Railway Sleepers Market 2026: Strategic Preview for Executive Decision‑Making

Why this study matters for 2026 planning

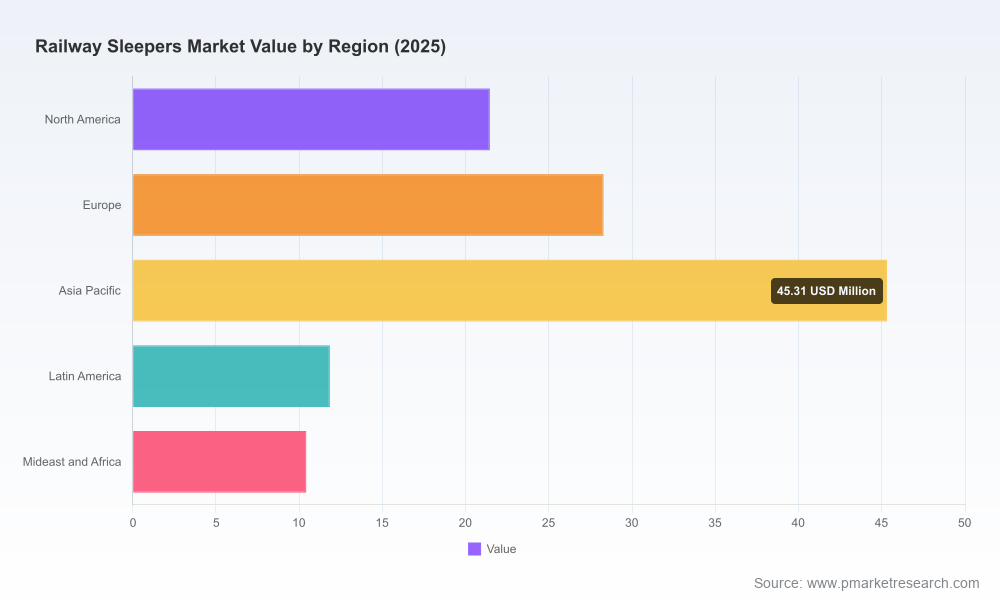

Railway sleepers are a deceptively simple element of rail infrastructure — yet their selection, sourcing and lifecycle management drive a disproportionate share of track cost, resilience and decarbonization outcomes. Our 2026 Railway Sleepers Market study (base year 2025; historical series 2020–2025; forecast 2026–2032) quantifies market trajectories and provides a pragmatic playbook for procurement, capital planning and technology roadmaps. Measured in USD million, the total market was USD 117.3 million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 6.1% through the forecast horizon, reaching USD 179.06 million by 2032. Market concentration metrics (CR3 ≈ 45.5%; CR5 ≈ 50.0%) indicate a market that is established but still contestable — a dynamic context for corporate strategy in 2026.

Railway Sleepers Market

What senior leaders will gain from this preview

- Confidence in capital allocation: a clear, scenario‑based view of demand growth and how it maps to replacement cycles versus network expansion.

- Procurement leverage: insights into where long‑term contracts, local capacity expansion, or strategic inventory positioning materially reduce TCO and schedule risk.

- Decarbonization pathways: quantified impacts of low‑carbon cement and material substitution options on lifecycle emissions and procurement premiums.

- M&A and partnership intelligence: an evidence‑based guide to where scale, technology or geographic footprint delivers defensible advantage.

High-level market dynamics driving 2026 choices

Three converging forces will shape near‑term choices for operators, manufacturers and investors.

Railway Sleepers Market

- Demand fundamentals: The market shows steady mid‑single‑digit growth driven by a mix of capacity projects, heavy‑haul upgrades and maintenance cycles. That balance shifts by geography and track type, which we model in depth in the full report.

- Raw material and input risk: Timber, cement and steel prices remain elevated and volatile as supply chain disruptions persist. These shifts compress margins for traditional sleepers and accelerate interest in low‑maintenance alternatives.

- Regulation and low‑carbon tech: Standards such as EN 13230 and the emergence of CO2‑capture cement materially change procurement specifications. Recent industrial deployments of carbon‑reduced concrete demonstrate that low‑carbon sleepers are moving from pilot to procurement reality.

What the full report contains (practical, actionable outputs)

This study is built as a toolkit for executives, not an academic monograph. Elements you will find inside include:

Railway Sleepers Market

- Executive scenarios: three demand pathways (base, accelerated modernization, and constrained investment) with downstream impacts on procurement and inventory needs.

- Market sizing and dynamic forecast model: an interactive, auditable model with unit assumptions (sleeper density, replacement rates, asset life) and sensitivity levers that let you stress‑test CAPEX plans.

- Competitive and capability maps: supplier scorecards (production footprint, material mix, manufacturing automation, certification, carbon credentials) that translate to sourcing decisions.

- Supplier risk register and mitigation playbook: raw material exposure, single‑source dependencies, logistics chokepoints and recommended contract structures (indexation, LTA triggers, make‑or‑buy thresholds).

