Shwachman-Diamond Syndrome Market Insights and Growth Trends

Other |

2026-06-30 05:20:40

PW Consulting’s Luxury Travel Market study (base year 2025; forecast period 2026–2032, USD Million) arrives at a pivotal moment for executive teams that must turn premium demand into durable, defensible growth. The market has expanded rapidly since 2020 — rising from approximately USD 105.5 million in 2020 to roughly USD 188.0 million in 2025 — and our projection framework, calibrated to a 6.5% compound annual growth rate, anticipates continued expansion through 2032. This briefing previews the strategic intelligence inside the full report: it demonstrates the depth of our analysis while deliberately withholding the granular segment tables that provide commercial advantage for subscribers.

Luxury Travel Market

Two simple facts drive boardroom urgency. First, the luxury travel category is growing at a mid‑single digit CAGR, which is meaningful for margin‑rich businesses and service ecosystems that can capture premium spends. Second, the post‑pandemic demand recovery is maturing into structural change: affluent travelers are reshaping trip patterns, spending priorities and distribution preferences. For 2026 decisions — resource allocation, product investment, partnerships and M&A — the combination of steady market growth and shifting customer behavior creates both opportunity and execution risk.

Luxury Travel Market

Signal to allocate capital: a sustained market expansion means capex and product refresh cycles should be assessed on a multi‑year ROI horizon, not a short‑term bounce.

Luxury Travel Market

Signal to sequence offers: shorter trip preferences and regional demand shifts call for modular packages and flexible fulfilment rather than long fixed itineraries.

Signal to hedge policy & climate risks: border policy volatility and emerging climate mandates require operational contingencies and compliance roadmaps embedded into 2026 plans.

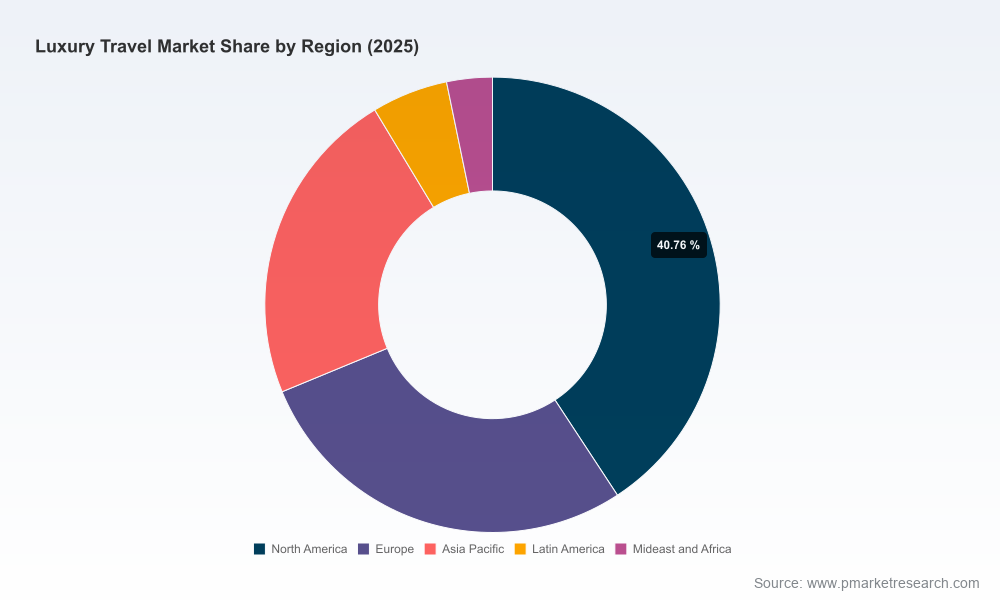

The luxury travel ecosystem remains moderately fragmented: top‑three players account for roughly one quarter of the market while the leading five combine for approximately one third. That structure creates a dual dynamic — there is scale advantage for global brands, but also sustained opportunity for nimble specialist players and platform innovators.

Marriott International — leverages a portfolio strategy across ultra‑premium brands to drive room‑nights, loyalty monetization and cross‑sell of branded experiences. Their presence at leading trade fairs underlines a continued emphasis on channel relationships and corporate demand segments.

InterContinental Hotels Group (IHG) — focuses on experiential luxury through curated brand tiers and increasing asset‑light initiatives, seeking to combine premium lodging with localized, wellness and heritage experiences.

TUI Group — integrates hospitality, cruise and curated holiday experiences, positioning itself to capture bundled spend from affluent travellers seeking seamless end‑to‑end journeys.

HBX Group — as a platform player, recently launched an AI‑enhanced ecosystem that connects advisors to high‑end hotels with end‑to‑end itinerary orchestration. This product exemplifies how data and automation are rapidly changing distribution economics in luxury travel.

