Stored Product Pest Control Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Senior Strategic Advisor and Lead Industry Analyst, I present a distilled, decision-focused introduction to our comprehensive Stored Product Pest Control Market study. This briefing is designed to clarify the macro forces, competitive dynamics, and near-term strategic choices that will matter most to executives planning budgets, acquisitions, and product-roadmap shifts in 2026. The full report contains the granular segmentations, proprietary models, and playbooks that operational teams will need to execute. Consider this a high-fidelity preview: enough depth to guide executive judgment, intentionally withholding the granular tables and segment-by-segment figures to direct you to the full subscription product for implementation-level intelligence.

Stored Product Pest Control Market

Market trajectory: what the numbers mean for 2026 planning

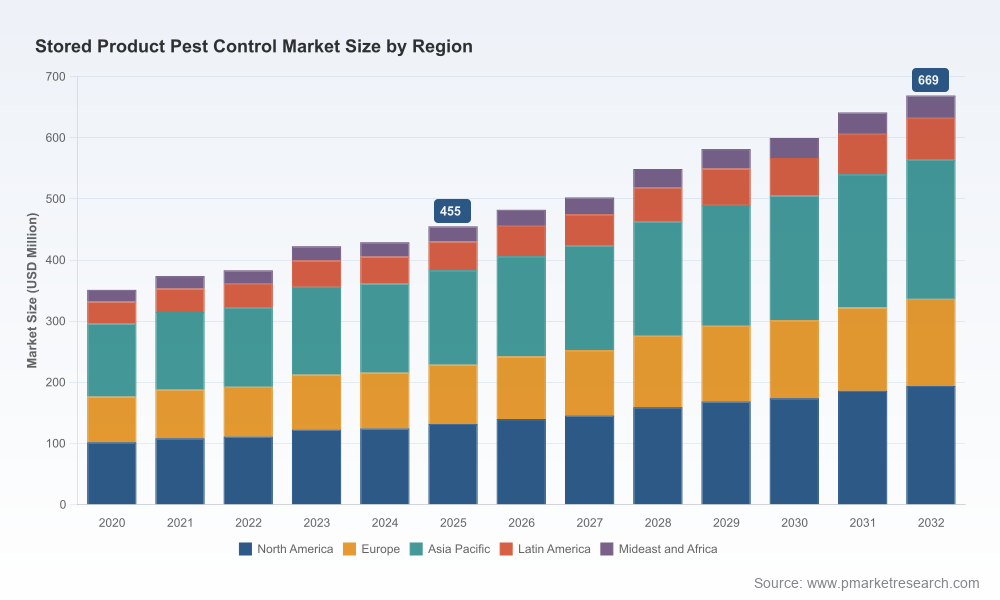

The stored product pest control market is on a steady growth path. From a base that expanded from roughly USD 350–380 million in the early 2020s, the industry reached approximately USD 455 million in our 2025 base year. PW Consulting’s forecast projects continued expansion through the 2026–2032 planning window at a compound annual growth rate (CAGR) of 5.9%, with total market value approaching the high hundreds of millions by the end of the forecast horizon.

Stored Product Pest Control Market

For strategy teams, those headline numbers translate into three practical expectations for 2026:

Stored Product Pest Control Market

- Demand headroom exists for expansion—organic growth will account for a meaningful slice of opportunity, but achieving above-market growth will require targeted investments in capability or M&A.

- Regulatory and operational risk will increasingly determine which players capture premium margins; compliance capability is now a commercial lever, not just a cost center.

- Technology and service differentiation (monitoring, IPM, integrated contracts) are where margins and sticky customer relationships concentrate—commodity chemical plays alone will be under margin pressure unless paired with value-added services or proprietary delivery systems.

Macro dynamics shaping the market

Three categories of external forces will shape competitive outcomes in 2026: regulation & compliance, raw-material and logistics constraints, and shifting buyer economics driven by food-safety & traceability demands.

- Regulatory tightening and credentialing: Recent regulatory milestones (including the U.S. EPA’s completed registration review for phosphine and metal phosphides, updated labeling and permit regimes in states such as California, and the universal classification of phosphide products as Restricted Use Pesticides) elevate compliance complexity. Companies that can operationalize certification, training, and audit-ready application protocols will turn regulatory burden into a barrier to entry.

- Raw-material & logistics realities: Phosphine remains the primary fumigant for many stored-commodity applications, but it depends on specialized transportation containers, micro-dosing units, and certified applicators. Supply-chain resilience—spare parts for dosing equipment, cylinder availability, and trained applicators—will be as strategic as chemical supply agreements.

- Customer-side pressure: Food processors, grain handlers, and warehouses are increasing investment in monitoring, traceability, and non-chemical controls (biologicals, IPM) to satisfy buyers and regulators. This lifts demand for integrated service models and technology-enabled pest management solutions.

Competitive landscape: leaders, challengers and the structural picture

The market is moderately concentrated: our concentration analysis shows the top three firms control a meaningful majority of market share, and the top five approach near-dominant levels. That concentration profile creates clear implications: scale matters for distribution, regulatory engagement, and R&D, while regional specialists and service-focused players can still capture attractive niches by investing in technical service and customer intimacy.