- Lifecycle cost models: total cost of ownership templates comparing wood, concrete, steel and composite options across service life, maintenance frequency and carbon pricing scenarios.

- Procurement tools and tender templates: technical specification clauses aligned with EN standards, emissions requirements, and acceptance tests that protect operators while supporting innovation uptake.

- M&A and partnership blueprints: value creation levers for vertical integration, capacity add‑ons, and joint ventures to secure strategic supply in high‑growth corridors.

- Regulatory and standards mapping: implications of timber treatment rules, creosote bans, and concrete conformity standards — with recommended compliance timelines and cost impact estimates.

Competitive landscape — who matters and why (strategic implications)

The market comprises global specialists, regional leaders and niche innovators. The full report contains comparative assessments; below are concise strategic reads on key players you should track:

- Vossloh AG (Düsseldorf, Germany) — A large producer of concrete and composite sleepers that has moved aggressively on decarbonization. Recent supply contracts that incorporate carbon‑reduced cement and strategic acquisitions underpin a technology‑led growth posture. Strategic implication: strong partner for operators prioritizing low‑carbon procurement and scale delivery.

- Abetong AB (Sweden) — A specialist in prestressed concrete sleepers integrated with fastening systems, well positioned for high‑speed and heavy‑haul projects. Strategic implication: attractive acquisition or joint‑venture target for regional contractors aiming to win performance‑sensitive projects.

- L.B. Foster Company (Pittsburgh, USA) — A multi‑material supplier with a broad product set and market access across North America. Strategic implication: a go‑to for integrated supply packages and local content strategies in the Americas.

- voestalpine Railway Systems GmbH (Austria) — Focuses on durability and maintenance reduction through concrete solutions. Strategic implication: vendor of choice for long‑term maintenance cost reduction programs.

- Pandrol Limited (London, UK) — Known for fastening systems and under‑sleeper pads; positions sleepers within a broader systems approach. Strategic implication: potential bundling partner where whole‑track performance matters.

- Stella‑Jones Inc. (Montreal, Canada) — A dominant wooden‑sleeper producer with deep North American market coverage. Strategic implication: faces regulatory and treatment‑cost pressures that may compress margins — consider hedged contracts and substitution pilots.

- IntegriCo Composites (USA) — A niche but rapidly maturing composite supplier offering long‑life, low‑maintenance sleepers. Strategic implication: priority for piloting in maintenance‑sensitive corridors and for operators seeking lifecycle certainty.

- Hyperion Verwaltung GmbH (Germany) — Specialist in Y‑shaped steel sleepers for specific gauges. Strategic implication: retains niche technical value on constrained or special‑geometry lines.

- AGICO (China) — Volume supplier across multiple materials with export capability. Strategic implication: supplier for cost‑sensitive and volume programs, where total landed cost and lead time tradeoffs are key.

Recent developments to watch in 2026

- Major supply contracts and corporate consolidation are accelerating the commercial adoption of carbon‑reduced concrete solutions — a structural shift for lifecycle emissions and procurement specs.

- Manufacturers continue to emphasize automation (extrusion, steam curing, ISO‑certified processes) which reduces labor intensity and enables more competitive manufacturing in higher‑cost regions.

- Regulatory pressure on timber treatment and creosote, paired with evolving standards, is increasing the effective cost and compliance overhead for wooden‑sleeper supply chains.

Decision playbook for 2026 — immediate actions for executives

- Recalibrate procurement specifications to include lifecycle emissions and maintenance cost drivers; demand carbon performance certificates for concrete sleepers where possible.

- Pilot composites and advanced materials on targeted replacement projects to validate TCO benefits under real operational profiles.

- Lock selective long‑term contracts for raw‑material intensive components (cement, treated timber), with indexation and performance KPIs to share risk with suppliers.

- Stress‑test network investment plans against the three demand scenarios in our model; defer or accelerate capital projects based on quantified service‑level tradeoffs.

- Consider small, strategic M&A or capacity partnerships in regions where your supply risk or time‑to‑market is highest — the market concentration metrics show room for scale plays.

- Invest in standards engagement (EN 13230 and equivalents) to shape procurement clauses and ensure early access to validated low‑carbon technologies.

Where this preview leaves you — and how to unlock the models

This briefing demonstrates the strategic value of an evidence‑based approach to sleepers procurement and infrastructure planning in 2026. The material above is intentionally a high‑level extraction: the complete study contains the granular scenario models, per‑track type demand matrices, supplier scorecards, and contract templates required to operationalize these recommendations. If your 2026 capital and procurement cycle is upcoming, the full dataset and interactive tools will materially shorten decision timelines and reduce execution risk.

For access to the full report, dataset exports, and a tailored briefing workshop for your procurement and engineering teams, please consult the PW Consulting Railway Sleepers Market page. Our team stands ready to run a live session that maps your asset portfolio to the demand scenarios and supplier options we model.

For detailed analysis of this topic, please visit the official page:Railway Sleepers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com