity is clear — the critical task for leaders is to convert that growth into durable competitive advantage by mastering supplier ecosystems, regulatory compliance, and capital deployment.

PW Consulting’s full OSAT Market report provides the granular segmentation, supplier scorecards, and executable playbooks required to make those choices with confidence. For the granular subsegment tables, company‑level scorecards, and the operational templates referenced above, access the complete study on our report page.

For detailed analysis of this topic, please visit the official page:Outsourced Semiconductor Assembly and Test (OSAT) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com