Global Superfruits Market Competitive Analysis and Industry Outlook 2026–2034

Food |

2026-07-02 12:55:41

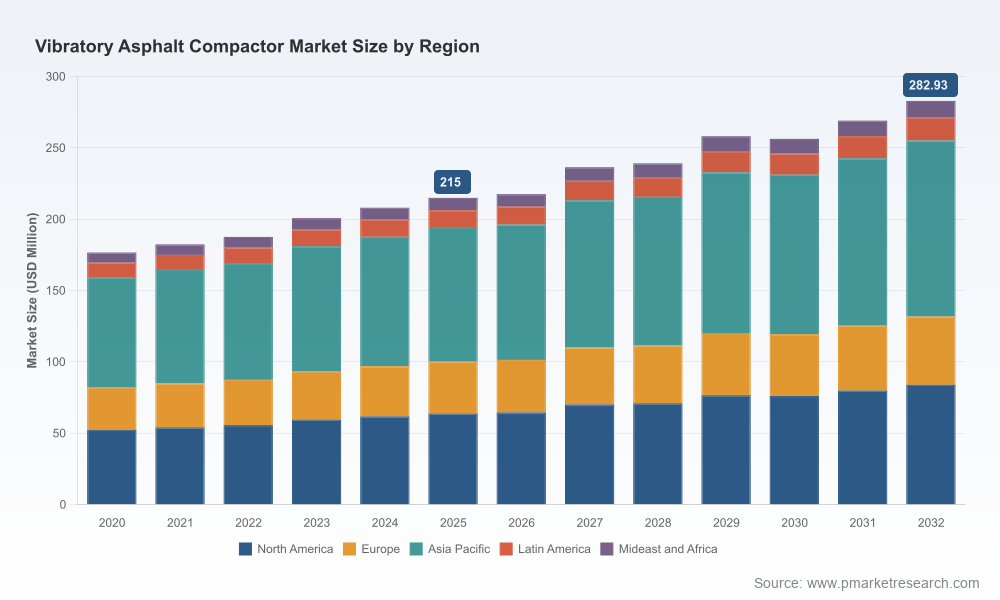

PW Consulting’s latest industry brief on the Vibratory Asphalt Compactor market is designed as a decision-grade input for strategy teams, product leaders, and corporate development groups planning actions in 2026. Built on a 2020–2025 historical base (base year: 2025) and a 2026–2032 forecast horizon, the study combines a granular understanding of equipment dynamics with pragmatic recommendations for go-to-market, R&D prioritization, and M&A. At the macro level, the market expanded from a mid-hundreds USD Million base in 2020 to approximately USD 215.0 Million in 2025 and is projected to grow at a 4.04% CAGR through 2032 to a forecasted market size near USD 283 Million. Market concentration is material — the top three manufacturers account for roughly seven in ten dollars of the market, and the top five approach eight in ten — an important structural factor for competitive strategy.

Vibratory Asphalt Compactor Market

Timing: 2026 is a pivot year when intelligent compaction standards, digital tooling, and customer procurement practices converge. Early movers can capture disproportionate share through bundled hardware + data offerings.

Vibratory Asphalt Compactor Market

Resource allocation: The market’s steady mid-single-digit CAGR implies that incremental share gains are achieved through product differentiation and channel optimization rather than volume-driven commodity plays.

Vibratory Asphalt Compactor Market

Risk management: Regulatory alignment (intelligent compaction standards for asphalt) and evolving specifications from public owners create both compliance costs and opportunities for premium service positioning.

Deal-making: High concentration at the top makes targeted acquisitions of niche technology suppliers and regional players a compelling route to scale features and fill capability gaps quickly.

Our analysis identifies three converging forces that will determine winners and losers over the next three years:

Technical evolution of compaction platforms — increased use of dual-frequency double-drum systems, variable amplitude control, and machine-integrated density sensing is allowing operators to tune compaction energy to mix designs. These capability differentials translate directly to field-level productivity and lifecycle pavement performance.

Data and automation — intelligent compaction standards (established regulatory frameworks and best practices) plus vendor-led telematics and on-machine measurement are shifting value from pure equipment throughput to measurable quality outcomes. Vendors that translate machine data into prescriptive workflows for operators will secure pricing power and recurring revenue.

Market structure and procurement — centralized procurement by public agencies and an active rental ecosystem mean OEMs must offer diverse commercial models (outright sale, rental partnerships, performance warranties tied to measured density) to defend and grow share.

