Temperature Monitoring Devices Market: Strategic Imperatives for 2026

Executive Preview

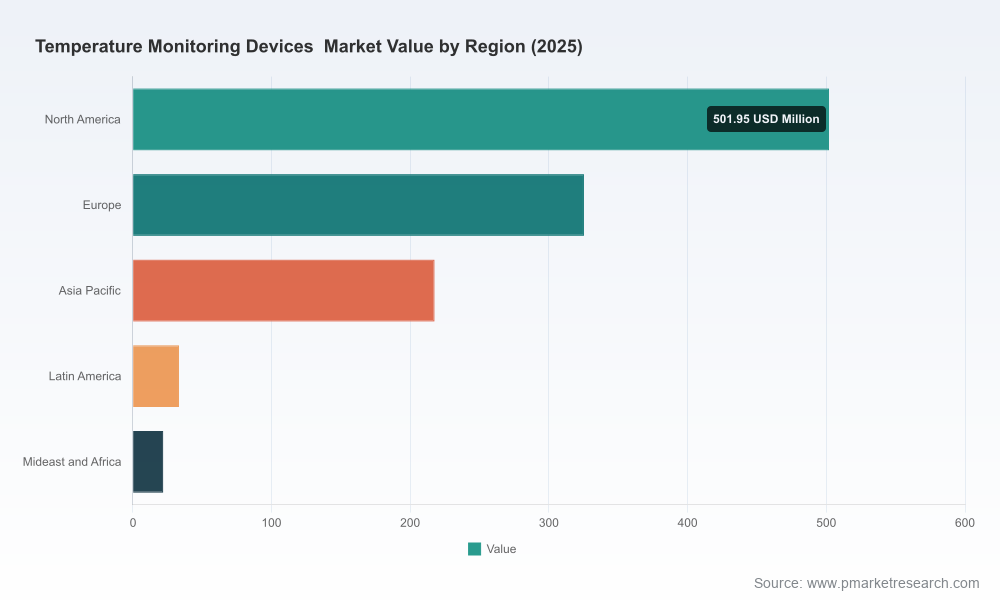

As healthcare providers, device manufacturers, and supply-chain stakeholders finalize budgets and strategic plans for 2026, temperature monitoring devices are at an inflection point. PW Consulting’s latest market study—anchored to a 2025 base year and projecting through 2032—finds the global market growing at a compound annual growth rate (CAGR) of 5.9%. After steady expansion from the early 2020s, the market reached approximately USD 1.10 billion in 2025 and is modeled to continue expanding into the early 2030s, reflecting a mix of clinical adoption, regulatory nudges, and digital-enabled use-cases across care settings.

Temperature Monitoring Devices Market

Why This Study Matters for 2026 Decision-Making

Leaders must convert macro momentum into executable programs—whether allocating R&D budgets, selecting M&A targets, or redesigning procurement contracts. The strategic value of this study is pragmatic: it translates market trajectory into decision-ready guidance for 2026. We show where growth pockets are emerging, quantify the sensitivity of revenue to reimbursement and material-cost shocks, and map regulatory risk against product roadmaps. To preserve commercial advantage for subscribers, this preview intentionally omits granular segment-level revenue tables—those precise splits are available in the full report and the accompanying downloadable datasets.

Temperature Monitoring Devices Market

Key Market Dynamics Driving 2026 Priorities

- Clinical and Guideline Pressure: Updated clinical guidance is reshaping procurement behavior. Professional bodies are urging pre‑purchase evaluations of measurement and warming devices, which elevates the value of validated performance data and third‑party clinical evidence in 2026 purchasing decisions.

- Regulatory Tightening and Quality Expectations: The new Quality Management System Regulation (QMSR), effective February 2026, aligns device manufacturers with ISO 13485:2016 expectations. Manufacturers must accelerate quality-system remediation and documentation to avoid market access delays.

- Reimbursement Shifts: Inclusion of external temperature-monitoring procedures within contemporary coding and reimbursement guidance creates new monetization levers—and new administrative burdens—for providers and vendors. Understanding payer-specific coding workflows will be a critical supplier capability this year.

- Materials and Cost Pressure: Supply-side inflation for advanced insulation materials and specialty polymers—material cost inflation observed since 2021—continues to compress margins. Procurement strategies, design-for-cost, and supply diversification will differentiate winners.

- Device Convergence and Connectivity: The market’s technological trajectory favors continuous, wireless, analytics-enabled monitoring (e.g., disposable Bluetooth patches, wearable forehead sensors, and robust cold-chain loggers). Value is increasingly realized not from single‑use sensors alone but from linked data streams and integration with EMR and logistics platforms.

- Regulatory Classifications Expanding Clinical Scope: New regulatory classifications for niche applications—such as brain temperature measurement—signal longer-term device sophistication and potential carveouts for specialty products.

Recent Market Movements That Matter

- April 2026: Paragonix Technologies launched a next‑generation thermal control solution for cardiac transport—underscoring continued innovation in high-value transport use cases and the premium placed on tight temperature stability across critical shipments.

