Medical Device Tray Market: Insights and Competitive Analysis

Other |

2026-02-18 09:10:00

As capital allocation cycles reset and construction pipelines mature in 2026, executives in roofing materials, building products, and downstream contracting need a concise but analytically rigorous view of the roofing underlying materials market to make defensible decisions. This preview from PW Consulting synthesizes core, market‑level trends from our full Roofing Underlying Materials Market report (base year 2025) and outlines the precise strategic uses of the research for 2026 planning — while intentionally preserving the granular segmentation tables and confidential model outputs for subscribers and licensees.

Roofing Underlying Materials Market

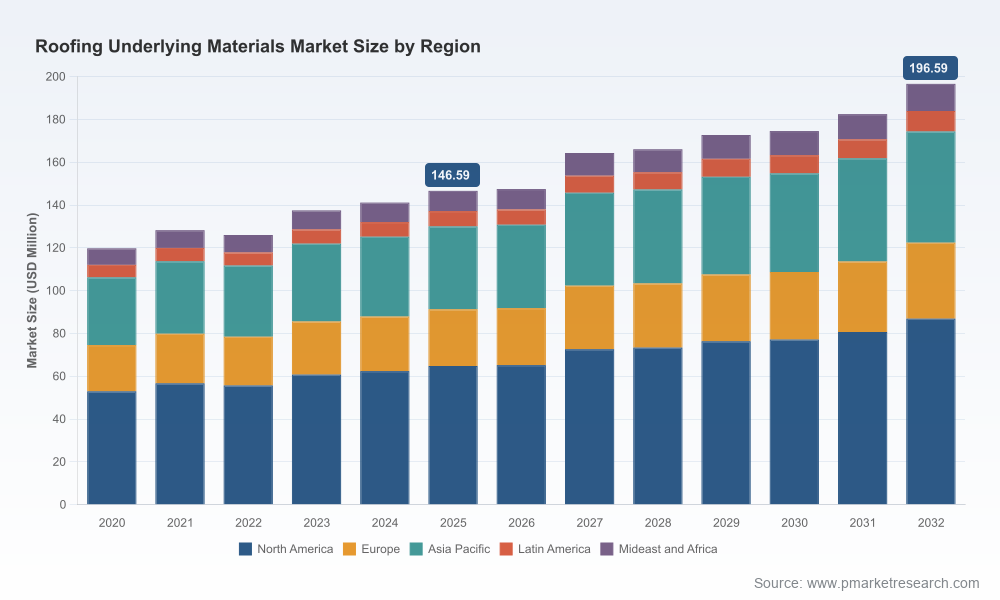

Between 2020 and 2025 the global roofing underlying materials market expanded materially, reflecting both cyclical recovery and structural demand from residential renovations and commercial retrofits. Our modeled market trajectory shows that the market grew from a low‑teens base in 2020 to a mid‑three‑figure total (USD Million) by 2025, and the forecast through 2032 carries a compound annual growth rate of 4.2% under the base scenario. That mix of steady expansion and near‑term volatility — driven by commodity cost swings and construction price inflation — makes 2026 a pivot year for strategy.

Roofing Underlying Materials Market

Commodity pressure: Brent and WTI crude traded in a band around the low‑to‑mid‑$90s per barrel in early June 2026, a level that materially raises asphalt and resin feedstock costs. These dynamics have transmitted directly into supplier cost structures and pricing.

Roofing Underlying Materials Market

Input inflation: Construction input prices displayed clear upward momentum in early 2026: month‑over‑month input inflation and a notable year‑over‑year rise in the first quarter put immediate pressure on margin profiles for underlayments and base materials.

Supplier response: Major manufacturers implemented price increases in March–April 2026. Several leading residential and commercial suppliers announced mid‑single to high‑single digit price adjustments across shingles, membranes, and underlayments in response to rising raw material costs.

Market structure: The roofing underlying materials market remains fragmented relative to more consolidated building‑materials subsegments. The top few firms do not dominate volume to the extent seen in other industrial markets, supporting both competition and opportunities for consolidation plays.

Our full report is built for decision use, not just reporting. The package combines the market model, scenario testing, procurement playbooks, and competitive intelligence so teams can convert insight into actions during 2026 budgeting and strategic planning cycles. Key deliverables include:

Dynamic market model (2020–2032): A downloadable, scenario‑enabled model calibrated to observed volumes and prices through 2025 with base, upside, and downside scenarios to stress test revenue, margin, and capacity assumptions.

Price elasticity and pass‑through analysis: Quantifies how input cost moves (notably asphalt and polymer resins) have historically passed through to end prices, enabling procurement and commercial teams to set cadence for price adjustments and contract clauses.

Procurement playbook: Tactical guidance on hedging strategies, supplier scorecards, and inventory positioning tailored to the roofing underlayment supply chain.

Manufacturing footprint and capex workbook: Decision tools to evaluate plant throughput enablers, retrofit tradeoffs, and near‑term brownfield expansion vs. offshoring options under varying input cost pathways.

