Gracilaria Agarose and Gelidium Agarose Market — Strategic Outlook for 2026

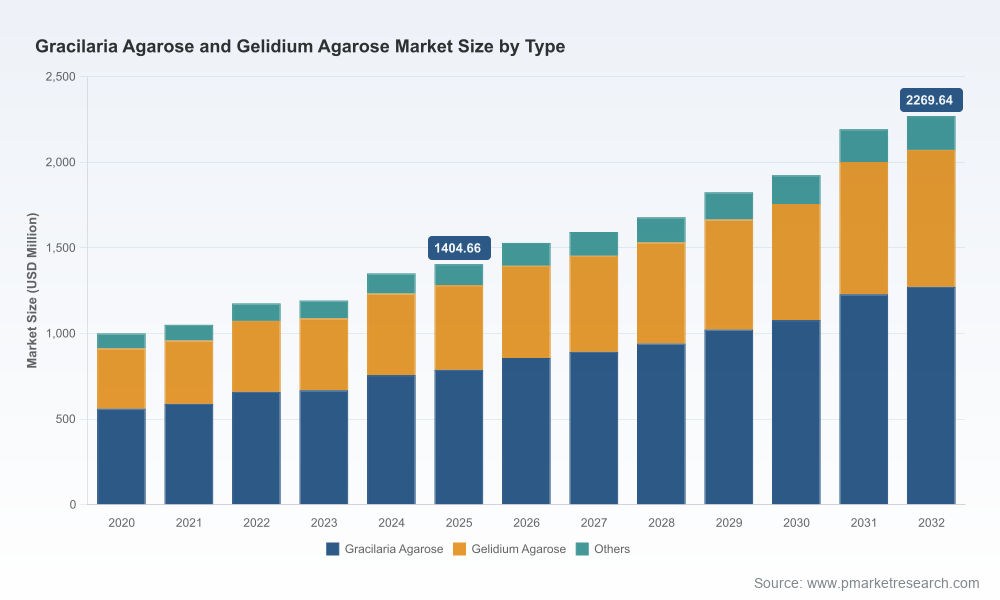

As companies prepare strategy for 2026 and beyond, clarity on where value pools will form in the Gracilaria and Gelidium agarose complex is essential. PW Consulting’s latest market study (base year 2025; forecast 2026–2032) synthesizes primary research, supplier due diligence and scenario-based forecasting to help commercial leaders translate a projected compound annual growth rate (CAGR) of 7.1% into defensible decisions. The global market is on a clear growth trajectory — expanding from roughly USD 1.0 billion in 2020 to an estimated USD 1.4 billion in 2025, and forecast to exceed USD 2.2 billion by 2032 — creating distinct opportunities and strategic pressures across supply, product differentiation and regulation.

Gracilaria Agarose and Gelidium Agarose Market

Why this study matters for 2026 decision-makers

- From volume growth to margin capture: Growth is not uniform across grades, applications and channels. With aggregate market expansion at ~7% annually, the strategic question for 2026 is how to convert top-line demand into sustainable margin improvement — through premium specialty grades, downstream value-added products, or scale-optimized commodity supply.

- Timing matters: The near-term period (2026–2028) presents a window for capacity investments and partnership formation before several structural supply-side shifts accelerate in the 2029–2032 horizon. Executives who lock in feedstock access and regulatory pathways early will secure asymmetric advantage.

- Regulatory and certification gatekeeping: Food and biotechnology applications require distinct regulatory and quality credentials. FDA GRAS considerations (21 CFR Part 184) and quality regimes such as ISO 9001 and cGMP for bioprocessing resins are not optional; they are commercial enablers.

What the market numbers tell us (macro perspective)

The dataset projects steady expansion from a 2025 market base of about USD 1.4 billion to roughly USD 2.27 billion by 2032 under a central 7.1% CAGR. This trajectory is consistent with rising demand from molecular biology and clinical diagnostics, continued innovation in food and cosmetic formulations, and increasing adoption of agarose-based resins in bioprocessing. Importantly, measured market concentration is modest: the top three players account for less than one-quarter of the market, and the top five capture under a third. That combination of growth and fragmented supply creates both scale opportunities for incumbents and entry points for nimble challengers.

Gracilaria Agarose and Gelidium Agarose Market

Key structural dynamics shaping strategy

- Feedstock economics and geography: Gracilaria remains the dominant biomass source worldwide (FAO reporting indicates it contributes ~66% of global agar production). Feedstock availability, harvesting cost, and logistics determine the economics of both commodity agar and high-purity agarose. Companies should stress-test sourcing strategies against price volatility, seasonal yield swings and regulatory import regimes.

- Premiumization of high‑purity grades: Pharmaceutical- and diagnostics-grade agarose commands a quality premium, requiring tighter process control, traceability and certification. Achieving and demonstrating cGMP/ISO compliance is often a pre-condition for entering higher-margin segments.

- Regulatory and tariff complexity: Food additive use is governed by GRAS criteria in the US and parallel frameworks elsewhere, and imports of seaweed-derived materials face variable tariffs in major markets as trade policy adapts to protect local cultivation. Companies must integrate regulatory outlooks and tariff scenarios into commercial planning.

