Nausea and Vomiting Treatment Market: Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive primer on the Nausea and Vomiting Treatment market that frames the tactical choices business leaders will face in 2026. This document is designed as a high-value “trailer”: it surfaces the macro trends, regulatory inflection points, and competitive dynamics that should shape boardroom strategy, while preserving detailed subsegment forecasts and granular splits for readers who obtain the full report.

Nausea and Vomiting Treatment Market

Market at a Glance — The Big Picture

Using 2025 as the base year, our market model shows a durable recovery and expansion trajectory for antiemetic therapies and adjunct technologies. The global market reached approximately USD 7.13 billion in 2025 and — under our central-case assumptions — is projected to expand at a compound annual growth rate (CAGR) of roughly 6.5% through the 2026–2032 forecast window, reaching just over USD 11.0 billion by 2032. Concentration metrics indicate a moderately fragmented competitive landscape (CR3 ~26.5%; CR5 ~32.1%), leaving substantial room for both incumbent expansion and challenger disruption.

Nausea and Vomiting Treatment Market

Why 2026 Is a Strategic Inflection Point

- New product and technology vectors are converging. The market is no longer exclusively pharmaceutical; device-based symptom management (e.g., neuromodulation wristbands) and combination formulations are reshaping care pathways and payer conversations.

- Policy and reimbursement are tightening the playbook. Recent HCPCS and quality-measure updates mean that commercial and public payers are changing coverage and performance expectations for prophylaxis and rescue therapies.

- Supply-chain and trade policy risk is rising. Tariff actions and raw-material constraints are elevating cost volatility, affecting both generics and proprietary supply chains.

Primary Growth Drivers and Market Dynamics

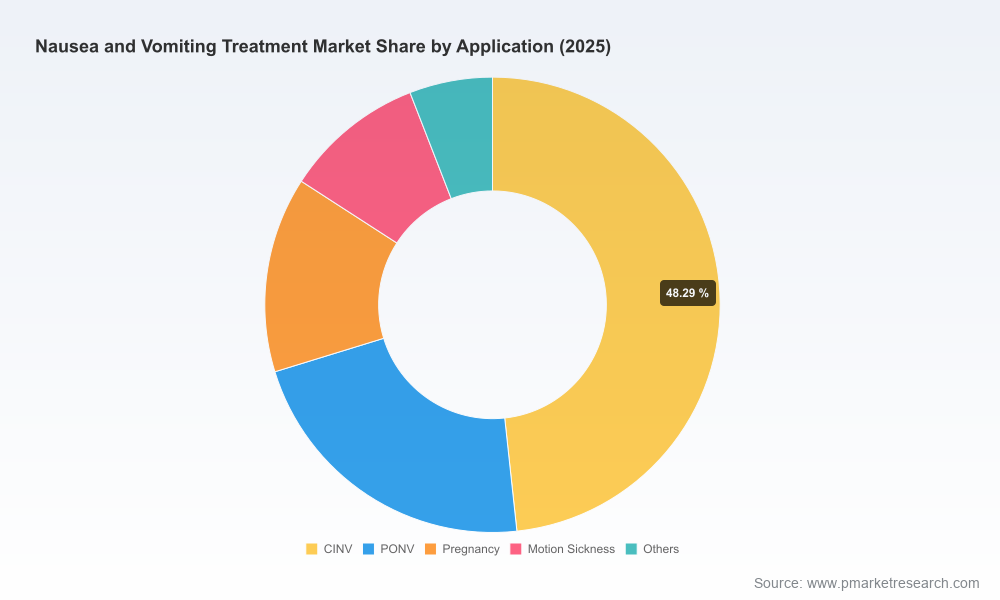

- Clinical demand diversification: Traditional oncology- and perioperative-focused use cases remain the largest demand pools, but motion sickness, pregnancy-related nausea, and consumer wellness channels are growing as medically validated alternatives expand.

- Product innovation: New molecular entities, novel routes of administration, and class-combination strategies (pharmacologic and non-pharmacologic) are increasing the range of care options and enabling premium pricing where efficacy and convenience are demonstrable.

- Payer-readiness and quality incentives: Regulatory measures such as the 2025 MIPS Clinical Quality Measure for PONV require combination prophylaxis in higher-risk patients, which alters inpatient formulary choices and perioperative protocols.

- Device therapy acceptance: Reimbursement clarity — for example, the HCPCS re-classification introduced in October 2025 for certain nerve-stimulation devices — has materially improved the commercial outlook for neuromodulation products.

- Cost pressures and trade policy: Section 232 tariff actions announced for July 2026 add a new dimension of risk for manufacturers dependent on imported APIs and specialized packaging, increasing incentives for local supply diversification.

Competitive Landscape — Who Matters and Why

The market is shaped by a mixture of large pharma incumbents and focused specialists. Key players that dominated our primary research and scenario analyses include, among others, Merck, Helsinn, Pfizer, GSK, Novartis, Sanofi, Johnson & Johnson, Baxter, and a cohort of smaller innovators such as TerSera, Heron Therapeutics, Acacia Pharma, Reliefband Technologies, and EmeTerm. Each brings distinct strategic assets:

Nausea and Vomiting Treatment Market

- Major pharma (Merck, Pfizer, GSK, Sanofi, Novartis, J&J, Baxter): Extensive clinical trial experience, global commercialization networks, and strong hospital and oncology formularies. These players are best positioned to defend large-volume institutional channels and to bundle antiemetic solutions within broader oncology and perioperative portfolios.

