Coating (Painting) Additives Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Chief Industry Analyst, I present a focused executive introduction to our new market study on Coating (Painting) Additives. This briefing synthesizes the macro trajectory, competitive topology, regulatory and raw-material dynamics, and the concrete, decision-grade outputs that senior executives and strategic teams must have in 2026. It is designed as a high-value “trailer”: it demonstrates analytical depth and immediate practical relevance while reserving the detailed subsegment tables and proprietary scenario matrices for the full report.

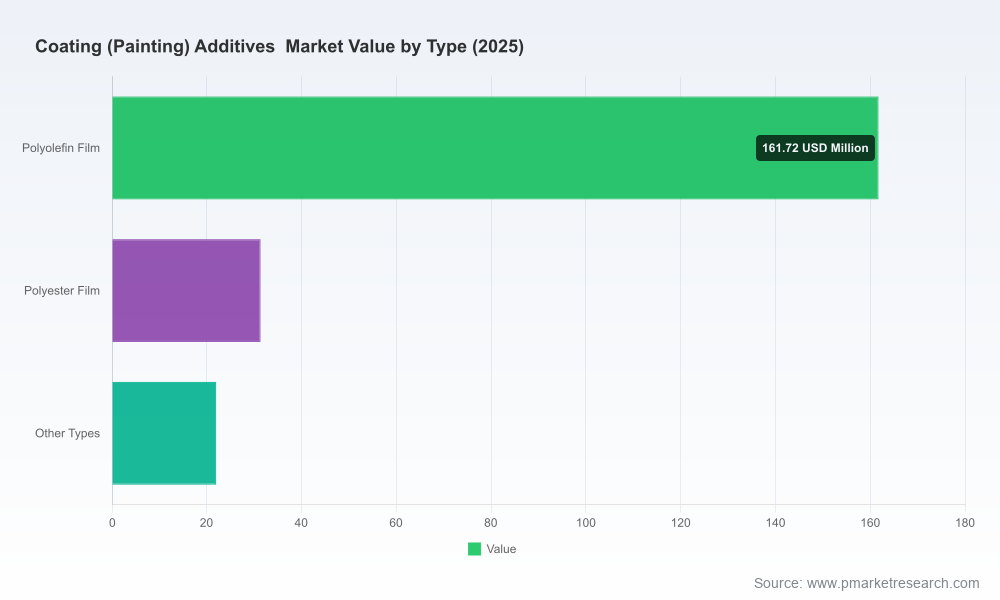

Coating (Painting) Additives Market

Market snapshot: What the macros tell you

By the close of our base year (2025), the global coating additives market had grown materially since 2020, reflecting steady demand across architectural, industrial and specialty coatings. Our historical sizing shows a clear recovery-and-acceleration pattern in 2021–2025, driven by formulation innovation, increased adoption of functional additives, and rising downstream activity in construction, automotive refinishing, and selected industrial end-markets.

Coating (Painting) Additives Market

Looking forward, our forecast period (2026–2032) assumes a compound annual growth rate (CAGR) of 6.98%, producing a materially larger market by the end of 2032. This growth reflects both broader coatings volume expansion and a premiumization trend — formulators buying more advanced additive chemistries to meet performance, sustainability, and regulatory constraints. The markets remain fragmented: the three- and five-firm concentration ratios are low, underscoring a competitive environment with many specialist and regional suppliers alongside a group of global leaders.

Coating (Painting) Additives Market

Why 2026 is a strategic inflection point

- Regulatory and product convergence: Accelerating low-VOC, bio-based and food-contact approvals are re-shaping formulation roadmaps. Early adopters of compliant chemistries capture formulation wins with downstream coaters and brand owners.

- Raw-material volatility: Recent spikes in key inputs such as pigment and monomer feedstocks have raised COGS pressure and forced procurement re-engineering.

- Technology differentiation: Dispersants, rheology modifiers and hyperdispersants for radiation-curing systems have opened new niches for margin expansion.

- Strategic consolidation opportunity: Fragmentation offers M&A playbooks: bolt-ons that add formulation breadth in waterborne or specialty curing technologies can deliver immediate cross-sell.

Top near-term market dynamics to monitor

- Supply-side investment and capacity moves: Global players are selectively expanding production lines in response to advanced dispersant demand and localized supply chains — expect targeted capacity additions rather than broad overbuild.

- Regulatory wins as commercial levers: Bio-based and food-contact approvals are not only compliance milestones but commercial differentiators when selling into sensitive end-markets.

- Upstream cost transmission: Recent commodity price actions across pigments and acrylic building blocks have shortened the transmission lag into finished-additive pricing, creating transient margin squeezes that require tactical pricing and procurement hedges.

- Innovation-driven pockets of premiumization: Specialty additives for low-odour, rapid-cure, and high-durability coatings are growing faster than the market average, opening routes to higher ASPs.

What the PW Consulting report delivers — operationally usable outputs

The full study is organized to support immediate 90–365 day decision cycles and longer-term strategic planning. Key deliverables include:

- Top-down market sizing and scenario-led forecasts (base year 2025), with sensitivity to demand, price, and raw-material pathways.

- Price and cost modeling tools that let procurement and finance teams model TiO₂, monomer and pigment pass-throughs under alternative market conditions.

