Global Styrene Butadiene Rubber (SBR) Market Growing at 6.0% CAGR Through 2034

Other |

2026-07-07 12:41:00

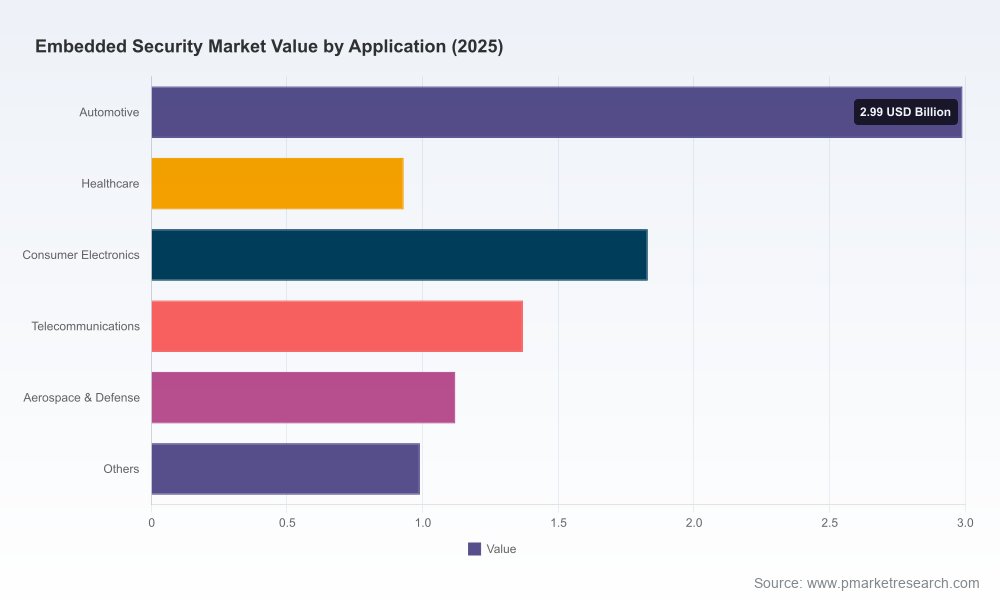

As embedded systems permeate every layer of digital infrastructure — from connected vehicles and medical devices to consumer wearables and industrial controllers — the economics and risk profile of embedded security have shifted from niche engineering concerns to board-level strategic imperatives. Our Embedded Security Market study, anchored on a 2025 base year, shows the market expanding from roughly USD 6.25 billion in 2020 to USD 9.23 billion in 2025, and projecting to reach approximately USD 17.42 billion by 2032 at a compound annual growth rate of 9.54%. Those headline numbers understate the heterogeneity beneath: demand drivers, compliance timelines, supplier concentration and technology inflection points vary materially by application class and procurement archetype. This executive introduction synthesizes the market dynamics that should shape 2026 capital, product and M&A decisions — while reserving the granular segment models and vendor scorecards for the full report.

Embedded Security Market

Several converging forces make 2026 a decision inflection point for companies that embed security into silicon, firmware and products. First, regulatory momentum is accelerating: region- and sector-specific requirements — exemplified by the EU Cyber Resilience Act and industry standards such as ISO/SAE 21434 for automotive — are concretizing compliance obligations that push hardware-root-of-trust and documented secure development lifecycles into procurement contracts. Second, attacker sophistication is evolving to exploit hardware and firmware attack surfaces, a trend codified by new frameworks such as MITRE’s Embedded Systems Threat Matrix. Finally, vendors are starting to ship the next generation of security primitives — from integrated HSMs in MCUs to secure enclaves with post-quantum accelerators — creating a technology refresh window for OEMs and system integrators.

Embedded Security Market

Our full study delivers these deliverables in executable forms — spreadsheet models, vendor scorecards, compliance roadmaps and a set of decision trees you can use in Q1 2026 to set budget, supplier selection and engineering priorities.

Embedded Security Market

The embedded security vendor ecosystem is a blend of long-established semiconductor houses, systems software specialists and agile start-ups. Market concentration is meaningful: the top three vendors control the largest share of commercial supply, and the top five widen that footprint further. This structure creates both systemic strengths — scale in certification, manufacturing and channel reach — and vulnerabilities, notably around supply concentration and geopolitical exposure.

Recent corporate moves are informative about strategic direction: capacity expansions targeted at automotive secure microcontrollers, joint ventures to enable vehicle-to-grid secure modules, and collaborative development of 16 nm secure elements with post-quantum accelerators. These are not isolated product announcements; they reflect a broader reallocation of R&D and capital toward hardware-based security primitives and post-quantum readiness.

Two supply-side dynamics merit urgent attention by procurement and engineering leadership. First, semiconductor and secure-element supply is concentrated: ‘ghost-foundry’ risks and node-specific bottlenecks materially increase lead times and dilution in negotiation leverage for organizations requiring high-assurance parts. Second, the human capital required to verify secure-element firmware and complete compliance evidence is scarce — our analysis flags multi-year skill gaps for healthcare and industrial segments. Both constraints create a premium for early commitment to suppliers, shared certification programs and supplier co-investment models.

Products shipping in late 2025 and into 2026 are beginning to incorporate post-quantum primitives at the silicon or accelerator level, and some secure-enclave launches now include lattice-based key-exchange support. For forward-looking OEMs, the key questions are timing and interoperability: when to adopt hybrid schemes, how to validate post-quantum implementations against evolving standards, and how to preserve upgrade paths for long-lived devices. These questions shape both product roadmaps and procurement specifications.

The full PW Consulting study provides the tactical instruments necessary to convert insight into action: a calibrated forecast model by product architecture and use case, vendor strength/weakness matrices, compliance timelines mapped to engineering milestones, procurement templates and a supply-risk heatmap that combines capacity, foundry exposure and certification readiness. We designed the deliverables for rapid integration with capital planning and product-gating processes in Q1–Q2 2026.

We have deliberately kept this introduction at the strategy level to comply with the “trailer” approach: it surfaces the decisive trends and the operational implications that should govern executive choices this year, while omitting the granular segment tables, vendor revenue breakdowns and the proprietary scoring used to rank suppliers. Those assets — including downloadable models and supplier dossiers — are available through the full report package.

If your 2026 plans include new device rollouts, automotive integrations, health-tech deployments or industrial modernization programs, now is the moment to align security architecture, supplier commitments and compliance evidence. The embedded security window is finite: choices made in 2026 will determine both risk exposure and differentiation across a product’s multi-year in-field lifecycle.

For detailed analysis of this topic, please visit the official page:Embedded Security Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com