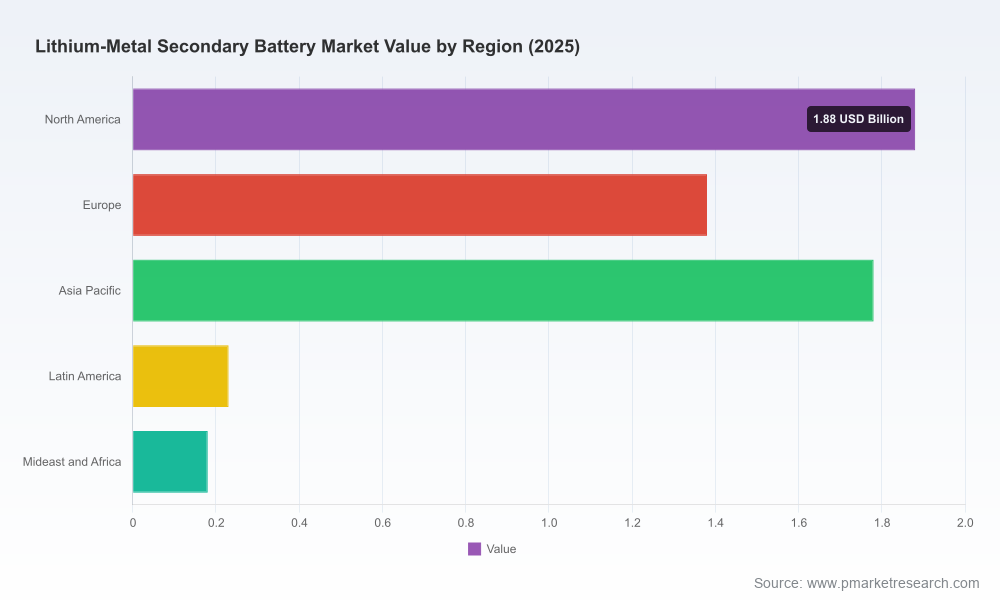

Lithium‑Metal Secondary Battery Market — A Strategic Primer for 2026 Decision‑Making

Between incremental engineering breakthroughs and a volatile raw‑materials backdrop, lithium‑metal secondary batteries have transitioned from laboratory promise to a nascent commercial ecosystem. This primer synthesizes the market trajectory, competitive posture, and actionable decision frameworks that corporate leaders and investors need to evaluate before committing capital or revising product roadmaps in 2026. It is derived from PW Consulting’s full Lithium‑Metal Secondary Battery Market study (base year 2025) and is structured to demonstrate analytical depth while reserving the report’s granular sub‑segment economics and proprietary datasets for license holders.

Lithium-Metal Secondary Battery Market

Market trajectory and what it means for corporate strategy

The market has moved rapidly over the past half‑decade and is now on a steep growth path. From a modest base in 2020, market revenues accelerated through 2025 and—under PW Consulting’s central forecast—continue to expand strongly across the 2026–2032 horizon. Our modeling shows the market entering a scale phase in the mid‑2020s; revenues grow at a compound annual rate of 18.42% across the forecast window, reaching a multi‑billion‑dollar market by 2032.

Lithium-Metal Secondary Battery Market

- Implication for product and R&D roadmaps: High CAGR and clear commercial momentum justify stepping up near‑term development budgets for higher‑energy‑density architectures (e.g., lithium‑metal anodes, lithium‑sulfur and solid‑state prototypes) while tightly managing technical‑risk gates.

- Implication for capital allocation: Early entrants that secure downstream cell manufacturing or stable anode supply can capture outsized margin expansion as manufacturing scales and material learning curves reduce cost per kWh.

- Timing sensitivity: The development curve is non‑linear—first‑mover premium applies for demonstration contracts and defense/aerospace sales, but mainstream adoption (EVs, grid services) depends on 2027–2030 cost parity dynamics that we model in the full study.

What the PW Consulting report contains (practical, transaction‑ready capabilities)

Our objective is pragmatic: equip decision makers with tools they can use this year. The report includes:

Lithium-Metal Secondary Battery Market

- Market sizing and scenario modeling (base year 2025; historical 2020–2025; forecast 2026–2032) with downside, central, and upside demand paths calibrated to technology readiness and macro inputs.

- Unit‑economics and cost‑curve models by manufacturing archetype (pilot cell, gigafactory, localized anode production), including sensitivity analysis to variable feedstock costs and manufacturing yield improvements.

- Supply‑chain mapping and stress‑testing: bottleneck identification for metal supply, precursor chemicals, and process equipment; lead‑time scenarios and mitigation playbooks.

- Technology readiness and integration assessment: TRL benchmarking across lithium‑metal anodes, lithium‑sulfur, and solid‑state chemistries; implications for thermal management, safety certification, and packaging standards.

- Commercial go‑to‑market playbooks: partner vs. captive manufacturing decision matrices, licensing templates, and sample JV term sheets calibrated to technology exclusivity windows.

- M&A and investment universe: diligence checklists, valuation drivers for strategic and financial bidders, and a ranked watch‑list of target archetypes (IP owners, pilot producers, specialty material suppliers).

