Automotive Control Arm Market: Strategic Outlook for 2026 Decision-Makers

Executive summary

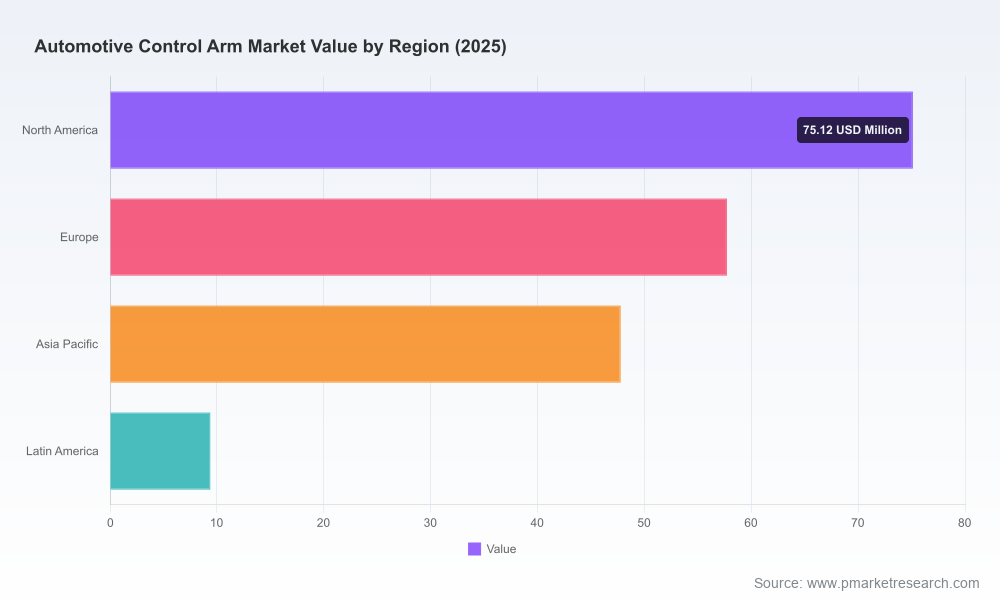

As original equipment manufacturers (OEMs), tier suppliers, aftermarket players and private equity sponsors calibrate capital and go-to-market plans for 2026, the automotive control arm market presents a measured but strategically rich growth profile. Our new PW Consulting industry study—anchored on 2025 as the base year—projects a steady expansion from a market size of approximately USD 190 million in 2025 to a mid‑to‑high two‑hundred million range by 2032 at a 3.28% compound annual growth rate (CAGR). This trajectory masks meaningful pockets of volatility and opportunity: product modularization for chassis systems, material substitution pressures (steel → aluminum), aftermarket parts proliferation, and regulatory-driven safety liabilities that are reshaping supplier economics.

Automotive Control Arm Market

Why this report matters for 2026 decision cycles

- Budgeting and capex prioritization: A low‑single‑digit CAGR can lull organizations into underinvestment. Our report isolates where modest growth justifies targeted capex (capabilities such as hydroforming, precision casting, and integrated assembly cells) versus areas that require cost containment or consolidation.

- Product roadmap alignment: Control arms are increasingly integrated into broader chassis and ADAS architectures. We map technical trajectories so product managers can prioritize features that matter to OEMs and aftermarket service providers in the 2026 procurement window.

- M&A and portfolio rationalization: Market concentration metrics indicate an industry that is neither fully fragmented nor monopolized—creating conducive conditions for bolt‑on acquisitions and carve‑outs. The report provides an M&A readiness framework and shortlist criteria for strategic targets.

- Aftermarket vs OE playbook: The aftermarket expansion driven by legacy vehicle populations creates differentiated margin dynamics from OE contracts. We deliver channel‑specific pricing, warranty and SKU rationalization strategies tailored to 2026 commercial cycles.

Market trajectory — what the headline numbers tell you (and what they hide)

Headline: at a 3.28% CAGR across the 2026–2032 forecast window, the control arm market grows steadily but does not follow the hyper‑growth patterns seen in powertrain electrification or ADAS sensor markets. That makes the segment attractive for companies seeking predictable, margin‑stable returns subject to operational excellence rather than speculative demand spikes.

Automotive Control Arm Market

Importantly, macro growth masks heterogeneity—some product types and manufacturing routes grow faster due to lightweighting and modularization, while legacy steel-based lines remain volume anchors. Our study quantifies these differentials and models the sensitivity of revenue and margin to material cost shocks, tariffs, and assembly automation investments—without disclosing the proprietary granularity in this executive summary.

Automotive Control Arm Market

Competitive landscape — who matters and why

The market sits at a mid‑concentration level. A handful of global players consistently capture share through OE relationships, extensive SKU portfolios and aftermarket coverage; simultaneously, regional manufacturers persist in lower‑cost geographies. Key strategic profiles included in our competitive assessment:

- ZF Friedrichshafen AG — Strong aftermarket presence under the TRW brand with OE‑spec control arms and an expanding chassis SKU set. Recent aftermarket catalog updates broaden replacement coverage and present tactical threats and opportunities for regional aftermarket consolidators.

- BorgWarner Inc. (Delphi brand) — Leverages steering and suspension integration experience to position wishbones and control arms as part of broader steering-suspension system sell‑ins to multiple OEM lines, strengthening aftermarket credibility for late‑model applications.

