Strategic Preview: Safety Shut-off Valves for Gas Meters Market — Why PW Consulting’s 2026 Research Will Shape Your Next Move

As PW Consulting’s Chief Industry Analyst, I present a focused, strategy-first preview of our latest market study on safety shut-off valves for gas meters. This is a “trailer” — designed to demonstrate the analytical depth and decision-usefulness of the full report while deliberately withholding granular segmentation data to encourage direct engagement with the source research. What follows synthesizes the largest strategic signals, explains how this intelligence will be used by executives in 2026, and outlines the practical playbook included in the full study.

Safety Shut-off Valves for Gas Meters Market

Headline market signals (what you need to know now)

- Market momentum: With a compound annual growth rate (CAGR) of 9.1% across our forecast horizon, the sector is transitioning from niche safety equipment to a mainstream element of smart gas distribution strategy. Our base-year analysis (2025) and multi-year forecast (2026–2032) demonstrate sustained, investment-grade growth driven by regulatory pressure, smart-meter integration, and rising safety expectations in residential, commercial, and industrial settings.

- Clear adoption inflection: Measured installations of integrated safety meters and retrofit valve solutions— spotlighted by milestone rollouts from leading meter OEMs—are converting awareness into procurement cycles. This translates into growing addressable revenue and a widening set of use-cases for manufacturers, utilities, and systems integrators.

- Market structure: Despite the presence of notable OEMs and safety specialists, concentration metrics point to a fragmented ecosystem with room for consolidation and vertical partnerships. The competitive landscape rewards technology integration, regulatory credibility, and scalable supply chains.

Why this research matters for 2026 decisions

Decisions made in 2026 will determine who leads in product specification, who participates in utility procurement contracts, and who captures the early recurring-revenue streams from safety-enabled meter services. Our report converts raw market growth into specific strategic implications:

Safety Shut-off Valves for Gas Meters Market

- Product strategy — Whether you are an OEM, valve specialist, or systems integrator: the imperative is to embed automatic, remote, and environmental-triggered shut-off capabilities in product roadmaps. Those capabilities are becoming minimum viable features for new meter specifications in several jurisdictions.

- Regulatory positioning — Emerging and existing rules (earthquake- and fire-actuated shut-off approvals, state-level mandates, and demo programs run by energy commissions) create deterministic demand windows. The report maps these regulatory triggers to procurement timelines so you can prioritize market entry and certification efforts.

- M&A and partnership timing — Fragmentation plus accelerating adoption creates both tuck-in acquisition and strategic JV opportunities. The study provides an investment framework to evaluate targets by technology fit, regulatory certifications, installed base access, and channel reach.

- Go-to-market and commercial models — With increasing appetite for meter-level services (remote shut-off, safety alerts, sensor fusion), vendors can shift from single-sale hardware to service-enabled contracts. The report translates adoption curves into price-volume scenarios and go-to-market tactics for 2026.

Competitive dynamics — what incumbents and new entrants are doing

- Itron: The Intelis platform has crossed meaningful installed-base thresholds and highlights how integrated shut-off valves plus remote-control capabilities create product differentiation. The strategic implication is clear: scale in installed units accelerates validation and creates a platform effect for meter-based safety services.

- Honeywell / American Meter / Elster: Ongoing demonstrations and field programs around smart meters with embedded shut-off valves showcase the commercial trajectory from demonstration to specification. Integrations with methane and environmental sensors are emblematic of the next wave—automated, sensor-driven shut-off as part of broader safety systems.

- NSF Control and specialist valve vendors: Regulatory compliance and standards expertise remain decisive for utilities and meter OEMs. Firms with certified valve technologies and proven integration toolkits become preferred partners in regulated procurements.

- Regulatory nudges: Location-specific measures—ranging from earthquake-actuated approvals to fire shut-off mandates—are not academic; they materially affect procurement windows. Where such mandates or pilot programs are active, procurement accelerates and product certification becomes a commercial gatekeeper.

What the full PW Consulting report delivers (practical, executable content)

We designed the report for operators, product leaders, corporate development teams, and utility procurement planners who need to make evidence-backed decisions in 2026. Contents include:

Safety Shut-off Valves for Gas Meters Market

- Market sizing and validated forecasts — base-year and annualized projections across the 2026–2032 horizon, plus sensitivity scenarios tied to regulatory and technology adoption inflection points.

- Methodology transparency — our data sources, triangulation methods, and assumptions so you can model bespoke scenarios for your business.

- Regulatory matrix — an actionable map of standards, mandatory programs, demonstration projects, and certification requirements that directly influence procurement cycles.

- Commercial models and price-volume scenarios — templates to stress-test OEM and integrator go-to-market strategies, including service bundling and recurring revenue pathways.