Commercial and go‑to‑market recommendations: Channel segmentation, route‑to‑market scenarios for synthetic vs. asphalt‑based underlayments, and pricing tactics aligned with contractor procurement cycles.

M&A and partnership screen: Prioritized target themes and valuation sensitivity matrices for buyers seeking scale, technology, or geographic fill‑ins in a fragmented market.

The market features a mix of integrated, vertically oriented incumbents and specialist membrane manufacturers. Leading firms maintain differentiated advantages through distribution breadth, branded warranty programs, and proprietary membrane technologies. Examples of notable participants in the competitive set we track closely include:

GAF Materials Corporation (Parsippany, New Jersey) — a dominant North American residential and commercial roofing systems producer with broad exposure to asphalt shingles and underlayments.

Owens Corning (Toledo, Ohio) — markets synthetic and self‑adhered underlayments alongside the traditional component set for residential and commercial applications.

CertainTeed Corporation (Malvern, Pennsylvania) — known for premium asphalt products and sustainability positioning in residential roofing.

Carlisle Companies (Scottsdale, Arizona) and Johns Manville (Denver, Colorado) — strong players in single‑ply membranes and commercial underlayments, with product portfolios oriented to retrofit and low‑slope applications.

IKO Industries (Mississauga, Ontario), TAMKO Building Products (Galena, Kansas), Atlas Roofing Corporation (Atlanta, Georgia), Duro‑Last, and Soprema — a mix of vertically integrated manufacturers and membrane specialists with sizable regional footprints.

Operationally, several of these firms moved in lockstep on pricing in early 2026: public notices from multiple manufacturers announced price increases across residential and commercial roofing lines in March–April 2026. Those coordinated moves indicate two realities: (1) feedstock pressures are industry‑wide and (2) margin restoration through pricing will be an important lever for incumbents while demand remains resilient.

For management teams, the intersection of persistent input volatility and steady demand growth creates several concrete imperatives for 2026:

Short-term: Revisit pricing cadence and contract language. Given recent upstream cost inflation, firms must accelerate commercial cadence and implement standardized pass‑through clauses while avoiding margin erosion in competitive bids.

Procurement: Increase focus on feedstock diversification and options for synthetic substitutes. Hedging programs and multi‑sourcing can blunt near‑term shocks; in parallel, evaluate higher‑value synthetic underlayments where payback on reduced lifecycle maintenance can be justified.

Operations: Prioritize throughput improvements and selective capex for assets that reduce dependence on volatile input streams, including investments in blending, recycling, and polymer modification capabilities.

Portfolio optimization: Use the market model to identify which product families and geographies deliver the best risk‑adjusted returns under alternate crude scenarios. In a fragmented market, disciplined M&A can accelerate scale and distribution without overstretching balance sheets.

Sustainability and regulation: Factor evolving codes and green procurement preferences into product roadmaps; higher upfront costs for advanced membranes can be offset by lifecycle savings and improved public‑sector procurement positioning.

Our advisory engagement for roofing materials operators typically integrates three workstreams that mirror 2026 priorities:

Commercial acceleration: We help build price playbooks, renegotiate distributor terms, and realign warranty economics so sales teams can implement price adjustments with minimal leakage.

Supply chain resilience: We run procurement stress tests using our commodity scenarios, define hedging thresholds, and redesign supplier scorecards to reduce single‑source exposure.

Strategic transactions: For buyers and investors, we deliver target screening, valuation sensitivity, and integration blueprints that incorporate cost volatility and the fragmented competitive landscape.

In line with the “preview” objective, this article intentionally focuses on the strategic implications and omits the detailed, proprietary segmentation tables that drive execution. The full report includes granular, license‑protected content you will need for transactional and operational execution: detailed regional and application splits, product‑level demand curves, supplier by plant mapping, and a set of downloadable data tables supporting the 2020–2032 model. These deliverables are designed to be plug‑and‑play with your internal planning tools.

Immediate (0–90 days): Run a rapid margin vulnerability assessment using your current cost and contract terms; adjust list pricing where allowable and implement contractual pass‑through language for volatile feedstocks.

Near term (90–180 days): Adopt a commodity scenario plan using our model to stress test manufacturing and procurement strategies; prioritize capex that improves feedstock flexibility.

Medium term (180–365 days): Evaluate M&A and partnership opportunities to close distribution gaps and consolidate where scale advantages are evident; implement product portfolio changes to capture premium segments resistant to low‑cost competition.

Roofing underlying materials sit at the cross‑section of commodity exposure, construction demand, and evolving product technology. For 2026, the highest‑return moves are those that combine disciplined commercial execution with targeted operational investments — informed by a robust market model and competitive intelligence. PW Consulting’s full Roofing Underlying Materials Market report supplies both the data and the playbooks to act.

To obtain the complete dataset, scenario model, and the supplier scorecards that underpin this analysis, please visit our report portal or contact your PW Consulting representative. The full deliverable contains the confidential segmentation, plant‑level mapping, and the downloadable financial model required to translate these strategic recommendations into 2026 P&L and capital plans.

For detailed analysis of this topic, please visit the official page:Roofing Underlying Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com