Key corporate archetypes in 2026:

- Global chemical integrators: Established crop protection and chemical majors (examples include legacy players headquartered in Europe, North America, Japan, and India) combine product portfolios with global distribution. Their strengths: regulatory influence, broad R&D budgets, and access to agronomic channels. Their limitations: slower to adapt on-the-ground service models and less nimble in region-specific operational compliance.

- Specialist fumigant and equipment manufacturers: Firms focused on fumigation technologies (including cylinderized phosphine and micro-dosing solutions) are technical anchors for the market. Their IP and training programs make them indispensable partners for large grain-handling customers and professional applicator networks.

- Service-first providers: Professional pest management companies and food-safety contractors leverage recurring revenues, integrated monitoring, and outcomes-based contracts to sustain margins. They often partner with chemical suppliers rather than compete head-on on product.

- Regional manufacturers and OEMs: Local producers—particularly in key commodity-producing regions—compete on price and fast supply, and they can be acquisition targets for multinational firms seeking local access or cost arbitrage.

Notable company developments and signals worth watching:

- A recent product and capability rollout by a leading fumigant specialist introduced a cylinderized phosphine product into a major market alongside a certification course for applicators. This combination—product launch plus operator training—illustrates a deliberate move to control both supply and the competency layer that locks customers into the supplier’s ecosystem.

- Major agrochemical and chemical firms continue to maintain portfolios oriented to stored-product applications, but many are shifting commercialization emphasis toward integrated solutions (fumigant + monitoring + service) rather than stand-alone chemistry.

- Service providers are increasingly aggregating through M&A or partnerships to scale technical teams and technology platforms, creating attractive acquisition targets for chemical majors seeking downstream distribution and recurring revenue.

Report content — practical, actionable deliverables included

Our full study is structured to convert insight into action. Highlights of the deliverables included for executive and commercial teams are:

- Market sizing and forecast models (historical 2020–2025 base, forecast 2026–2032) with sensitivity scenarios tied to regulatory outcomes and technology adoption curves.

- Regulatory risk matrix and compliance playbook mapping regional registration, restricted use classifications, and permitting permutations to commercial impact (time-to-market, training costs, label constraints).

- Supplier & channel mapping that profiles incumbents, regional specialists, OEMs, and service providers—aligned with go-to-market implications for manufacturers and third-party service contractors.

- Commercial playbooks for four corporate archetypes (global chemical houses, fumigation specialists, service providers, and regional players) with specific investment priorities and KPIs for 2026 execution.

- M&A and partnership screens, including asset-level due diligence checklists and integration templates tailored to pest-control product lines and service platforms.

- Operational templates: application-certification program blueprints, digital monitoring ROI calculators, and container/dosing logistics risk mitigations.

- Case studies and negotiation playbooks based on recent market moves and procurement behaviors of food processors and grain handlers.

Strategic implications and recommended 2026 moves

For leaders preparing budgets and strategy in 2026, we recommend a small set of high-impact actions:

- Harden regulatory & certification capability: Invest in certified applicator programs, label-compliant packaging, and audit-ready documentation. For chemical suppliers, co-develop training with fumigation equipment partners to lock in distribution channels and reduce liability.

- Diversify delivery models: Combine chemical offerings with monitoring, IPM advisory services, and biological alternatives. Pilots that demonstrate reduced total-cost-of-ownership for customers will accelerate adoption and create recurring revenue streams.

- Secure critical logistics and spare parts: Establish strategic inventory positions for dosing equipment and specialized cylinders, or contract with local manufacturers to mitigate cross-border transport risk.

- Take an opportunistic M&A stance: Target acquisitions that provide local applicator networks, digital monitoring platforms, or manufacturing access in high-growth commodity corridors. With the top five players controlling a substantial share, bolt-on acquisitions remain the quickest path to near-term scale.

- Run scenario planning tied to regulatory inflection points: Model outcomes under stricter residue tolerances, additional state-level permit regimes, and potential restrictions on key chemistries. Embed trigger-based contingency budgets to accelerate pivots.

How to use this preview — next steps to operationalize

This executive preview is designed to set direction. The full PW Consulting Stored Product Pest Control Market report contains the granular segment-level shares, regional and application breakouts, company scorecards, and downloadable financial models you will need to execute. If your team is evaluating capex, M&A, pricing strategy, or compliance investments for 2026, request the full dataset and the scenario-driven slides for board-level presentation. Our clients use these deliverables to build 18-month operating plans and to stress-test post-merger integration cases.

In summary: the market offers predictable expansion, but the path to outperformance in 2026 runs through regulatory mastery, service differentiation, and selective consolidation. Firms that ignore certification and logistics realities risk commoditization; those that combine chemistry, training, and digital monitoring will secure the most defensible positions.

For access to the full report, the underlying models, and tailored advisory engagements, contact PW Consulting’s Commercial Intelligence team to schedule a briefing. The full intelligence package contains the segment-level granularity and proprietary frameworks you’ll need to translate this strategic preview into operational advantage.

For detailed analysis of this topic, please visit the official page:Stored Product Pest Control Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com