- Competitive benchmarking and vendor scorecards — qualitative and quantitative assessments of OEMs, valve specialists, and systems integrators along technology, certification, channel, and scale dimensions.

- Deployment playbooks and pilot templates — step-by-step guides for utility pilots, retrofit programs, and specification-driven rollouts, including KPIs and testing criteria.

- M&A and investment framework — a decision rubric to prioritize targets, integrate acquisitions, and estimate value creation over a 3–5 year horizon.

How to use the intelligence: a 6-step 2026 playbook

- Regulatory-proof your roadmap: Prioritize certifications and design-for-compliance features aligned with active and anticipated mandates. Use our regulatory matrix to forecast timelines for approvals and procurement cycles.

- Prioritize integrations, not just components: Meter manufacturers and valve suppliers should formalize OEM partnerships and API standards to reduce time-to-specification for utilities.

- Deploy pilot clusters that de-risk scale: Run geographically distributed pilots tied to regulatory programs to accelerate evidence for procurement. The report includes pilot KPIs and acceptance criteria used by utilities.

- Evaluate supply-chain resilience: Secure dual sourcing for key valve components and validate capacity assumptions against our scenario forecasts to avoid production bottlenecks as adoption ramps.

- Consider vertical plays: Utilities and large service providers should evaluate owning meter-plus-safety-service stacks to capture recurring revenue and data monetization opportunities.

- Use M&A selectively: Target firms that provide either certification shortcuts, installed-base access, or unique sensor-fusion competencies. Our acquisition rubric ranks candidates based on defensibility and integration cost.

What we deliberately withhold here — and why

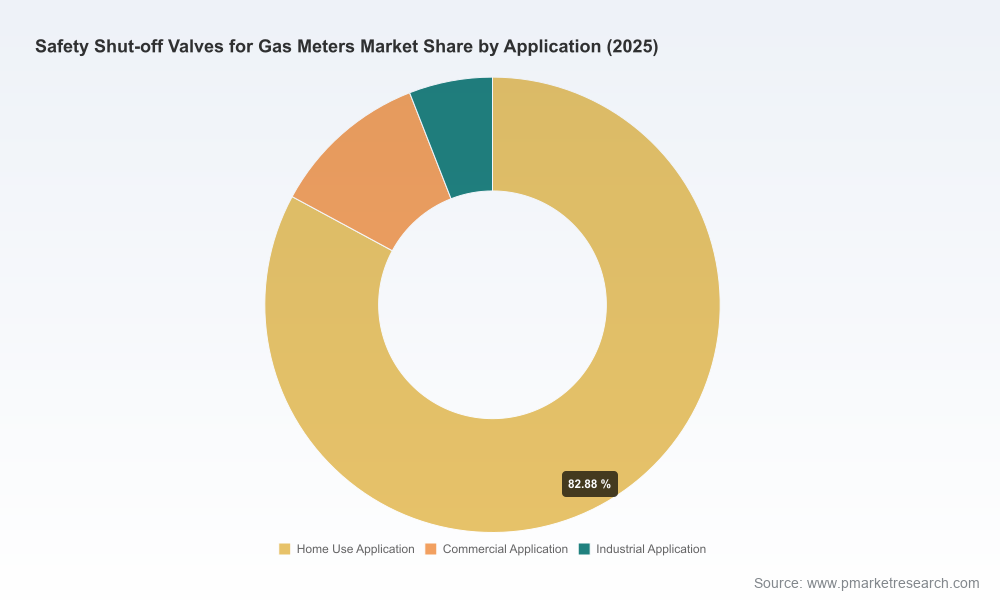

This preview purposely omits granular regional and application split figures, detailed segment-by-segment revenue tables, and the complete vendor scorecard. Those elements are central to tactical procurement and investment decisions and are presented in the full report as proprietary, downloadable deliverables. If you are evaluating a tender response, M&A target, or a 2026 product roadmap, the segmented tables and downloadable models in the full report will be indispensable.

Bottom line: the strategic inflection is now

By 2026, safety shut-off valves are no longer optional for many new meter installations; they are part of the specifications that will determine who wins utility contracts and who is excluded. With a robust CAGR and a clear pathway from pilot demonstrations to regulatory-driven procurements, the window for strategic positioning is narrow but actionable. Early movers — those that combine regulatory credibility, system integration, and supply-chain readiness — will capture the structural advantages that follow.

To access the full intelligence, including the proprietary regional and application splits, price curves, and vendor scorecards that underpin the analyst recommendations above, please consult the complete PW Consulting Safety Shut-off Valves for Gas Meters Market report on our research portal. The report contains the operational tools and datasets your leadership team needs to convert the 2026 opportunity into sustainable market leadership.

For detailed analysis of this topic, please visit the official page:Safety Shut-off Valves for Gas Meters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com