Cold Planers Market 2026: Strategic Imperatives for Executives — A PW Consulting Preview

As PW Consulting’s Chief Industry Analyst, I present a focused preview of our Cold Planers Market research designed to inform executive decisions in 2026. Based on a 2025 base year and a seven‑year forecast horizon (2026–2032), the global market has expanded from approximately USD 2.05 Billion in 2020 to USD 2.65 Billion in 2025 and is projected to continue growing to around USD 3.80 Billion by 2032, reflecting a compound annual growth rate (CAGR) of roughly 5.3% over the forecast period. These headline dynamics matter: they place cold planers squarely in the “steady growth, strategic importance” bucket for infrastructure OEMs, rental fleets, municipal procurement, and aftermarket players.

Cold Planers Market

Why this research matters for 2026 decision-making

Leaders need more than market size and a growth rate. They need operational levers, competitive positioning, and scenario-proofed strategies. Our report delivers exactly that — a compact playbook that translates the market’s macro momentum into concrete choices across procurement, product roadmap, aftermarket economics, and M&A screening. This preview highlights the strategic takeaways while preserving the granular segmentation and models that are accessible through the full report.

Cold Planers Market

Key market signals and what they mean

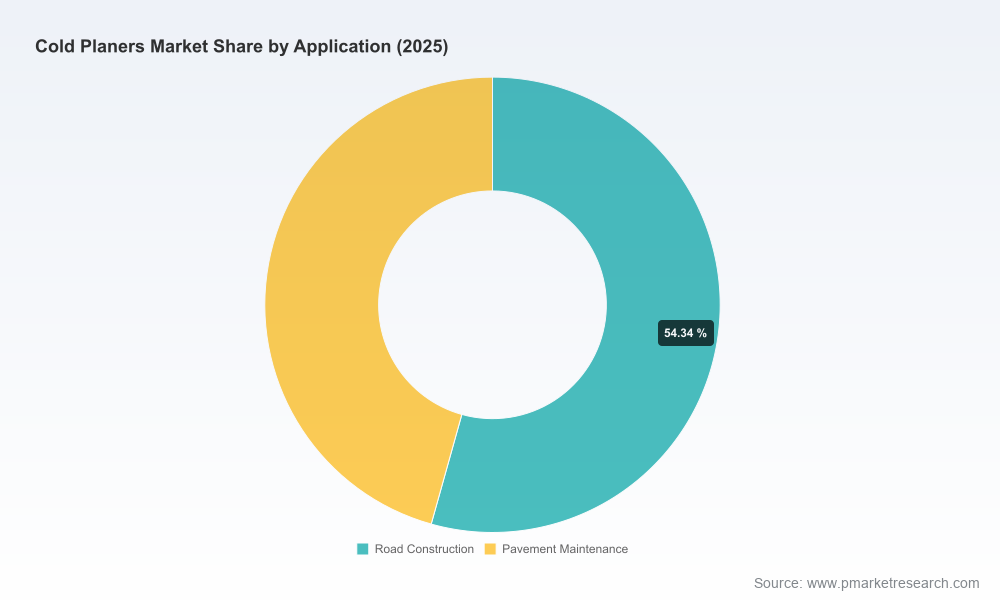

- Steady expansion with tactical inflection points: The sector’s mid-single-digit CAGR masks pockets of accelerated demand tied to infrastructure stimulus, municipal resurfacing cycles, and rising pavement maintenance budgets. Organizations that time fleet refreshes to coincide with local capex waves capture outsized utilization gains and resale values.

- Fragmented supplier landscape = opportunity: Market leadership is not monopolistic; the landscape remains sufficiently fragmented that differentiated product features, service networks, and financing options materially shift share. This fragmentation favors specialist suppliers, attachment manufacturers, and aggressive MRO (maintenance, repair, overhaul) strategies.

- Cost volatility layers strategic risk: Raw material signals — for example, observed cold‑rolled coil pricing dynamics in early‑to‑mid 2026 and broader downward pressure on steel through 2026–2027 — influence OEM margins and aftermarket spare pricing. Buyers and OEMs should model procurement clauses and hedging options into 2026 sourcing contracts.

- Regulatory and occupational safety pressures: Compliance obligations (notably respirable crystalline silica controls during milling) and stricter municipal quality/reclamation codes elevate the value of systems that reduce exposures, automate controls, and document compliance trails.

What practical, decision‑grade tools the report contains

Executives and program managers tell us they need immediately implementable tools. The full PW Consulting study includes:

Cold Planers Market

- Robust market-sizing methodology and downloadable sizing model (base 2025, forecast 2026–2032) that supports “what‑if” scenario runs.

- Procurement playbook with TCO (total cost of ownership) templates, lifecycle replacement triggers (benchmarked by operating hours and age), and vendor negotiation checklists.

- Aftermarket and parts strategy maps including service margin models, critical spare lists, and spare‑parts lead‑time sensitivity analyses.

