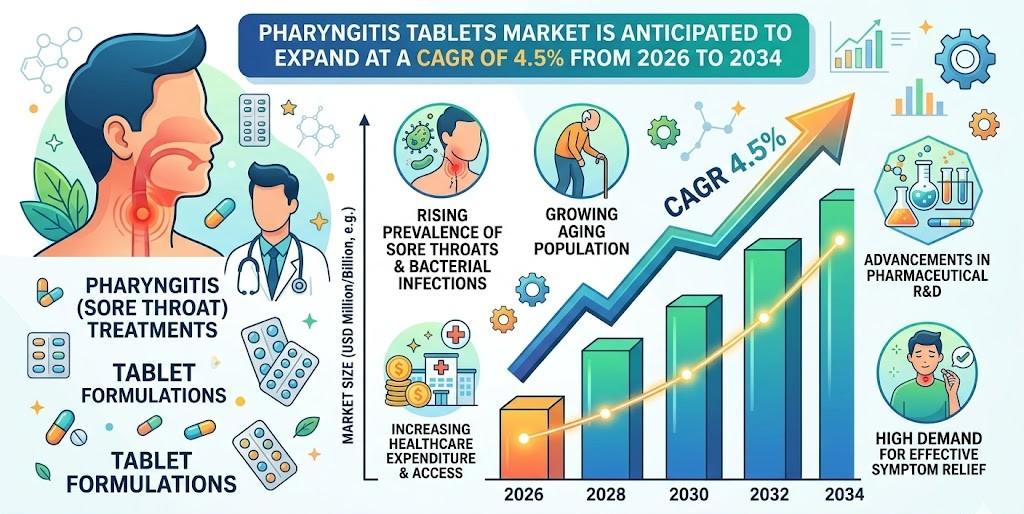

Pharyngitis Tablets Market Growth Analysis 2026–2034

Health |

2026-04-14 14:45:32

As organizations calibrate product roadmaps, channel strategies, and M&A pipelines for 2026, the Water Hammer Arrestors market presents a steady growth profile, structural consolidation, and an increasingly technical specification environment driven by codes and smart-plumbing trends. PW Consulting’s new market study (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes the commercial, regulatory, and engineering signals that will determine winners and losers in the next planning cycle. The market registered a recovery and step-up through 2024–2025, reaching a 2025 market size of USD 283.15 Million, and under our base-case projection is expected to grow at a compound annual growth rate (CAGR) of 4.28% through 2032.

Water Hammer Arrestors Market

Timing: Procurement cycles, code adoption timelines, and spec changes across major construction programs accelerate investment decisions in late 2025 and early 2026. Leadership teams that align R&D, channel incentives, and supplier commitments now will secure specification advantage in 2026–2028 projects.

Water Hammer Arrestors Market

Margin leverage: The category shows durable, differentiated margins for engineered solutions (piston-based, system-rated units) versus commodity designs. Understanding where to position product platforms against regulatory and contractor preferences is central to margin expansion.

Water Hammer Arrestors Market

Consolidation opportunity: The market is moderately concentrated at the top — the three largest suppliers account for a material share of sales and the top five capture a substantial portion of the market — making acquisitive scale and distribution breadth critical competitive levers.

Our historical analysis (2020–2025) captures pandemic-era disruption, subsequent residential retrofit tailwinds, and early adoption of smart plumbing integrations in commercial projects. The market climbed from USD 231.85 Million in 2020 to USD 283.15 Million in 2025. Under baseline assumptions — steady construction activity, continued code enforcement, and gradual penetration of smart plumbing systems — the market grows to an estimated USD 379.76 Million by 2032 at a 4.28% CAGR. This evolution reflects both unit growth in new-build and retrofit demand and a modest shift toward higher-spec engineered arrestors in multifamily and commercial systems.

Product and R&D: Prioritize compact, easy-install forms and smart-enabled arrestors. Recent product launches in 2025 demonstrate vendor emphasis on miniaturization and push-fit/quick-install features. For 2026, differentiate on installation time, PDI/ANSI compliance, and compatibility with smart shut-off and sensor platforms.

