Water Pumps Market 2026: Strategic Primer for Executive Decision-Making

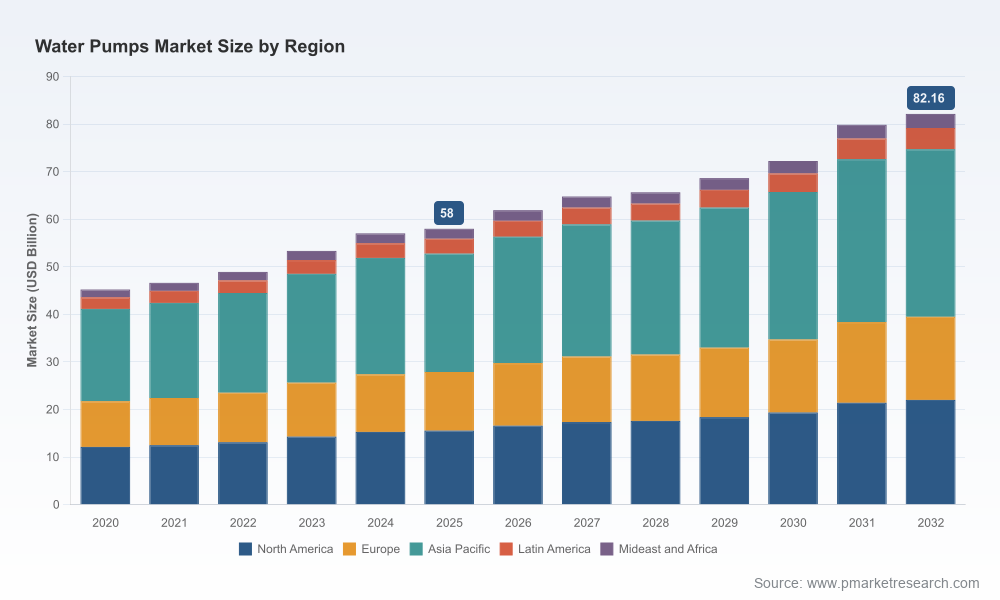

As companies finalize budgets and strategic plans for 2026, the global water pumps market is entering a phase where incremental growth intersects with structural transformation. Our PW Consulting market study — anchored on a 2025 base year with a historical view through 2020–2025 and forecasts to 2032 — tracks this evolution quantitatively and translates it into operational choices executives must make now. The market expanded from the mid‑40s (USD Billion) in 2020 to roughly USD 58.0 Billion in 2025 and is expected to approach the low‑80s by 2032 under a normalized compound annual growth rate of about 5.1%. These headline metrics underscore steady demand but mask heterogeneity across product types, end‑use applications and geographies — the same heterogeneity that will determine winners and losers in 2026 and beyond.

Water Pumps Market

Why this report matters for 2026 planning

- Timing: 2026 will be the first full planning year after several regulatory and technology inflection points (energy efficiency standards, PFAS-related drinking water regulations, and national incentive programs) have begun to materially reshape procurement specifications and TCO calculus.

- Investment prioritization: With moderate overall market growth, margin expansion will come from efficiency gains, digital services and aftermarket capture rather than volume alone. Companies must choose where to allocate constrained R&D, manufacturing and M&A capital.

- Risk management: Supply‑chain localization mandates and raw material policies are raising the political-economic risk profile of cross‑border sourcing — a key consideration for firms with global footprints.

Market dynamics that will shape 2026 decisions

The report synthesizes macro forces into five decision levers executives can use to stress‑test their 2026 plans:

Water Pumps Market

- Regulatory acceleration on efficiency and water quality: Recent U.S. Department of Energy pump efficiency mandates and the finalization of PFAS drinking water standards have already altered technical specifications and procurement evaluation criteria. Expect EPCs, utilities and large industrial users to demand higher‑efficiency units and validated contamination‑resilient solutions.

