Insulated Jacket Market — 2026 Strategic Preview

As PW Consulting’s senior strategy advisor and chief industry analyst, I present a forward-looking executive preview of the Insulated Jacket Market intended to guide 2026 corporate decision-making. Anchored on a 2025 base year, the market sizing and trend analysis in this preview are drawn from a full study that combines historical patterns (2020–2025) with scenario-based forecasts through 2032. At the aggregate level the market has expanded steadily from the early 2020s and is projected to grow at a compound annual growth rate of approximately 5.8% over the forecast window — a trajectory that creates distinct strategic inflection points for product managers, supply-chain leaders, and corporate development teams.

Insulated Jacket Market

Why this briefing matters for 2026 decisions

- Timing: 2026 is the first full planning year after several industry shocks — tariff changes, accelerating material substitution, and fast-moving product innovation — that together alter cost structures and consumer expectations.

- Scale and shape: The overall market size has moved materially since 2020 and the near-term 2026 baseline reflects both pent-up demand and structural shifts in channel and product mix. This is not a marginal cyclical correction; it is a structural re-pricing of premium versus mass-market propositions and the economics of insulation technologies.

- Decision leverage: Tactical choices made in 2026 — supplier contracts, R&D prioritization, pricing architecture, and channel investment — will compound through the forecast period and determine whether firms capture disproportionate share as the market expands.

Macro forces shaping 2026 strategy

- Cost pressure from trade and input dynamics: Recent tariff adjustments have raised the average duty environment and, in aggregate, increased manufacturing input costs for exposed apparel segments. Independent analyses point to a mid-single-digit impact on input cost lines for industries that rely on imported textiles and components; this requires rebuilding margin models and re-evaluating lead-time vs. landed-cost trade-offs.

- Material transformation and sustainability premium: Leading brands are accelerating adoption of recycled and low-carbon synthetic fillings. High-profile product launches using 100% recycled PET fibers have moved the sustainability conversation from niche to mainstream, forcing competitive responses across price tiers.

- Product innovation frontiers: Integrations of connectivity and sensing, and the commercialization of advanced insulation technologies (including nanotech-enhanced fills), are shifting feature parity and creating new axes of differentiation beyond traditional loft and fill-power metrics.

- Demand texture: Consumer spending in apparel has shown modest recovery signals, but buyers are increasingly discerning about durability, repairability, and embodied environmental impact. This favors brands that can credibly align technical performance with circular-economy credentials.

Competitive structure — fragmentation and strategic ramifications

The insured-jacket landscape remains structurally fragmented. Market concentration metrics indicate that the top three and top five suppliers do not dominate in the way seen in many consumer industries; there is substantial room for regional specialists, technical premium players, and large-format mass-market brands to co-exist. For incumbents and newcomers alike, this fragmentation implies both opportunity and risk: the ability to scale a distinct proposition quickly can capture premium pockets, but failing to differentiate leaves brands exposed to margin compression.

Insulated Jacket Market

Key competitors and strategic postures we monitor closely:

Insulated Jacket Market

- Canada Goose — Maintains a premium, performance-led winter portfolio targeted at extreme cold use-cases. Their brand equity supports high price points and selective distribution.

- The North Face — Continues to blend technical performance with mainstream accessibility; recent moves into smart, sensor-enabled jackets signal a commitment to feature-based differentiation.

- Patagonia — A category leader in sustainability positioning; product introductions built from recycled PET fibers exemplify how environmental credentials can be operationalized at scale.

- Arc’teryx and Rab — Specialist, high-performance brands that command loyalty among mountaineering and technical users; their relentless focus on fit, materials, and systems integration is a barrier to entry in technical segments.

- Columbia Sportswear — A broad active-lifestyle player that has supplemented organic capabilities with capability-building M&A, including acquisitions focused on novel insulation technologies.

- Helly Hansen, Fjällräven, Mammut — Regional and segment specialists with strong reputations in professional and endurance-use contexts; these brands often lead in niche channel partnerships and B2B professional supply agreements.

- REI Co-op and Uniqlo — Represent different ends of the distribution spectrum: REI with private-label value and sustainability strategies for outdoor shoppers; Uniqlo with mass-market, design-for-scale insulated offerings.

Recent corporate developments illustrate strategic directions: Patagonia’s 2025 rollout of fully recycled synthetic jackets shifted competitive expectations on materials; Columbia’s acquisition of a nanotech insulation startup in 2025 signals accelerated tech-driven differentiation; and The North Face’s launch of a connected insulated jacket in mid‑2025 demonstrates the emergence of digital-enabled garment value propositions.

What the full report delivers — practical outputs for teams

The complete PW Consulting study is intentionally operational. It is structured to convert market insight into executable choices across five workstreams:

- Strategic sizing & scenario planning: A granular forecast framework that allows users to test alternate growth trajectories by channel, price tier, and product-innovation adoption curves. (Note: the executive preview intentionally withholds granular split tables; these are available in the full report.)