- Site‑level exposure & compliance checklist for silica and municipal code adherence — designed for operations, safety officers, and procurement.

- Competitive benchmarking framework and supplier scorecards with detailed product capability matrices (teaser below; full matrices in the report).

- M&A and partnership screening criteria tied to volume synergies, geographic expansion vectors, and channel consolidation scenarios.

Competitive landscape — capability clusters to watch

The cold planers market is populated by well‑known global OEMs and focused attachment specialists. In our analysis we group competitive capabilities into clusters — heavy‑duty mainline millers, compact and skid‑steer attachments, and modular aftermarket specialists. Representative players and their strategic focus include:

- Caterpillar Inc. (Irving, Texas) — Offers a broad PM series line with models emphasizing advanced grade‑control systems and operator ergonomics. Recent updates have improved visibility, safety lighting, and quick‑change mount options that shorten set‑up time.

- Wirtgen Group (Windhagen, Germany) — Continues to push performance per footprint with new high‑performance compact millers that incorporate automated tracking and productivity telematics; recent world‑premiere introductions emphasize CO₂ and efficiency narratives.

- BOMAG GmbH (Boppard, Germany) — Focused on adaptability across road resurfacing projects; product lines stress selectable discharge arrangements and ease of integration for selective milling operations.

- Dynapac AB (Stockholm, Sweden) — Positions its cold milling machines around efficient pavement removal for both commercial and large infrastructure overlays, optimizing throughput and fuel efficiency.

- Erskine Attachments (Alexandria, Minnesota) — Specialized in skid‑steer mounted planers that target road repair, bridge deck prep and utility cut‑ins, a growth niche for rental fleets and municipal crews.

- RoadHog, Inc. (USA) — Offers hydraulic cold planers suitable for compact loaders and skid steers, stressing modular cutting widths for urban and tight‑access milling.

Recent manufacturer activity underscores competitive dynamics. Wirtgen’s world premiere of a compact high‑performance model at a major trade show in early 2025 signaled product‑led differentiation. Caterpillar’s mid‑2025 updates emphasized operator safety and serviceability — a direct response to procurement requests for machines that lower on‑site risk and downtime. Additionally, attachment showcases from specialized fabricators continue to blur the line between OEM machines and third‑party productivity solutions.

Cost, lifecycle and regulatory dynamics that will drive buyer behavior in 2026

- Raw materials and procurement: Short‑term raw material price moves — for example, cold‑rolled coil pricing observed in early 2026 — transmitted directly into OEM quoting practices and spare‑parts catalogs. Steel price forecasts pointing to moderation in 2026–2027 reduce one input risk but create a timing arbitrage for buyers who can defer purchases or negotiate indexed pricing.

- Lifecycle economics: Empirical benchmarks indicate a typical cold planer lifetime at roughly 5,000 operating hours (or around five years before trade‑in for many fleet profiles). Align replacement policies and warranty structures to this rhythm to avoid unplanned costs.

- Health & safety / municipal codes: Compliance with respirable crystalline silica controls and local milling standards will premium machines that either reduce exposures or provide verifiable control measures. Expect procurement tenders to score equipment on compliance documentation and integrated control features.

Three strategic moves for 2026

- Refinance and align fleet refresh cycles: For rental companies and municipalities, structuring refresh plans around the 5,000‑hour lifecycle, indexed parts pricing, and available OEM financing reduces total ownership cost and improves uptime.

- Invest in data & compliance features: Equip new purchases with telematics and automated logging for both productivity and compliance. Buyers that can report productivity per shift and exposure controls win competitive tenders.

- Target aftermarket capture: OEMs and distributors should accelerate spare‑parts availability, quick‑change tool carriers, and local service footprints. The aftermarket represents the highest margin lever and the most defensible revenue stream against commoditization.

How PW Consulting helps — the actionable edge

Our full Cold Planers Market report translates the above into executable steps: ready‑to‑use procurement RFP language, a downloadable TCO model pre‑populated with base‑case inputs (2025 baseline), vendor scorecards, and scenario playbooks mapping demand shocks to inventory and service capacity. Importantly, the detailed segmentation by region, machine type, and application — including granular shares, pricing bands, and channel economics — is intentionally withheld in this preview to protect the strategic value of the underlying intelligence. That granular data and the interactive models are available through the report landing page.

Next steps for executives

If your 2026 strategy hinges on fleet optimization, margin expansion in aftermarket services, or a targeted acquisition to accelerate presence in a high‑value niche, this research is designed to shave months off your diagnostic phase and deliver decision‑grade options in weeks. Access the full study for the complete segmentation, downloadable financial models, and our extended supplier capability matrices that show where to allocate resources for maximum ROI.

PW Consulting stands ready to support customized scenario workshops, bid‑support for major procurements, and commercial diligence for M&A opportunities surfaced by the report. Contact details and the full report access are available on our publication page.

For detailed analysis of this topic, please visit the official page:Cold Planers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com