- Energy and operating cost focus: With energy accounting for a large share of lifecycle cost, energy‑savings claims are now table stakes. The Bureau of Energy Efficiency’s programs and similar national initiatives are driving adoption of premium‑efficiency pumps and controls in emerging markets as well as developed ones.

- Supply‑chain localisation and procurement rules: Policies like the Build America, Buy America framework are changing the calculus for where to manufacture iron, steel and assembled products used in public infrastructure, increasing the value of regional manufacturing capacity.

- Service and digitalization as margin engines: Predictive maintenance, remote monitoring and outcome‑based contracts are creating aftermarket revenue streams that materially outperform new‑equipment margins. Digital features are also becoming a gating factor in competitive tenders.

- Fragmented competitive structure: The market is moderately fragmented — the largest three firms account for roughly a quarter of the market and the top five for about one‑third — which leaves room for focused consolidation, vertical integration by large OEMs, and regional champions to expand.

Technology and product strategy: where to allocate R&D in 2026

Given the interplay of efficiency standards and buyer expectations, companies should prioritize three development threads in 2026:

Water Pumps Market

- Hydraulic optimization and novel materials to meet evolving DOE thresholds while lowering lifecycle operating expense.

- Integrated control systems and digital services enabling condition‑based maintenance and remote performance guarantees.

- Modular designs that reduce localization costs and accelerate time‑to‑market for regionally manufactured variants.

Recent product and model launches illustrate these priorities in practice. For example, leading manufacturers continue to introduce next‑generation hydraulics designed for high efficiency and low solids handling, while new smart, cordless pump controllers have started to expand addressable domestic and small industrial segments.

Supply chain, manufacturing footprint and localization

2026 procurement strategies need to reflect rising non‑tariff constraints. Investments in regional capacity — whether greenfield facilities or brownfield upgrades — will be evaluated against procurement rules that increasingly favor domestically produced components for infrastructure projects. In practice, expanding local manufacturing can be both a market‑access play and a margin protection mechanism. Celebratory plant inaugurations and capacity investments by established regional players underscore how physical footprint moves from a back‑office consideration to a strategic lever.

Commercial model: winning in tenders and aftermarket

Pumps are no longer sold as purely mechanical assets. Buyers evaluate total cost of ownership, service availability, and digital assurance. Companies that align commercial teams around lifecycle propositions — combining optimized hardware, retrofittable controls, and outcome‑based service agreements — will outcompete peers who remain focused on transactional sales. For OEMs, building capability in aftermarket analytics and spare‑parts logistics in 2026 will materially shift margin profiles.

Competitive landscape — what to watch in 2026

The market is populated by established multinational OEMs, strong regional specialists, and emerging technology providers. Below is a concise perspective on the core incumbents covered in our study and how they are likely to position themselves in 2026 decisions:

- Grundfos Holding A/S (Denmark) — https://www.grundfos.com

A technology‑centric leader with deep investments in smart pumps and integrated water solutions. Expect continued emphasis on digital platforms and service bundles targeted at municipal and commercial customers.

- Xylem Inc. (United States) — https://www.xylem.com

Focused on water infrastructure and digital solutions, Xylem will leverage its systems expertise and aftermarket services to compete for utility contracts and large infrastructure programs.

- KSB SE & Co. KGaA (Germany) — https://www.ksb.com

Known for heavy‑duty industrial offerings; recent launches of next‑generation axially split volute pumps reinforce its focus on hydraulic efficiency for water and low‑solids applications.

- Sulzer Ltd. (Switzerland) — https://www.sulzer.com

A specialist in engineered pumping solutions and services for process industries. Sulzer’s strength in refurbishment and specialized applications makes it a key player in aftermarket and project‑based work.

- Pentair plc (United States) — https://www.pentair.com

Concentrates on residential and commercial water treatment and pumping systems, where integration with filtration and smart home/ building systems is a differentiator.