- Supply-chain maps and supplier risk heatmaps highlighting single-point-of-failure exposures and regional logistics constraints.

- Technology and formulation matrix showing where incremental additive investments unlock outsized customer value (e.g., low-VOC rheology modifiers, radiation-curing dispersants).

- Commercial playbooks: channel strategies, premiumization tactics, and specification-play templates for engaging formulators and coaters.

- Competitive scorecards and capability benchmarking across product breadth, formulation support, production footprint, and regulatory credentials.

- M&A screening lists and valuation heuristics tailored to buyers seeking scale or capability buys in specialty and regional segments.

- 100‑, 250‑ and 500‑day tactical plans for cost containment, procurement hedging, and go-to-market pivots.

Competitive landscape — who matters and why

The market structure is a two-speed environment: a cohort of global specialty chemical leaders and a broad field of regional, formulation-focused players. Global leaders tend to combine deep R&D, formulation science, and global manufacturing reach; regional players compete on speed, local service, and bespoke formulations. Our competitive intelligence focuses on the strategic posture of the following companies:

- BYK/ALTANA: A leader in wetting agents, defoamers and rheology modifiers with strong application support for architectural and industrial coatings. Their strength is formulation know-how integrated with analytical instruments — a classic “solution-plus-instrument” proposition.

- BASF: Broad portfolio and scale; active investment in bio-based and low‑VOC wetting technologies and selective capacity expansions aimed at high-performance dispersants. Their play is global breadth plus regulatory alignment.

- Evonik: Focused on high‑performance additives under established brand platforms, with targeted innovations for radiation-curing and specialty solventborne applications.

- Clariant: Niche leader in performance additives with an emphasis on eco‑label-compliant solutions and recent regulatory approvals that open sensitive end-markets.

- Large integrated chemical players (Dow, Arkema, Eastman, Nouryon, Ashland, Elementis, Lubrizol, Momentive): These firms are differentiated by global supply chains, synergies with adjacent chemistries, and scale advantages in raw-material negotiation.

- Regional and specialist players (e.g., Raj Speciality Additives and others): Provide agility and price-competitive offerings for local coaters; important acquisition targets for buyers seeking channel access.

Notably, the market remains fragmented (low three- and five-firm concentration ratios), which creates both pricing pressure and M&A runway. Recent industry events — new performance additive launches, supplier recognitions, and targeted awards — underline the intense product-led competition and the value of owning formulation IP.

Raw materials, regulation, and near-term headwinds

- Input-cost shocks: The sector has seen cascading cost pressure from pigment and monomer markets; procurement teams must adopt multi-scenario hedging and indexed contracting to protect margins.

- Regulatory tightening: Low-VOC and bio-based compliance regimes are accelerating. Firms without an explicit regulatory roadmap risk lost specification share in high-value end-markets.

- Localized supply risk: Strategic expansions and site investments are concentrated in nodes where advanced dispersants and polymeric additives are demanded; footprint optimization is now a competitive lever.

Strategic playbook for 2026 — actions that separate winners from followers

- Product-led differentiation: Prioritize R&D in hyperdispersants, low-VOC wetting systems, and radiation-curing additives that unlock premium margins.

- Procurement sophistication: Implement granular cost-to-serve analytics, dual-sourcing for critical intermediates, and dynamic pricing mechanisms that reflect upstream volatility.

- Go-to-market refinement: Build formulation labs near strategic customers, offer co-development and trial programs, and shift part of commercial incentives to performance-linked models.

- M&A and partnerships: Pursue bolt-ons that add formulation IP or regional channels rather than low-value capacity buys. Partnerships with pigment and resin suppliers can secure feedstock continuity.

- Regulatory and sustainability positioning: Translate approvals and eco‑credentials into specification wins; use them as a premium feature in bids for food-contact and regulated industrial contracts.

Implications for 2026 corporate planning

Executives preparing 2026 budgets and strategic plans should treat coating additives not as a commodity wedge but as a technology-enabled margin lever. The market’s expected mid-single-digit CAGR over the forecast period presents attractive organic growth prospects, but achieving outperformance requires coordinated investment across R&D, procurement, and commercial functions. For acquirers, the fragmentation and low concentration ratios imply attractive returns on roll-up strategies that combine formulation expertise with regional distribution.

Next steps — how to use the full PW Consulting study

The companion full report contains the detailed subsegment breakouts, proprietary scenario models, supplier scorecards and the confidential valuation matrices that we intentionally withhold here. If your 2026 planning requires:

- Granular subsegment demand and pricing trajectories;

- Custom sensitivity runs on TiO₂ and acrylic feedstock price scenarios;

- Ready-to-execute M&A target lists and commercial due diligence templates;

- Site-level capex optimization and tax-efficient footprint recommendations;

— PW Consulting can provide the full study and bespoke briefings. Contact our advisory team to schedule a strategic workshop that aligns the report’s tactical outputs with your 90–365 day implementation milestones.

In sum: the coating additives market offers a compelling combination of steady volume growth and pockets of high-value innovation. The strategic choices you make in 2026 on technology investment, procurement architecture, and M&A posture will determine whether your organization captures the premium opportunities this expansion creates. Our full study is structured to convert those choices into executable plans.

For detailed analysis of this topic, please visit the official page:Coating (Painting) Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com