- Regulatory and ESG matrix: mapping of certification timelines, recycling and end‑of‑life pathways, and jurisdictional permitting considerations relevant to 2026 commercial rollout plans.

- Proprietary datasets and dashboards (interactive): monthly raw‑material stress indices, manufacturing CAPEX benchmarks, and commercialization readiness timelines by company cohort.

Competitive landscape — who matters now

The market exhibits meaningful concentration: the top three firms account for just over half of identifiable commercial capacity metrics we track, and the top five approach roughly two‑thirds of that concentrated metric. That structure creates strategic dynamics where leading IP owners and early producers can materially influence standards, supplier terms, and customer expectations.

- Lyten (San Jose, CA) — An important vertical player that has moved from demonstration to domestic production of battery‑grade lithium‑metal foils and alloys. Lyten’s 2025 U.S. production startup signals industrialization of foil supply for lithium‑sulfur anodes and is a critical step towards shortening lead times and stabilizing specialized input supply chains.

- Sion Power (Tucson, AZ) — Focused on high‑energy secondary lithium‑metal cells for defense, aerospace and other high‑value applications. Sion’s program expansion and targeted initial shipments in late 2026 position it as a prime candidate for early contractual deployments in sectors where performance justifies premium pricing.

- Pure Lithium Corporation (Chicago, IL) — Pursuing vertical integration from lithium feedstock to anode and cell production with proprietary “Brine to Battery™” innovations. Recent patent allowances in multiple jurisdictions strengthen its strategic options for localized production in regions seeking secure and traceable lithium supply chains.

- SES AI (Woburn, MA) — Specializes in lithium‑metal polymer electrolyte cells, including large‑format 50Ah and 100Ah designs aimed at EVs, drones and urban air mobility. SES AI’s pilot‑to‑production scaling illustrates the different commercialization paths between specialty high‑value cells and mass‑market automotive formats.

- Regional and European entrants — Suppliers such as Avesta have announced series production of lithium‑metal anodes in 2025, expanding the diversity of supply and technical options available to OEMs seeking non‑US, non‑Asian suppliers.

For executives this creates clear strategic choices: lock exclusive supply and IP options with a narrow set of first movers, or maintain optionality and diversify across regional suppliers to mitigate single‑source risk. The best choice depends on the firm’s appetite for time‑to‑market versus unit‑cost optimization over a five‑year horizon—our report provides decision trees and contract templates for both approaches.

Dynamics and risk: raw materials, prices and regulation

Raw‑material volatility has been a key driver of near‑term economic uncertainty. Lithium chemical spot prices showed wide swings across 2024–2026, compressing margins for some producers and creating opportunities for vertically integrated supply chains. These price swings—combined with differential availability of battery‑grade hydroxide and carbonate feedstocks—affect both capex recovery timelines and unit cost per kWh.

Regulatory landscapes are equally important. Permitting for new lithium‑metal production, material handling rules, and certification pathways for novel cell architectures (especially those with metallic lithium anodes) vary by jurisdiction and will shape where large‑scale capacity is economical to build. Our regulatory risk matrix highlights jurisdictions with faster certification cycles and those with emerging strategic incentives that materially alter levelized cost outcomes.

Actionable recommendations for 2026 decisions

- Prioritize supply‑chain options that reduce exposure to spot feedstock volatility. For organizations without upstream control, short‑term offtake plus hedging strategies should be coupled with strategic options for equity stakes in anode or foil producers.

- Differentiate by application: pursue early high‑margin niches (defense/aerospace, premium drones, urban air mobility) to establish reference customers and de‑risk production flows before scaling into price‑sensitive EV and grid markets.

- Adopt a phased CAPEX approach: stagger investments tied to demonstrable yield improvements and safety certifications. Our capex model shows the inflection points where larger factory builds become accretive under central and upside scenarios.

- Use IP and partnership levers: locking non‑exclusive technical partnerships can accelerate market access without the full cost of captive manufacturing; exclusive licensing should be reserved for core, defensible process IP that aligns with long‑term strategic positioning.

- Integrate regulatory readiness into the product development timeline: allocate resources early for certification testing and recycling pathway design to avoid commercialization delays common in 2026 deployments.

The strategic value of the full PW Consulting study

This primer outlines the strategic levers available to executives in 2026, but the full report contains the transaction‑grade detail required to act: scenario‑specific financial models, vendor scorecards, contract archetypes, and our interactive dashboards. Critically, the report retains and protects proprietary sub‑segment economics—market share curves, regional and application splits, unit costs by cell architecture and supplier—because those are the constructs that materially change deal valuations and require controlled dissemination.

If you are planning to allocate R&D funding, make capacity commitments, negotiate offtake arrangements, or evaluate strategic investments in lithium‑metal technologies in 2026, PW Consulting’s full dataset and advisory services will convert the macro view presented here into executable actions and defensible board materials.

Next steps

Contact PW Consulting’s Lithium‑Metal practice to request the full study, interactive models, or a tailored executive briefing. We offer accelerated option‑scans and diligence‑on‑demand services for clients who require a compressed decision cycle during 2026 budget and strategy rounds.

For detailed analysis of this topic, please visit the official page:Lithium-Metal Secondary Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com