- Supply-chain stress testing: Landed-cost models, tariff-sensitivity analyses, and supplier concentration mapping to prioritize near-term sourcing and negotiation strategies.

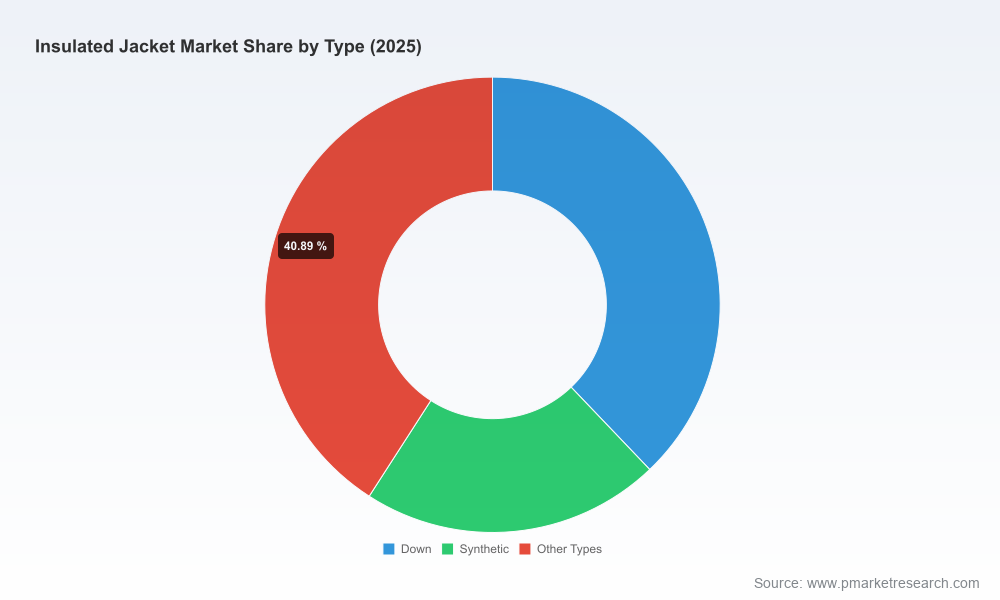

- Product and R&D playbooks: Comparative performance assessment of insulation technologies (down, synthetic, emerging nanotech), feature-value mapping, and cost-to-benefit models to inform product roadmaps and SKU rationalization.

- Go-to-market and channel optimizers: Retail vs. DTC return-on-investment scenarios, co‑branding and licensing constructs, and inventory‑carry strategies tuned for seasonality and demand volatility.

- M&A and partnership screening: A transaction readiness checklist, valuation overlays for target archetypes, and integration risk matrices designed for both bolt-on acquisitions and minority strategic investments.

Actionable implications for 2026 playbooks

- Reprice with rigor: Given the changed duty landscape and raw-material transitions, firms should re-run product-level P&Ls and implement dynamic pricing tests that protect margin without eroding volume elasticity.

- Invest selectively in materials and IP: Firms that commit to validated low-carbon synthetics or proprietary insulation tech can translate those investments into sustainable premiums and differentiated go-to-market stories.

- Diversify sourcing and nearshore where it matters: Shorter, more resilient supply chains reduce tariff and lead-time exposure; for many players, a hybrid model (strategic nearshore capacity plus cost-efficient offshore scale) is optimal.

- Prioritize product modularity: Designing interchangeable insulation layers and repairable shells can extend product lifecycles and lower customer acquisition costs through stronger loyalty.

- Prepare for digital feature competition: Connected garments will create new service layers (data-driven comfort control, extended warranties, subscription-based updates). Early pilots can surface monetization pathways and avoid late-stage scramble.

- Use concentration gaps as acquisition runway: A fragmented top table means well-executed M&A can buy substantial scale and distribution quickly; build an acquisition pipeline now with clear post-merger integration playbooks.

How to use this preview — next steps

This preview is designed as a decision trigger. PW Consulting’s full Insulated Jacket Market study contains the detailed segmentations, channel and regional tables, supplier scorecards, and downloadable models that decision teams will need to operationalize the strategies summarized above. For 2026 planning cycles, we recommend three immediate actions:

- Commission a 90-day supply-chain stress test that overlays your vendor list against the tariff and raw-material scenarios we modelled.

- Run a two-track product strategy: protect near-term margin via pricing/assortment adjustments while funding a medium-term pivot to sustainable and tech-enabled insulation offerings.

- Initiate a prioritized M&A watchlist focused on insulation tech, near‑shore manufacturing, and adjacent channel access, with pre-drafted LOI and integration templates.

To access the full dataset, proprietary segment models, and executable playbooks — including the tables and maps that have been intentionally omitted from this preview — please refer to the PW Consulting Insulated Jacket Market report landing page. The complete study is structured to convert the 5.8% CAGR and the evolving market dynamics into board-level actions, product roadmaps, and transaction-ready diligence materials that will determine winners and laggards across the coming planning cycles.

For detailed analysis of this topic, please visit the official page:Insulated Jacket Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com