- November 2025: Arctx Medical received FDA 510(k) clearance for a catheter system for body temperature regulation—highlighting cross‑discipline device strategies where temperature control becomes an interventional therapy rather than a monitoring adjunct.

Competitive Landscape — Strategic Takeaways

The market structure remains fragmented: the top-three and top-five incumbent shares indicate ample room for regional specialists, niche innovators, and new entrants to scale. Below we summarize strategic postures of four influential participants to illustrate competitive archetypes and implications for 2026 strategy.

Temperature Monitoring Devices Market

- 3M Company (St. Paul, MN) — A large diversified medtech with a perioperative focus, 3M’s offering underscores an enterprise play: single‑use core sensors integrated into warming systems. Strategic implication: expect 3M to continue leveraging clinical relationships and large-system procurement channels; potential partners should offer complementary evidence proving incremental clinical or operational value.

- Blue Spark Technologies (Westlake, OH) — With a wearable disposable Bluetooth patch for continuous axillary monitoring, Blue Spark exemplifies the “connected disposable” model. Strategic implication: connectivity and data workflows are differentiators. Vendors without an interoperable cloud/EMR story will struggle to compete in ambulatory and home-care adoption paths.

- Sensitech (Nashua, NH) — Focused on cold‑chain and clinical trial logistics with Bluetooth-enabled data loggers, Sensitech highlights logistics-centric value capture. Strategic implication: partnerships with CROs, biomanufacturers, and pharma logistics providers are high‑value plays for device firms moving beyond clinical monitoring into supply-chain assurance.

- Drägerwerk AG & Co. KGaA (Lübeck, Germany) — With continuous core trackers using adhesive sensors, Dräger represents the high-reliability bedside monitoring faction. Strategic implication: legacy bedside-systems incumbents will compete on integration, accuracy, and clinical adoption; nimble challengers can win share by combining lower unit cost with cloud analytics and streamlined procurement terms.

What the Full PW Consulting Report Delivers (Operational Outputs)

The full study is structured to convert analysis into action. Key deliverables include:

- Market model (historical 2020–2025, forecast 2026–2032) with base-case, optimistic, and downside scenarios calibrated to reimbursement and materials‑cost variables.

- Segmentation logic and TAM/SAM/SOM frameworks mapped to clinical use cases and delivery settings (note: granular numeric splits are reserved for subscribers).

- Competitive heat maps and capability matrices across technology, clinical evidence, pricing, and digital integration.

- Supplier and raw‑material risk dashboards with hedging options and design‑for‑cost levers.

- Regulatory and reimbursement playbooks—timelines, evidentiary requirements, and payer-approval strategies specific to 2026 rules and coding changes.

- Go‑to‑market templates (value propositions by buyer persona, pilot designs, and contract negotiation checklists).

- M&A target scoring model and a shortlist of acquisition archetypes that would accelerate share capture.

- Excel toolkits for pricing-sensitivity, PBM/reimbursement impact analysis, and production-capacity planning.

How to Use These Insights to Shape 2026 Initiatives

Below are prioritized, actionable steps for executives planning resource allocation and product strategy in 2026:

- Prioritize Regulatory and Reimbursement Readiness: Immediately align quality systems with QMSR/ISO 13485 expectations and map product labeling to new coding guidance. Early alignment reduces time-to-market and positions products for preferential procurement.

- Invest in Data Integration: For both clinical-monitoring and cold-chain modalities, the marginal value now lies in analytics and workflow integration. Allocate resources to secure APIs, cloud-certification, and EMR partnerships.

- Hedge Material Cost Exposure: Rework BOMs for cost resilience and qualify alternate suppliers. Consider passing through material surcharges via contracting clauses for large institutional buyers.

- Design Trials With Reimbursement Endpoints: Clinical validation should include economic outcomes and coding capture—this creates a stronger negotiating position with payers and large health systems.

- Pursue Modular Partnerships: If your core capability is sensors, partner with cloud and logistics specialists to expand into value-added services without long hardware cycles.

- Screen M&A Targets by Capability, Not Geography: Look for targets with complementary digital capabilities, clearance footprints, or unique logistic relationships rather than simply regional revenue.

Closing — Where PW Consulting Adds Immediate Value

For 2026, temperature monitoring devices represent both an operational necessity and a platform for new, recurring revenue models tied to data and services. PW Consulting’s study translates macro growth (CAGR 5.9% and a market expanding from approximately USD 1.10 billion in 2025) into market-entry, product, and operational playbooks. We have intentionally provided a high-level preview here; the full report and accompanying datasets contain the detailed segmentation, regional, and application-level figures that procurement, product, and M&A teams will require to finalize budgets and contracts this year.

To access the complete intelligence suite—including the granular segment tables, supplier heat maps, and Excel tools—visit the report page or contact PW Consulting for a subscriber briefing. Our analysts are prepared to run tailored scenario workshops that apply the study’s models to your portfolio and market targets for 2026.

For detailed analysis of this topic, please visit the official page:Temperature Monitoring Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com