- ITT Inc. (United States) — https://www.itt.com

Offers engineered pumps and fluid handling systems. ITT’s client base in industrial and critical infrastructure positions it well to capture retrofit and reliability work.

- Flowserve Corporation (United States) — https://www.flowserve.com

A major supplier of industrial pumps and services. Flowserve is likely to emphasize lifecycle service contracts and engineered rotating equipment solutions.

- WILO SE (Germany) — https://www.wilo.com

Strong in building services and municipal applications, WILO’s focus on compact, smart, energy‑efficient systems positions it favorably in urban infrastructure projects.

- Ebara Corporation (Japan) — https://www.ebara.co.jp

A diversified industrial pump manufacturer with strength in reliable, long‑life equipment for utilities and construction markets across Asia.

- Kirloskar Brothers Limited (India) — https://www.kirloskar.com

A leading regional player with recent investments in capacity and new product introductions for domestic and export markets. Local manufacturing expansions will influence procurement in South Asia in 2026.

- SPX FLOW, Inc. (United States) — https://www.spxflow.com

Provides application‑specific pumps and aftermarket services, particularly in process industries that demand hygienic and precise fluid handling.

- Gorman‑Rupp Company (United States) — https://www.gorman-rupp.com

A specialist in wastewater and dewatering solutions; its niche strength will remain valuable to municipal and construction sectors where reliability under harsh conditions is required.

Notable recent developments that will influence 2026 actions

- Early‑2026 facility inaugurations and model rollouts by regional and global players signal industry confidence in demand and an emphasis on localized manufacturing and new hydraulics.

- Smart controller introductions and cordless automation products indicate a fast‑moving consumer and small‑scale commercial segment where digitization and ease of installation create new uptake pathways.

- Regulatory updates — notably efficiency standards and drinking water quality rules — are already reshaping purchase specifications and will be fully felt in 2026 procurement cycles.

What the full PW Consulting report delivers (practical contents)

The report is designed as an applied toolkit for executives. It includes:

- A quantified market model from 2020–2032 with scenario options to stress test commodity, regulatory and macroeconomic shocks.

- Segment and product roadmaps (hidden in this preview) that map technological pathways, cost curves and adoption timelines.

- A detailed competitive playbook with strengths, weakness and strategic options for each major player, plus M&A and partnership targets calibrated to 2026 objectives.

- Commercial negotiation templates, lifecycle TCO calculators and aftermarket service design blueprints that can be deployed rapidly in tender responses and boardroom decisions.

Note: This article intentionally omits the granular segmentation tables and region/application share breakdowns that are part of the full report. That detailed intelligence is essential to tactical execution and is available on the report portal for licensed subscribers.

How to use these insights in your 2026 planning cycle

- Re‑score your product pipeline against the DOE and local efficiency thresholds; defer or accelerate programs based on TCO impact rather than component cost alone.

- Prioritize investments that enable regional manufacturing flexibility or rapid customization to comply with localization rules and shorten lead times for infrastructure tenders.

- Build or buy digital aftermarket capability: the revenue uplift from services will be a critical lever to offset flat‑to‑modest equipment growth.

- Run a short list of M&A/partnership scenarios focused on regional manufacturing, controls/software capabilities, and aftermarket logistics — these moves can shift competitive position quickly in a fragmented market.

Conclusion — the strategic imperative for 2026

The water pumps market presents a classic strategic inflection: overall growth is steady, yet the rules of competition are changing rapidly due to regulation, digitization and procurement policy shifts. For executives, 2026 should be treated as a year to convert strategic direction into implementable capability: localized manufacturing footprint, superior hydraulic and controls technology, and aftermarket monetization. The PW Consulting report provides both the macro numbers and the operational playbooks to convert those choices into measurable outcomes.

To unlock the detailed segmentation, regional dynamics, and tactical templates referenced here, access the full report on our website — the granular intelligence there is designed to be used directly in budget allocation, R&D prioritization, and M&A screening for the 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Water Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com