- Consolidation and capability plays: Low market concentration today coexists with strategic capacity expansions and product launches by key suppliers — moves that can shift supply dynamics rapidly. Expect targeted M&A, JV formation and greenfield expansion focused on specialty agarose for chromatography and therapeutic applications.

What our report delivers — practical content for action

The full PW Consulting study is structured to move leaders from insight to execution. Highlights include:

Gracilaria Agarose and Gelidium Agarose Market

- Proprietary bottom‑up market model (2020–2032) with scenario pathways and sensitivity to feedstock, yield and regulatory shock assumptions.

- Supply chain mapping and supplier scorecards — from raw seaweed harvesters through extraction, purification and finished agarose resins — with a focus on capacity, cost drivers and margin pools.

- Commercial playbooks for three archetypal buyers: (1) large biopharma chromatography resin makers, (2) food and beverage ingredient buyers, and (3) cosmetics/consumer ingredient suppliers. Each playbook includes procurement levers, spec rationalization and contract design templates.

- Regulatory and quality readiness checklists covering GRAS, ISO 9001, cGMP and analytical methods for gel strength and purity required in biotech applications.

- Go‑to‑market and pricing frameworks for premium versus commodity agarose, including margin benchmarking and guidance on up‑trading product lines.

- Risk matrix and mitigation playbook for feedstock scarcity, tariff exposure, climate impacts on coastal harvesting and contamination risks — with contingency actions and supplier diversification mapping.

- Deal diligence and M&A target short‑list methodology tailored to buyers seeking inorganic growth or backward integration into seaweed cultivation/extraction.

Competitive landscape — who to watch

The marketplace combines specialized manufacturers, ingredient houses and regional producers. Key companies profiled in our study include:

- Agarose Bead Technologies (Burgos, Spain) — a specialist in high-performance agarose resins for bioprocessing and chromatography. Notable: a facility expansion in September 2024 increased resin production capacity materially, signaling a push into therapeutic downstream processing demand (Agarose Bead Technologies press release, 2024).

- Java Biocolloid (Indonesia) — focused on purified agarose and agar products derived from Gracilaria and Gelidium. Recent product launches and trade show activity in 2025 expanded their cosmetics-grade offering, reflecting a strategic pivot into higher value consumer ingredients (Java Biocolloid announcements, 2025).

- CyberColloids Ltd (Ireland) — hydrocolloid specialist with capabilities across agarose and functional texturizers.

- Hispanagar S.A., Industrias Roko and a set of established ingredient suppliers and regional processors — each plays distinct roles from research reagent supply through industrial food-grade agarose.

- Ingredient houses and distributors (e.g., Ingredion, Colony Gums, Lodaat) that shape channel dynamics between producers and end‑use sectors.

Recent corporate activity demonstrates the mixed nature of competition: capacity investment by resin-focused players, product launches aimed at cosmetics and food formulators, and increased trade show visibility for new purified agarose lines. These moves indicate parallel strategies — scale and specialization — converging in the mid-decade market.

Strategic implications and recommended actions for 2026

- Secure feedstock access with layered contracts: For manufacturers, near-term contracting with differentiated clauses (indexation to biomass yield, quality bonuses for low contaminants, and force‑majeure clarity for climate events) reduces supply risk. Suppliers should pursue vertical partnerships with coastal cultivators to stabilize costs.

- Differentiate through certified quality: Investment in cGMP, ISO 9001 and robust analytics is a pre-requisite for premium segments. Buyers and producers alike should prioritize these certifications as commercial gates to higher-margin channels.

- Optimize product portfolio by value path: Segment SKUs into commodity, specialty food and high-purity biotech grades; allocate capital and marketing resources to the highest IRR pathways while maintaining optionality for up‑trading.

- Hedge tariff and trade risk: Scenario‑driven sourcing and local/regional packaging hubs can mitigate exposure to variable tariffs. Multinational buyers should embed tariff sensitivity into supplier scorecards and procurement playbooks.

- Prepare for consolidation windows: Given the market’s fragmentation and rising demand, 2027–2030 is likely to see M&A activity. Buyers should develop acquisition criteria and a pipeline of targets now; sellers should prepare by strengthening compliance and traceability dossiers to maximize valuation.

- Invest in sustainability as a market differentiator: Traceability, low‑impact harvesting and community engagement are commercially valuable in food and cosmetic channels and increasingly expected in corporate procurement frameworks.

KPIs and decision triggers to monitor in 2026

- Quarterly feedstock price indexes and harvest volume reports from major producing regions.

- Regulatory updates on GRAS determinations and import tariff changes in key markets.

- Capacity utilization and announced expansions by resin-focused producers.

- Order intake and formulation wins in diagnostics, molecular biology and cosmetics segments.

- Certification milestones (cGMP/ISO) achieved by suppliers and competitors.

Final note — the value of the full study

This briefing highlights the strategic contours of the Gracilaria and Gelidium agarose market and provides actionable guidance for 2026 planning. The complete PW Consulting report contains the granular scenario outputs, supplier scorecards, segmented demand models and transaction advisories that executives and investment committees need to operationalize these insights. To review the detailed segmentation, region- and application-level forecasts, and the full set of tactical playbooks and model assumptions, please consult the full report on our site.

For detailed analysis of this topic, please visit the official page:Gracilaria Agarose and Gelidium Agarose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com