The market structure is characterized by a small set of global OEMs with strong product portfolios and broad distribution networks, complemented by regional and low-cost manufacturers that compete on price and availability. Leading OEMs in the global set include established European, North American, and Japanese manufacturers with differentiated engineering approaches and growing digital stacks. Notable market participants include BOMAG, Wacker Neuson, Hamm AG, Dynapac, Caterpillar, Ammann Group, Volvo Construction Equipment, Hitachi Construction Machinery, and a number of Chinese OEMs supplying high-tonnage rollers.

Strategic implications for incumbents and challengers:

Incumbents: Leverage installed base and telematics to monetize aftermarket services and data products. Protect margin by bundling sensors, fleet analytics, and operator training tied to improved compaction outcomes.

Challengers: Focus on niche value propositions — cost-competitive high-tonnage machines for specific regional mixes, or lean, retrofit-compatible smart packages that enable older machines to comply with intelligent compaction workflows.

New entrants / software firms: Pursue OEM partnerships and channel-led pilots; software that closes the loop from machine sensor to actionable operator guidance is a natural acquisition target for OEMs looking to accelerate differentiation.

Vendor-level motion over 2024–2026 indicates acceleration in embedded sensing and operator assistance:

Hamm AG’s product cadence — including the introduction of an on-machine density measurement system in 2025 and subsequent automation suites announced for 2026 — exemplifies the strategic trajectory: merging hardware improvements with software-enabled control and operator workflow enhancements.

Other OEMs continue incremental hardware innovation (drum designs, frequency/amplitude control) and telematics evolution to support fleet-level productivity measurement and preventive maintenance — activities that compress the time-to-value for customers adopting smart compaction.

Based on our scenario modeling and customer interviews, the following strategic plays offer differentiated returns relative to the incumbent cost of capital and competitive intensity:

Product + data bundling: Convert one-time equipment revenue into multi-year service streams by packaging sensor subscriptions, compaction analytics, and certification reports for public owners.

Operator augmentation: Invest in operator-assist features (automated track assist, roll sequencing guidance) that lower training costs and improve first-pass compaction—an area with demonstrable ROI for contractors.

Channel partnerships with rental houses: Structure shareable fleet solutions with clear commercial terms around utilization and wear to capture the growing rental demand for short-duration projects.

Targeted M&A / minority investments: Identify software firms or sensor vendors that enable predictive quality guarantees. Small acquisitions can shortcut multi-year internal development cycles.

Regulatory engagement: Proactively certify solutions against intelligent compaction standards and partner with public agencies on pilot projects to become the preferred supplier for projects with strict compaction specs.

The full report is structured to be operationally useful for commercial planning, product road-mapping, and transaction diligence. Key deliverables include:

Top-down and bottom-up market sizing models (historical 2020–2025; forecast 2026–2032) with scenario sensitivity and unit-volume translation logic.

Competitive profiles and capability heatmaps for leading OEMs (engineering attributes, digital maturity, channel strength), and a mapped view of supplier dependencies across critical subsystems (drums, vibration systems, sensors).

Buyer decision frameworks and procurement playbooks for contractors and public owners, including TCO templates, specification checklists, and performance-based contracting language examples.

Go-to-market and pricing playbooks for OEMs and distributors, including rental partnership structures and service-tier architectures.

Technology adoption roadmap for smart compaction and automation, with a prioritized list of pilot use-cases, expected payback periods, and operator training outlines.

Investment memo templates and a short-list of targets for inorganic growth (technology suppliers, regional OEMs, and data analytics firms). Note: transaction-ready valuations, target-level revenue splits, and sensitive segment tables are available in the paid dossier.

Primary research appendices (interview transcripts, supplier questionnaires, and methodology notes) to support executive and investment due diligence.

For fast-moving teams, we recommend a three-step 90–180 day activation plan:

90 days — Pilot and validate: Deploy one or two machine-level pilots focused on real-time density measurement and operator assist; evaluate performance uplift and reconcile to cost and rental utilization models.

120 days — Commercialize and price: Create a bundled product offering with subscription terms and pilot a rental partnership that shares upside from improved compaction outcomes.

180 days — Scale and partner: Negotiate channel agreements with rental firms and public owners, and begin integration talks or small acquisitions to close identified capability gaps.

This preview is intentionally selective: it demonstrates the rigor of our modeling and the strategic lens we apply while withholding proprietary segment-level tables and recommended target lists to preserve client value and confidentiality. Teams that need executable playbooks, downloadable financial models, and full competitive scorecards will receive the complete segmented datasets, supplier scorecards, and transaction-ready recommendations in the full PW Consulting report.

To obtain the full report and interactive spreadsheets that power our 2026 strategic recommendations, contact PW Consulting or access the report landing page for licensing and custom engagement options.

For detailed analysis of this topic, please visit the official page:Vibratory Asphalt Compactor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com