Minor Hotels and Constance Hotels — represent regional premium operators that benefit from destination specialization and localized service models, important for brands scaling selectively into high‑margin resort markets.

Recent product launches and trade engagement — from platform innovations to trade show visibility — underline two competitive truths: distribution is a battleground (platforms and advisor networks matter) and brand experience is the primary source of differentiation (not purely price). The competitive field favors players who combine experiential product, high‑touch service and digitally modern distribution.

Our research translates market dynamics into operational priorities. Below are the levers that senior teams should consider prioritizing this year:

Experience Architecture: Break luxury offers into modular components (transport, private access, curated moments) so you can flex packaging to regional demand patterns and shorter‑stay preferences.

Distribution & Partnerships: Rebalance direct channels, advisor networks, and platform integrations. Invest in API connectivity and white‑label solutions for high‑value intermediaries — and evaluate partnership pilots with AI‑enabled itinerary providers.

Digital Personalization & Data Monetization: Deploy customer profiles and predictive modeling for pre‑trip upsell and post‑trip loyalty triggers. Prioritize first‑party data capture in property and charter experiences to reduce OTA dependency.

Revenue Management & Dynamic Pricing: Move beyond room‑night yield to total trip value optimization, including ancillary services, experiences, and asset use (e.g., private jets, yachts).

Sustainability & Compliance: Integrate climate regulation readiness into capital planning and supplier contracts. Consumers and regulators increasingly expect verifiable carbon strategies tied to premium pricing.

Resilience & Policy Monitoring: Build real‑time policy watchlists for visas, border changes and digital consumer protections to avoid fulfilment disruption and reputational risk.

Go‑to‑Market Speed: Use micro‑launches and rapid experimentation in key source markets to test short‑stay and regional propositions before scaling.

Strategy & Corporate Development: Use the modelled scenarios and market concentration analysis to size M&A targets and evaluate vertical integration vs. asset‑light partnerships.

Commercial & Distribution: Leverage channel elasticities and advisor ecosystem maps to reassign sales incentives and prioritize API integrations.

Product & Experience Teams: Apply persona frameworks and willingness‑to‑pay clusters for new curated offers and loyalty tiers.

Finance & Capital Allocation: Stress test investment cases under downside scenarios (accelerated policy tightening or geopolitical shocks) and upside cases (technology adoption unlocking distribution margins).

Sustainability & Compliance: Use the policy watchlist to prioritize early actions for emissions reporting and supplier compliance programmes that large corporate clients will require.

The full study contains three forward scenarios — baseline, upside and downside — all anchored to the 6.5% CAGR framework. Each scenario layers different assumptions about travel length preferences, regional substitution effects, distribution evolution and regulatory tightening (including climate mandates and digital consumer protections). We calibrate demand elasticity, pricing pass‑through and channel mix to reflect both rapid platform adoption and persistent human‑delivered experiences.

For decision‑makers, these scenarios are not theoretical exercises: they are operational stress tests. For example, a scenario combining accelerated climate regulation with restricted airlift to key long‑haul destinations materially alters asset utilization models for private charters and superyacht deployments. Conversely, a scenario where AI‑assisted itinerary platforms scale rapidly increases the addressable market for curated, high‑margin advisory services.

Proprietary, year‑by‑year market sizing (2020–2032) with downloadable model files and scenario toggles.

Segmented forecasts by region, product type and application — plus channel and distribution overlays (note: this preview intentionally omits those granular tables).

Competitive profiles and capability heatmaps for global and regional operators, including recent product launches, platform plays and trade‑fair activity.

Practical playbooks: 18 tactical initiatives with KPIs, timelines and investment envelopes calibrated for 12–36 month execution windows.

M&A & partnership decision tree and valuation sensitivities based on market concentration dynamics and margin uplift levers.

Start with the macro trendlines presented here (notably the 6.5% CAGR and the jump from ~USD 188.0M in 2025 to a materially larger market by 2032) to set top‑line assumptions for FY26. Then adopt a two‑track approach: (1) Rapid tests — launch micro‑experiments in distribution, modular experiences and AI‑enhanced advisor partnerships to gather first‑party evidence; (2) Structural moves — allocate capital to compliance readiness, systems integration and any transformative M&A identified through the report’s target screening. Use the full report to replace hypothesis with precise, table‑driven scenarios and to populate board‑level investment memos.

This briefing demonstrates PW Consulting’s strategic perspective and the practical application of our modelling. The full study adds the decisive layer you need to convert insight into action: detailed regional and application splits, downloadable financial models, and the exact matrices that market leaders and private equity teams use to make investment and M&A choices. To evaluate specific product, region or channel plays, access the full report and dataset — the granular evidence required to justify capital and commercial commitments in 2026.

For detailed analysis of this topic, please visit the official page:Luxury Travel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com