Go-to-market and channel: Contractors and plumbing distributors remain the primary adoption vectors. Winning requires trade training programs, SKU rationalization for faster pick-and-pack, and targeted incentives for retrofit-oriented reps. Our field study identifies which trade segments respond to value vs. low-cost propositions — essential input for 2026 channel planning.

Regulatory & standards alignment: Compliance with standards such as ANSI/ASSE 1010 and PDI WH-201 is now table stakes. The International Code Council’s enforcement language and manufacturer-installation obligations mean specification teams must embed compliance documentation into product datasheets and training curricula to reduce rejection at inspection.

Smart plumbing and integration: Partnerships that integrate arrestors into broader water management solutions accelerate value capture. Our research shows initial commercial pilot programs and at least one 2025 vendor collaboration bringing integrated solutions to market — a pattern that will shape specification language in 2026 projects.

M&A and portfolio optimization: Given the market concentration dynamics, acquisitive moves focused on niche engineered technologies, distribution footprint expansion, or complementary water control devices offer the fastest route to scale. Our target-screening framework identifies acquisition profiles that deliver immediate route-to-market benefits versus longer-term R&D plays.

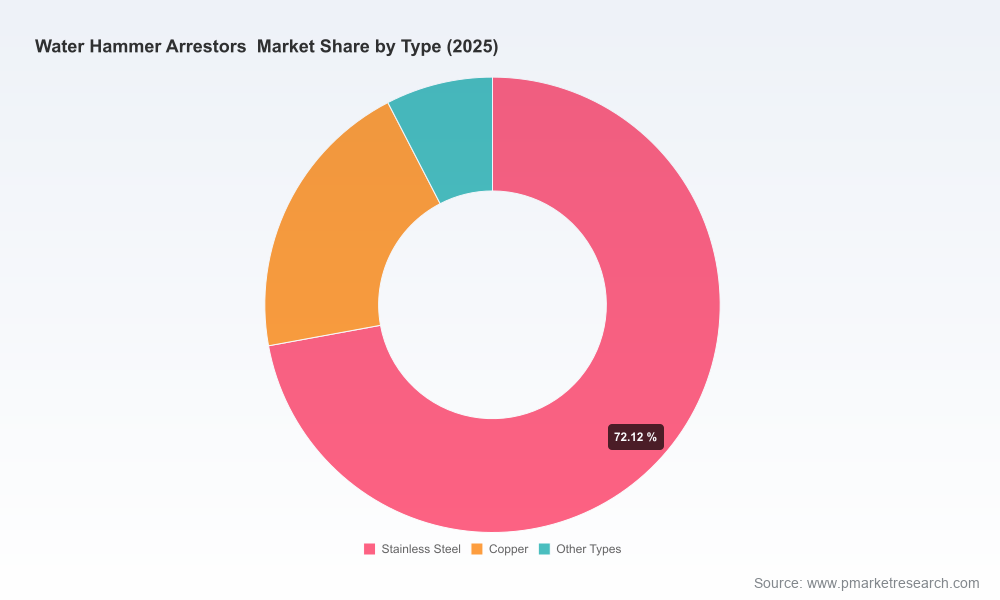

Supply chain and cost resilience: Raw-material volatility (notably for stainless steel and copper) and the need for near-zero lead content in many markets require dual-source strategies and inventory hedging. The report quantifies supplier concentration risk and suggests inventory thresholds for 2026 budget planning.

PW Consulting’s study is written for operators and strategists who need executable outputs, not theory. The full deliverable includes:

Validated market sizing and a 2026–2032 forecast with scenario alternatives (base, upside, downside) and sensitivity to construction cycles and smart-plumbing adoption.

Win/loss analysis and specification maps to show how product features translate into procurement decisions at contractor, distributor, and engineer levels.

Competitive benchmarking (cost curve, product-feature matrix, channel reach) and a playbook for SKU rationalization and margin improvement.

Regulatory compliance matrix aligning PDI, ANSI/ASSE, and national plumbing codes to product development checkpoints and certification timelines.

