How an LMPC Certificate Helps Ensure Legal Compliance for Packaged Products

Other |

2026-07-03 05:19:33

As organisations calibrate capital plans and supply-chain strategies for 2026, the tipper market is re-emerging as a strategic decision node across mining, construction and bulk-transport sectors. PW Consulting’s forthcoming Tipper Market study uses 2025 as the analytical base and projects the market forward with a compound annual growth rate (CAGR) of 4.8% across the 2026–2032 forecast window. The trajectory from the early‑2020s into the next decade is clear: after steady recovery, the market is on a higher-growth path toward the end of the forecast period. This preview explains why those topline dynamics matter for executives, procurement leaders and investors — and outlines the practical intelligence the full report delivers to inform 2026 decisions.

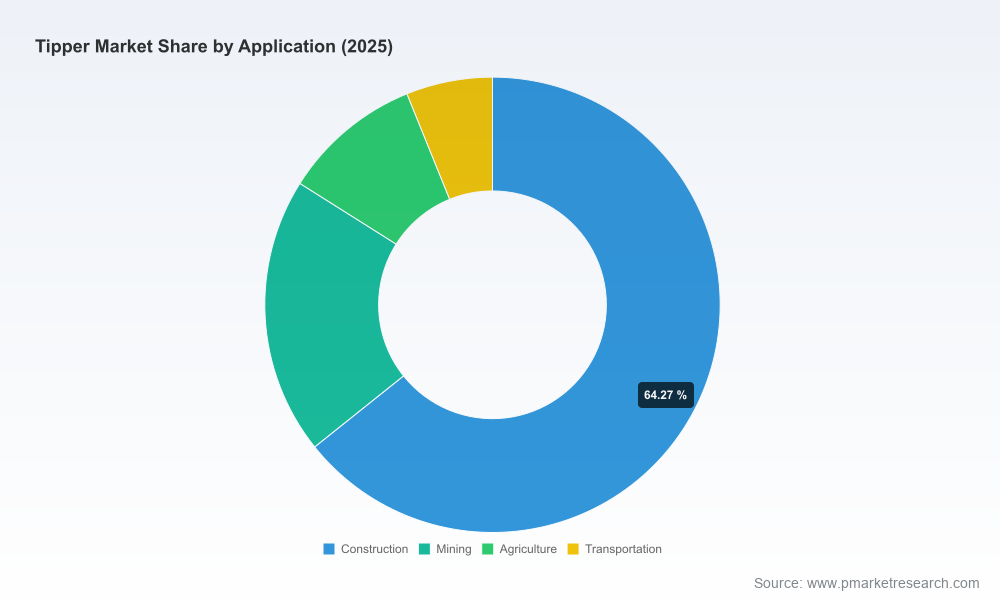

Tipper Market

Timing capital: With the market having expanded consistently through 2020–2025 and continuing to grow under our baseline 4.8% CAGR, the window for cost‑efficient capacity additions and fleet renewals is narrowing. Delayed capex decisions will face a different cost and supply environment by mid‑2026 as demand pockets firm and steel market signals normalize.

Tipper Market

Procurement and tender readiness: Public and private tenders are continuing to surface in 2026, from municipal fleets to mining operator requirements. Being tender-ready — with compliant, pre‑qualified suppliers and validated technical specs — materially shortens delivery lead times and reduces price exposure.

Tipper Market

Supply‑chain volatility: Recent industry data highlights nuanced pressure points in raw materials and regional steel production. Short‑run shifts in global steel output and tariff dynamics are amplifying supplier risk; procurement strategy must bridge near‑term availability with medium‑term pricing uncertainty.

We designed the report as an operational playbook for 2026. It goes beyond narrative and contains the working tools teams can use in decision windows this year, including:

We intentionally present this as a “preview”: the full report consolidates the granular regional, type and application splits, the vendor scorecards and the downloadable financial models that enable immediate operationalisation.

The tipper market’s competitive structure combines regional specialists and established global OEMs. Market concentration metrics point to a mid‑to‑high consolidation level among top suppliers, creating both entry barriers for new challengers and opportunities for specialised players to command niche margins. Below we outline strategic positions and near‑term moves for select participants that matter for 2026 planning.

PRBB Trailers (Pretoria, South Africa) — A regional manufacturer focused on side‑tipper configurations for mining and bulk transport. Their proximity to mining operations and expertise in side tipping bodies positions them well for operators prioritising tailored local service and short delivery windows. Strategic opportunity: partnerships with global OEMs for southern Africa aftermarket coverage and OEM‑level warranties to capture larger fleet upgrade programmes.