- Specialty pharma and device innovators (Helsinn, TerSera, Heron, Acacia): Focused product portfolios and differentiated formulations (e.g., transdermal patches, long-acting NK1 antagonists, rescue agents) that can win on niche efficacy and protocol convenience.

- Device and digital-health entrants (Reliefband, EmeTerm): Non-pharmacologic offerings that are gaining traction in ambulatory, pregnancy, and motion-sickness contexts — a fast-moving category as payer codes and clinical acceptance improve.

Recent regulatory and product milestones underscore the competitive shift. Notably, the FDA approval of a novel motion-induced vomiting therapy in late 2025 represents the first new entrant in decades for that indication and signals faster regulatory pathways for differentiated mechanisms. Separately, device manufacturers continue to extend product durability and service models, increasing lifetime customer value.

Regulation, Reimbursement, and Supply-Chain Considerations

- Reimbursement updates: The HCPCS code E0765 redefinition (effective Oct 1, 2025) and explicit Medicare coverage pathways for oral antiemetics tied to chemotherapy create clear levers for manufacturers to monetize device and oral products within institutional and outpatient settings.

- Quality measures: The 2025 MIPS measure requiring combination prophylaxis for high-risk patients increases demand for multi-class regimens but also raises protocol complexity and opportunities for bundled solutions.

- Input costs & tariffs: Manufacturers should model tariff-driven cost shocks and build mitigation playbooks — from onshoring critical APIs to reconfiguring packaging and sterile manufacturing footprints.

- Regulatory design: Device-specific manufacturing requirements (e.g., sterilization compatibility for reusable neuromodulation wristbands) impose both product development constraints and recurring quality costs that need to be priced into go-to-market plans.

What Our Full Report Delivers — Practical, Transactional, and Tactical

The full PW Consulting study is constructed to be immediately actionable for corporate development, commercial strategy, and operational planning. Deliverables include:

- Proprietary total-addressable-market model (2020–2032) with scenario-ready forecasting engines and sensitivity levers.

- Go-to-market playbooks for five commercial archetypes — incumbent branded, specialty challenger, device innovator, generics consolidator, and channel/consumer entrants — highlighting salesforce design, formulary access tactics, and payer negotiation roadmaps.

- Regulatory and reimbursement impact matrix mapping HCPCS, Medicare coverage rules, and quality measures to expected uptake curves.

- Supply-chain stress tests that quantify exposure to tariff and API-disruption scenarios, with recommended mitigation steps and cost-to-implement estimates.

- Deal and M&A heatmap: prioritized acquisition targets and partnership structures that accelerate access to devices, novel mechanisms, and distribution channels.

- Competitor dossiers and capability benchmarking for the key players referenced above, including launch readiness assessments and vulnerability analyses.

- Primary research appendices: transcripts and anonymized insights from payers, KOLs, hospital formulary committees, and device procurement specialists.

To honor the “trailer” principle, this summary deliberately omits the granular subsegment splits and region-level percentages that underpin the financial model. Those detailed tables, unit-volume forecasts, and pricing assumptions are available exclusively in the full report.

Strategic Recommendations for 2026 Planning Cycles

- Prioritize hybrid portfolios: Firms that combine pharmacologic efficacy with device-enabled symptom control — or tie-device offerings into service-based reimbursement — will capture higher lifetime patient value.

- Lock-in institutional pathways: Use the changing MIPS and HCPCS landscape to secure perioperative and oncology formulary placements through bundled care protocols and outcomes-based contracting.

- Mitigate supply risk proactively: Start contingency sourcing and qualification programs now for critical APIs and specialized materials to avoid margin erosion from tariff-related input-cost shocks.

- Segment go-to-market by channel: Design discrete commercial models for inpatient oncology, ambulatory surgery centers, pregnancy-care clinics, and consumer channels — each requires different clinical evidence and reimbursement narratives.

- Accelerate evidence generation for non-pharmacologic options: Robust real-world data and head-to-head health-economic studies will be decisive in unlocking payer coverage and clinician adoption for neuromodulation and wearable therapies.

Final Thoughts — How to Use This Insight in 2026

For boards and executive teams establishing priorities for the 2026 fiscal year, the Nausea and Vomiting Treatment market presents a balanced opportunity set: steady underlying growth propelled by clinical need and meaningful upside from product innovation and device adoption. However, that upside will accrue unevenly — it will favor organizations that can simultaneously manage regulatory complexity, secure payer pathways, and shore up supply resilience.

If your organisation is evaluating launches, partnerships, or M&A in this space, the full PW Consulting market study is designed to convert uncertainty into a prioritized action plan. The complete research package contains all subsegment forecasts, regional breakdowns, price and volume assumptions, and tactical templates referenced above.

Next Steps

- Request the full report to access the detailed subsegment models, scenario tables, and competitor scorecards.

- Schedule a tailored strategy workshop with our healthcare team to translate the findings into a 12–18 month execution roadmap.

PW Consulting remains available to support executive briefings, due-diligence processes, and operational planning to capitalize on the market dynamics summarized here.

For detailed analysis of this topic, please visit the official page:Nausea and Vomiting Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com