TV White Space Spectrum Market — Strategic Preview for 2026 Decision Makers

By PW Consulting — Senior Strategy & Industry Analysis

TV White Space Spectrum Market

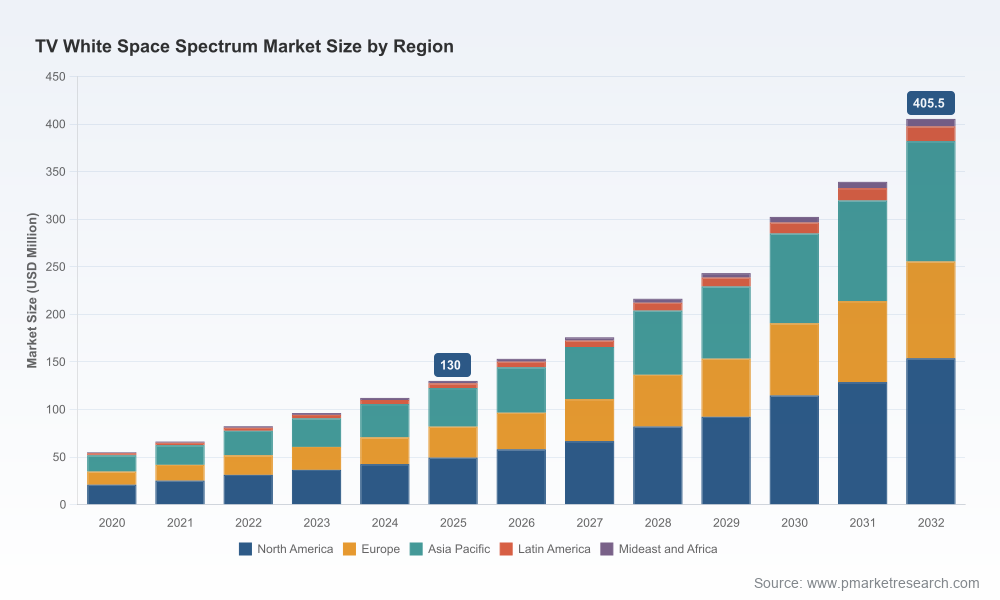

The TV White Space (TVWS) spectrum market is entering a strategic inflection point. Our baseline market model (base year 2025) shows the global TVWS market expanding from approximately USD 55 million in 2020 to USD 130 million in 2025, thereafter projecting robust growth through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 17.8%. By 2032 the market is expected to exceed USD 400 million (USD Million basis). For executives planning capital allocation, partnerships, or regulatory engagement in 2026, these dynamics create a finite window to capture scale advantages before the market consolidates further.

TV White Space Spectrum Market

Market trajectory and the 2026 inflection

Three converging forces are driving the 2026 strategic calculus:

TV White Space Spectrum Market

- Regulatory liberalization: Recent rulemaking and certification advances have meaningfully increased the usable channel inventory and clarified operational conditions for both fixed and portable TVWS devices. These regulatory changes reduce deployment friction and improve capacity planning for service providers.

- Technology maturation: Software-defined radios, robust ruggedized appliances for mission-critical use, and field-proven dynamic spectrum access systems have moved from lab demonstrations to commercial products. Vendors are shipping next‑generation radios and adaptive spectrum-sharing platforms tailored for broadband, IoT, and smart-grid applications.

- Anchor deployments and demand validation: Large-scale initiatives and targeted deployments — including rural broadband programs and emergency communications pilots — have validated business models and unit economics in multiple geographies, enabling repeatable GTM approaches.

For 2026, these forces mean that tactical execution (pilots, partnerships, and regulatory positioning) will determine which players capture the disproportionate benefits of scale. The market is growing quickly, but early mover advantages will concentrate returns.

Structural dynamics and competitive architecture

The competitive structure already displays meaningful concentration: the top three vendors control a material portion of market activity, with the top five commanding a dominant share. That structure creates both risks and opportunities for new entrants and incumbents:

- Risk: Buyers face vendor lock-in when an integrated stack (radio hardware + spectrum database + management software + services) is offered by leading suppliers.

- Opportunity: Niche players with superior software, spectrum database capabilities, or ruggedized hardware can be acquisition targets or can form symbiotic partnerships with large integrators and public-sector programs.

Key competitive profiles (selected):

- Carlson Wireless Technologies — Arcata, California (https://www.carlsonwireless.com/). A leader in TVWS radio solutions with a focus on rural broadband and emergency communications. Recent product launches emphasize longer signal range and field-deployable form factors suitable for low‑infrastructure contexts.

- Adaptrum — San Jose, California (https://adaptrum.com/). An early proponent of dynamic spectrum access. Their roadmap centers on adaptive TVWS sharing suited for IoT and smart-city verticals, with a strong software component that targets scalability for dense M2M deployments.

- Microsoft Corporation — Redmond, Washington (https://www.microsoft.com/). A non‑traditional telecom player that operates TVWS-enabled rural broadband projects through initiatives such as Airband. Its role as a program operator and large-scale deployer materially de‑risked certain use cases and demonstrated end-user demand at scale.

- 6Harmonics — Ottawa, Canada (https://6harmonics.ca/). Positioned on ruggedized hardware and mission‑critical use cases; their products target harsh-environment deployments for public safety and industrial networks.