SA Trailers (Australia) — Known for custom builds and deep local supply chains. Compliance with Australian design and ADR standards and an established component network gives them an advantage in domestic tenders, particularly in mining‑heavy states. Strategic opportunity: leverage local sourcing to structure nearshoring options for international buyers seeking ADR‑compliant solutions.

Schmitz Cargobull (Germany) — A European leader with lightweight aluminium and heavy‑duty steel body options. Strong brand, broad distribution and engineered variants make them a preferred supplier for customers balancing payload optimisation with lifecycle cost. Strategic risk: exposure to EU demand cycles and steel input price volatility.

MEILLER Fahrzeug‑ und Maschinenfabrik (Germany) — Specialised in heavy‑duty tipping mechanisms and rapid‑cycle systems. Their mechanical innovations are most valued where operational uptime and tipping throughput translate directly into operator revenue. Strategic opportunity: technology licensing and retrofit programmes targeting larger fleets.

Lider Trailer & Tanker and Nova Trailer (Turkey) — Both Turkish manufacturers focus on high‑capacity tipper semi‑trailers and abrasion‑resistant bodywork. Their cost competitiveness and use of high‑hardness steel variants make them alternatives for large bulk transport and scrap handling. Strategic move: western expansion via distribution partnerships and targeted certification to reduce buyer switching costs.

Ashok Leyland (Chennai, India) — A major truck OEM entering or expanding tipper offerings with new models (notably product upgrades announced in early 2026). Their scale and local manufacturing footprint make them a compelling partner for fleet operators in price‑sensitive markets seeking integrated truck‑and‑body solutions. Strategic proposition: bundle offerings with financing and aftermarket packages to win volume contracts.

Raw materials: Recent short‑range outlooks and production data indicate modest changes in steel demand and supply dynamics in 2026. Small percentage shifts in global steel output and demand translate into meaningful cost movements for tipper manufacturers because steel forms a large share of bill‑of‑materials weight. Hedging raw material exposure and negotiating index‑linked supply contracts should be core procurement tactics in 2026.

Regulatory and trade policy: Regional regulatory frameworks and tariff actions continue to shape competitive advantage. In Europe, delayed rebounds and tariff dynamics are weighing on OEM orderbooks; meanwhile, local certification standards (for example, ADR compliance requirements in Australia) are decisive in procurement evaluations.

Labour and component sourcing: Several manufacturers source critical components locally to control lead times. For buyers, a supplier’s domestic sourcing footprint is now as important as headline price — especially for tenders with tight delivery schedules.

Fast‑track vendor pre‑qualification: Prioritise suppliers with demonstrated local support, compliance credentials and spare‑parts logistics mapped to your deployment windows.

Adopt a staged procurement plan: Use modular win‑back clauses and staged deliveries to manage both price and delivery risk as market conditions evolve.

Lock in critical inputs where possible: Negotiate short‑to‑medium term supply agreements indexed to steel movements rather than spot purchases to reduce margin erosion.

Evaluate M&A and partnerships selectively: For OEMs and investors, regions with fragmented supply bases present opportunities to consolidate aftermarket networks or to secure scale in manufacturing capacity before the market upswing accelerates.

Operationalise tender intelligence: Use an active tender tracker and compliance checklist to convert pipeline opportunities into wins — the recent municipal and mining tenders observed in 2026 illustrate the value of being pre‑positioned.

This article is a strategic preview. The complete PW Consulting Tipper Market report includes the granular regional and application segmentation, detailed vendor scorecards, downloadable financial models and a live tender calendar that procurement teams can deploy immediately. We deliberately withhold the segment‑level tables and raw contact lists here to ensure decision‑makers access the full dataset and tools on our secure platform — where you can also licence the models for internal use.

For 2026, the question isn’t whether the market will change, but how prepared your organisation is to capture the opportunity or mitigate the downside. PW Consulting’s full report is structured to convert market intelligence into executable plans — from procurement playbooks and bid‑readiness tools to M&A theses and cost‑management templates.

To discuss how the report’s tools can be tailored to your specific fleet, tender pipeline or investment mandate, contact our industry team at PW Consulting. In a market moving at a steady CAGR and with clear structural signals for the medium term, speed and clarity of action will be the differentiators between incremental outcomes and strategic advantage.

For detailed analysis of this topic, please visit the official page:Tipper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com