- Magna International Inc. — Vertical capabilities across hydroforming, stamping, casting and assembly make Magna a natural partner for OEMs seeking single‑source chassis modules. Their breadth mitigates technology transition risk for OEMs.

- BENTELER — High volume production of steel and aluminum components positions Benteler as a cost‑focused, scale supplier for both front and rear suspension modules.

- Schaeffler AG — Offers OE‑grade steering and suspension arms with a focus on lifetime testing and vehicle longevity solutions appealing to premium OEMs.

- Continental AG — Adds value through precision bearings, vibration damping and corrosion‑resistant components targeted to European OEM specifications and aftermarket channels.

Recent catalog expansions from leading suppliers demonstrate an aftermarket push to capture replacement demand and defend OEM relationships. These moves matter strategically: they increase SKU complexity for distributors, compress aftermarket margins in the near term and elevate the premium for OEM tier status in the longer term.

What the full PW Consulting report contains (actionable, execution‑ready)

- Segmented demand models (by vehicle class, production vs. aftermarket, and material class) with sensitivity to fuel/electric vehicle mix and geographic production shifts. Note: this summary intentionally omits the cell‑level segmentation data—full tables are available in the report.

- Supply‑side mapping: manufacturing footprints, cost curves for hydroforming vs stamping vs casting, and labor automation inflection analysis.

- Price and margin benchmarking across OE and aftermarket channels with contract negotiation playbooks for 2026 procurement cycles.

- M&A playbook: screening filters, valuation heuristics, integration risk checklists and a shortlist of archetypal targets by capability gap (lightweighting, modular assembly, aftermarket distribution).

- Regulatory and litigation risk dashboard (safety recalls, material regulations, and regional compliance requirements) and corresponding mitigation strategies for suppliers and distributors.

- Scenario planning: a base case (aligned to the headline CAGR), a downside (macro slowdown and steel/aluminum price shock), and an upside (accelerated lightweighting and aftermarket replacement surge) — each with P&L and capex implications.

Strategic implications and recommended actions for 2026

- Prioritize modular assembly investments: For firms pursuing OEM contracts, the marginal ROI of multi‑model chassis cells is higher than point upgrades. Invest in flexible automation that reduces changeover time between upper/lower arm families.

- Hedge material exposure: Establish dual‑sourcing for steel and aluminum feedstocks, and consider hedging strategies or long‑term supplier agreements to dampen raw‑material volatility impact on margins.

- Aftermarket SKU rationalization: Rationalize SKU portfolios to focus on high‑turn and high‑margin SKUs, and align distribution partnerships regionally to minimize inventory carrying costs.

- M&A focus: Target assets that bring either lightweighting capabilities, regional aftermarket distribution, or niche OE relationships—particularly companies with predictable cashflows and low integration complexity.

- Safety and compliance leadership: Integrate lifecycle testing and traceability into product offers. Proactive compliance and public‑facing safety verification can become competitive differentiators in bids and aftermarket trustworthiness.

Regulation, recalls and dynamics — what keeps procurement awake at night

Regulatory and safety events remain high‑impact, low‑frequency risks. Recent recall activity linked to lower control arm ball joint assembly has elevated scrutiny across procurement and warranty teams; supply chain traceability and third‑party validation will be procurement bargaining chips in 2026 tenders. Concurrently, leading aftermarket suppliers increasingly emphasize OE‑spec testing and vehicle lifetime fitment claims as a competitive positioning play. The report’s risk dashboard connects these operational realities to insurance, warranty provisioning and reputational exposure metrics.

Methodology and data confidence

Our analysis synthesizes production and registration datasets, supplier financials, catalog and SKU analyses, and primary interviews with OEM chassis engineers, aftermarket distributors and tier suppliers. We apply scenario analysis to account for commodity cycles, electrification shifts and regulatory changes. Confidence in the headline projection is high for the base case given stable vehicle parc dynamics; however, individual company outcomes will vary materially by execution on cost, quality and channel strategy.

How boards and strategy teams should use this study in 2026

- Use the scenario P&L outputs to stress‑test capital allocation and determine the threshold ROI for automation projects.

- Embed the M&A playbook into a 12–24 month acquisition pipeline; prioritize bolt‑ons that close capability gaps identified in supplier audits.

- Adopt the warranty and safety checklist as a procurement addendum for all incoming control arm contracts to reduce recall risk and lifecycle cost exposure.

- Leverage the market concentration analysis to negotiate improved commercial terms with dominant players or to identify white‑space opportunities for regional consolidation.

Final note — this article is a strategic trailer

This briefing is designed to demonstrate the analytical depth of PW Consulting’s Automotive Control Arm Market study and to map immediate, decision‑relevant implications for 2026. It purposefully omits the granular cell‑level segmentation tables, SKU‑level pricing matrices, and proprietary target lists that populate the full report. For organizations preparing board decks, RFPs or M&A diligence packages in 2026, the full report provides the necessary quantitative detail and executable playbooks.

Call to action

For access to the complete dataset, scenario models, supplier scorecards and the M&A shortlist, contact PW Consulting to obtain the full Automotive Control Arm Market report and a tailored executive briefing for your leadership team.

For detailed analysis of this topic, please visit the official page:Automotive Control Arm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com