Laundry Care Market Growth with Increasing Hygiene Awareness Post-Pandemic

Other |

2026-04-21 06:50:43

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our L‑Menthol Market study — a pragmatic, decision‑oriented synthesis designed to guide corporate strategy in 2026. This preview demonstrates the analytical depth underpinning the full report while deliberately withholding the granular segmentation tables, price curves, and exact regional/application allocations so that executives and deal teams are incentivized to consult the full source for transaction‑grade inputs.

L-Menthol Market

For 2026, L‑menthol sits at a crossroads where product economics, regulatory shifts, and sustainability expectations intersect. Buyers and producers will be making capital allocation, sourcing, and portfolio decisions against a backdrop of continued growth, agricultural volatility, and shifting end‑market demand. Our research distils five high‑impact takeaways that should inform budget cycles, supply‑chain redesigns, and M&A screens in 2026:

L-Menthol Market

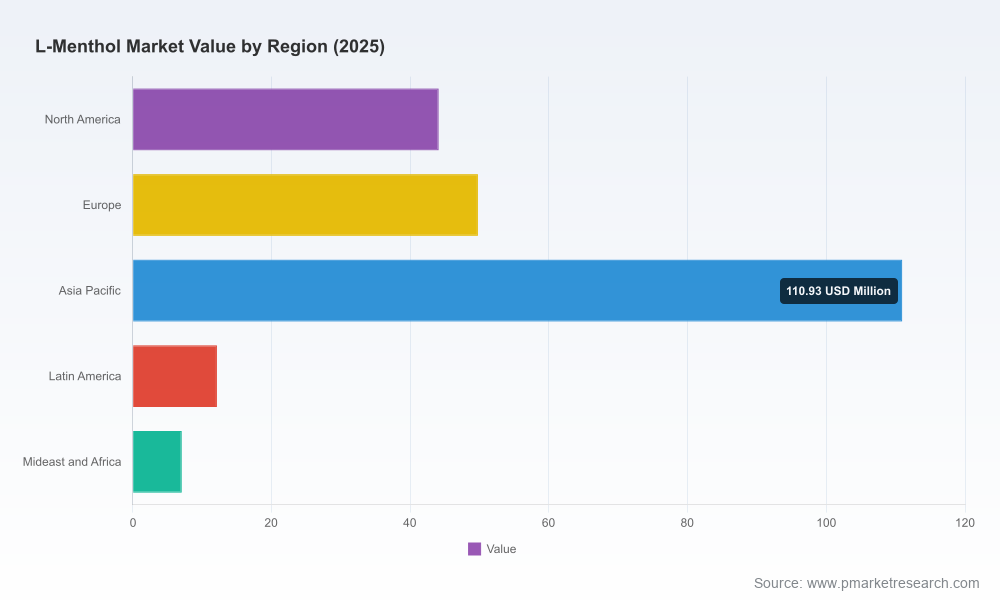

Our market model (base year 2025; historical window 2020–2025; forecast horizon 2026–2032) shows a steady expansion. The global L‑menthol market expanded through the first half of the decade and is projected to grow at a compound annual growth rate (CAGR) of roughly 4.5% over the 2026–2032 forecast period. In absolute terms, the market has grown from the low‑hundreds of USD million in 2020 to a larger base by 2025, and the forecast points toward further expansion through 2032.

L-Menthol Market

Why that matters: a 4.5% CAGR in a market with well‑established incumbents and differentiated product grades means two things for strategy. First, growth is predictable enough to justify brownfield capacity investments targeted at specialty grades (pharma‑grade flakes, low‑impurity crystals, reduced‑PCF grades). Second, the moderate growth rate increases the strategic value of operational efficiency, product differentiation, and cost‑effective feedstock strategies — rather than pure volume plays.

L‑menthol demand is being reshaped along three vectors. First, regulatory changes in tobacco markets have created demand uncertainty for tobacco‑grade menthol while accelerating demand in pharmaceutical, therapeutic, and personal‑care segments where menthol functions as an active ingredient or sensory modulator. Second, buyers increasingly value specification integrity — traceability, GMP conformity for pharma, and documented natural sourcing for “natural” grades. Third, sustainability credentials are fast becoming procurement differentiators: the launch of reduced Product Carbon Footprint (rPCF) L‑menthol products in 2025 underscores a new battleground for premium pricing.

For commercial leaders, this changes portfolio strategy. Commodity‑grade, price‑led competition is giving way to margin opportunity in pharma‑grade and sustainability‑enabled skus — but only for suppliers who can back claims with audit trails and multi‑year retention test results.

Two structural supply themes drive near‑term risk and opportunity. One is the agricultural volatility of natural feedstocks: peppermint oil pricing exhibits sharp year‑on‑year swings during crop stress periods, and seasonal yields create intermittent supply tightness. The second is the robustness of synthetic supply chains. Leading chemical houses have developed backward‑integrated synthetic L‑menthol capabilities that decouple supply from crop cycles and support multi‑year retest product formats preferred by pharma buyers.

For risk mitigation, we recommend a layered sourcing strategy: secure long‑term contracts for strategic volumes of natural grades where brand positioning requires it, while using synthetic backstops (or blended approaches) to protect continuity and margin during agricultural shocks.

The market is a mix of large, vertically integrated chemical houses and regional specialists focused on natural grades. Our competitive assessment emphasizes capability, specification breadth, geographic reach, and strategic intent rather than simple market shares. Representative profiles included in the full study:

Market concentration is moderate: a handful of global players anchor synthetic supply while numerous regional producers supply natural grades and specialty niches. This creates both stability (from global plants) and episodic pricing pressure (from crop‑linked suppliers), which we quantify and scenario‑test in the full report.

Our scenario work organizes risks into three buckets and provides quantified P&L and working‑capital impacts for each: supply‑shock scenarios from peppermint crop failures; regulatory scenarios particularly around tobacco product rules and pharmaceutical approval pathways; and sustainability/regulatory reporting regimes that increase compliance costs for exporters.

The full PW Consulting L‑Menthol Market study is designed for immediate operational use by procurement teams, product managers, and corporate development groups. Deliverables include:

Note: granular regional and application splits, detailed price series, and target company financials are intentionally omitted from this preview to preserve the transactional value of the complete deliverable.

Our full report provides the data, models, and playbooks needed to operationalize the above recommendations. We combine granular supplier diligence, validated market forecasts, and executable contract language to convert insight into 90‑ to 180‑day actions. For teams making capital allocation or M&A decisions in 2026, this study is structured to be both a pre‑deal diligence package and a strategic roadmap for first‑100‑day integration.

If your board or commercial leadership is sizing investments, negotiating multi‑year offtake, or evaluating acquisition targets in L‑menthol for 2026, the PW Consulting L‑Menthol Market study will supply the transaction‑grade inputs you need. The full dataset contains the withheld regional and application breakdowns, price series, and supplier financial proxies necessary to finalize term sheets and integration plans.

Contact PW Consulting to request the full report and model package; our advisory team can also provide a tailored briefing that maps the intelligence directly to your 2026 planning calendar.

For detailed analysis of this topic, please visit the official page:L-Menthol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com