- Shared Spectrum Company — United States (https://www.sharedspectrum.com/). A provider of spectrum database and management services; essential for compliance-based TVWS operations and a natural partner for device OEMs and operators seeking certified GLSDB integration.

- Metric Systems Corporation — United States (https://www.metricsystems.com/). Integrator of TVWS network infrastructure and solutions for wireless broadband.

- Aviacomm — United States (https://aviacomm.com/). Developer of software-defined radio solutions that facilitate dynamic spectrum access and flexible deployment models.

- Meld Technology Inc — United States (https://www.meldtech.com/). Focused on turnkey TVWS solutions for broadband and enterprise connectivity applications.

Recent competitive moves — including product launches by Carlson, Adaptrum and Aviacomm in 2024, and Microsoft’s expansion of its Airband Initiative (deploying TVWS-based services to additional underserved communities in 2025) — indicate an acceleration from R&D to scale deployments. For investors and technology buyers, vendor selection increasingly hinges on software/platform capabilities and database partnerships as much as on raw RF performance.

Strategic implications for 2026 decisions

Executives who will outperform in 2026 will align investment choices to capture three linked outcomes: reduced time-to-market, defensible margins, and regulatory resilience. Below are priority actions tied to those outcomes.

- Secure spectrum-management partnerships early. Certification and GLSDB integration are non-trivial procurement items. Negotiate access and service-level commitments with certified database operators or consider strategic investment in in-house database capability to control operational risk.

- Prioritize software-defined architectures. SDR and dynamic spectrum management are the vectors for future product differentiation. Allocate R&D to modular, upgradable platforms that can adapt to regulatory changes and new sharing rules without full hardware replacement.

- Design vertical-first go-to-market plays. Smart grid, emergency services, rural ISPs, and transportation are converging on TVWS for distinct reasons. Build packaged solutions (hardware + DB + managed service) that map to procurement cycles and financing models of public agencies and utilities.

- Pilot at scale to de-risk unit economics. Move beyond lab pilots to 12–24 month deployments in representative markets. Capture measured KPIs (throughput, latency, uptime, TCO per connected premise) to refine pricing and deployment playbooks before committing large CAPEX.

- Consider M&A and partnerships to neutralize concentration risks. With a concentrated supplier base, acquiring niche capabilities (DB management, ruggedized hardware, or systems integration) accelerates route-to-market and reduces dependency on single vendors.

- Embed regulatory monitoring in operating processes. Regulatory rule changes — particularly database certification, protection margin settings, and device authorization criteria — materially affect capacity and interference risk. Operationalize policy tracking and advocacy as a business function.

What our full report delivers (practical, execution-ready content)

The PW Consulting TVWS report is structured as an execution toolkit for 2026 planning cycles. Core deliverables include:

- Market sizing and forecast model (base year 2025; historical review 2020–2025; detailed forecast 2026–2032) with downloadable time-series for scenario and sensitivity testing.

- Scenario analyses that stress-test regulatory, technology, and demand variables and show upside/ downside paths for investment returns.

- Vendor benchmarking and scorecards assessing radio performance, software maturity, database integrations, and service delivery capabilities.

- Deployment playbooks for five priority verticals — including procurement templates, partner maps, and field trial designs — enabling rapid replication of successful pilots.

- Techno-economic models that estimate CAPEX/OPEX envelopes, payback timelines, and customer-acquisition economics for alternative service models.

- Regulatory tracker and engagement playbook: a practical guide to certification requirements, database compliance, and advocacy levers in priority jurisdictions.

- M&A and partnership decision matrices to evaluate tuck-in acquisitions, joint ventures, and supplier agreements in a concentrated competitive landscape.

To comply with our “trailer” principle, we present high‑confidence directional findings and strategic recommendations here while withholding detailed segmented tables and granular sub‑regional or application revenue splits. The full dataset, vendor scorecards, and the downloadable market model are available in the full report.

Operational checklist for Q1–Q4 2026

Translate strategy into the first 12 months with a focused checklist:

- Launch two geographically and operationally diverse pilots (one public sector, one commercial) to validate service bundles and pricing.

- Execute at least one strategic alliance with a certified GLSDB provider or negotiate exclusivity for database access in target counties.

- Begin SDR integration roadmaps and allocate 20–30% of product development spend to software-upgradeable features.

- Establish regulatory monitoring and a stakeholder engagement calendar aligned to expected FCC/ISED/ICASA updates.

- Run a vendor sourcing exercise focusing on end-to-end compliance, interoperability, and service-level guarantees.

Conclusion — why 2026 matters

Absolute market dollars are still modest versus other wireless segments, but the growth trajectory and regulatory shifts create a classic “platform opportunity” where early positioning yields outsized returns as the market scales. The top-line numbers show a market set to more than triple over the coming decade on a high‑teens CAGR; the strategic prize in 2026 is to convert early wins into sustainable market share before consolidation accelerates.

PW Consulting’s complete TV White Space Spectrum Market report contains the granular segmentation, vendor scorecards, and the full forecast model you need to operationalize these recommendations. Access the full report for the confidential spreadsheets, detailed regional and application breakdowns, and our vendor ranking matrix to inform 2026 investment and partnership decisions.

For detailed analysis of this topic, please visit the official page:TV White Space Spectrum Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com