M&A screen and 12–18 month integration checklists for targets that deliver distribution, engineered capabilities, or complementary product lines.

Implementation-ready GTM templates for retrofit programs, new-build specifications, and multi-family building rollouts — including training outlines and sample distributor incentive plans.

The category features several globally recognized incumbents with differentiated capabilities across residential, commercial, and engineered municipal segments. Our competitive review emphasizes product architecture, distribution footprint, and recent innovation moves:

Watts (North Andover, MA, USA) — Focused on lead-free residential and commercial arrestors. Recent 2025 product activity shows an emphasis on compact units designed for constrained installation environments.

Sioux Chief Manufacturing (Sioux Falls, SD, USA) — Known for USA-made, lead-free mini-series arrestors with a strong presence in trade channels; a reliable play for contractors seeking domestic-sourced solutions.

Zurn (Erie, PA, USA) — Positioned toward engineered commercial and municipal applications with advanced piston technologies; product roadmaps favor specification-grade performance features.

Oatey (Cincinnati, OH, USA) — Distributor-friendly line with an increased focus on integrated solutions; 2025 collaboration activity signals a move toward smart plumbing ecosystems.

Jay R. Smith Manufacturing Co. (Montgomery, AL, USA) — Specializes in piston-type and Hydrotrol designs for a range of sizes and service conditions, often selected for larger commercial projects.

Precision Plumbing Products (Oregon, USA) — Offers system-rated arrestors and PDI-compliant products; appeal to specifiers concerned with standards and reliability.

BERMAD (Israel) — Provides designs focused on pressure-surge absorption at scale, commonly used in multi-story and complex water-supply systems.

Notably, the market saw targeted product innovation in early 2025: compact mini arrestors engineered for tight spaces, push-fit/quick-install mini-arrestors, and integrated smart-plumbing arrestor solutions. These moves illustrate how incumbents are attacking both the retrofit and specification-driven new-build segments.

Regulatory clarity is improving, not loosening. Key reference points for 2026 planning include accreditation under PDI WH-201, performance requirements in ANSI/ASSE 1010, and the National Plumbing Code’s treatment of factory-built arrestors. In practice, this means procurement teams must not only insist on lab certifications but also ensure manufacturer-supplied installation instructions are embedded into project submittals to pass inspections without delay.

To preserve the commercial integrity of actionable intelligence and to encourage direct engagement, this preview intentionally omits granular regional, type, and application-level percent shares and line-by-line revenue tables. The full report contains the detailed segmentation, regional forecasts, and price curves that clients use to build business cases and model investment returns. If your 2026 plan requires line-item visibility by region, application, or material type, the full dataset—presented with interactive charts and downloadable spreadsheets—is included in the premium package.

Conduct SKU triage: Prioritize compact, low-install-time SKUs for retrofit programs and engineered piston units for commercial specifications.

Lock-in distribution pilots: Agree 12-month incentive trials with high-velocity distributors in target metro markets to accelerate specification wins.

Certify early: Fast-track PDI/ANSI certifications for next-generation arrestors and embed compliance evidence into pre-bid packets.

Screen acquisition targets: Evaluate small engineered-product manufacturers or regional distributors that deliver immediate route-to-market synergies.

Test smart integrations: Run two commercial pilots integrating arrestors with building water-management controls to validate value capture and retrofit simplicity.

The Water Hammer Arrestors market offers predictable growth and attractive margins for firms that blend product engineering, compliance rigor, and channel execution. While unit growth is steady, the real upside in 2026 will accrue to firms that leverage certification-led product development, shorten installation time through form-factor innovation, and secure specification pathways into commercial and multi-family projects. PW Consulting’s full study provides the granular inputs you will need to convert these strategic directions into executable 12–36 month plans.

Access the complete PW Consulting report to obtain the full regional and application segmentation, downloadable datasets, and the competitor scorecards referenced in this brief. For tailored advisory support — including scenario modelling for acquisition candidates, distributor incentive design, or pilot specifications for smart-plumbing integrations — contact our strategic advisory team.

For detailed analysis of this topic, please visit the official page:Water Hammer Arrestors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com