Third-Party Risk Management Market Growth and Future Trends

Other |

2026-04-16 08:40:35

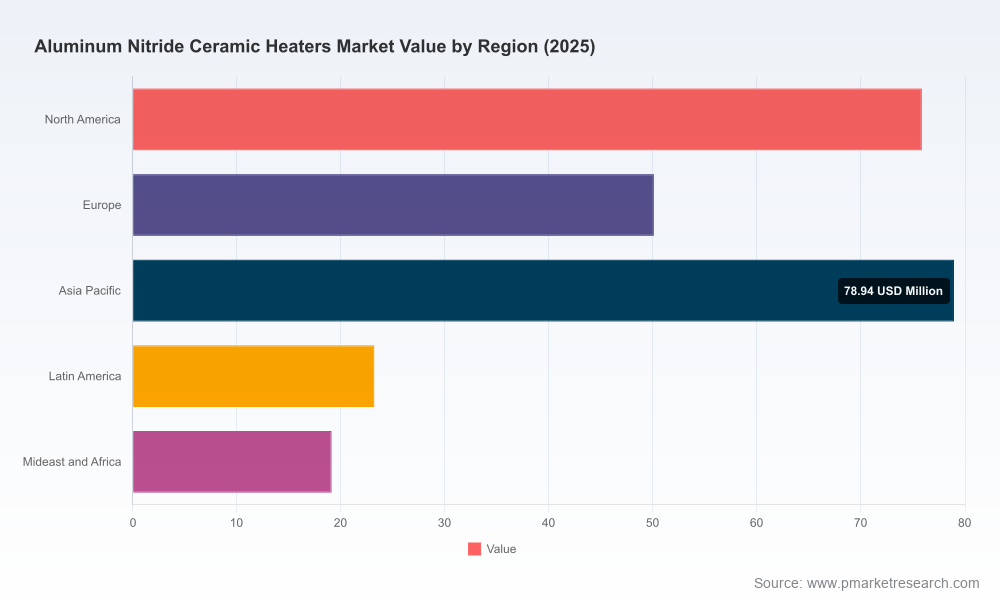

As semiconductor, medical, and advanced industrial applications push thermal management requirements into ever-higher performance envelopes, the Aluminum Nitride (AlN) ceramic heaters market has moved from niche specialty to strategic component class. Our analysis at PW Consulting shows the market expanding from approximately USD 185.5 Million in 2020 to USD 247.2 Million in 2025 (base year), with a projected compound annual growth rate (CAGR) of 7.2% through the 2026–2032 forecast window. By 2032, revenues are expected to approach the USD 402 Million mark.

Aluminum Nitride Ceramic Heaters Market

This briefing outlines why that trajectory matters for 2026 planning cycles: manufacturers, equipment OEMs, materials suppliers and investors need clarity on supply constraints, technology roadmaps, and differentiated go-to-market plays. We deliberately present high-level, decision-useful insight here while preserving the granular segmentation and proprietary scenario outputs for the full report—your next step if you need executable intelligence.

Aluminum Nitride Ceramic Heaters Market

Timing aligns with capital cycles: Many players will finalize product roadmaps, capacity investments, and M&A decisions in 2026. Understanding the pace and shape of AlN heater demand—already growing strongly—changes the NPV and risk calculus for multi-year investments.

Aluminum Nitride Ceramic Heaters Market

Thermal design is a gating factor for advanced nodes and ALD/CVD process control: As deposition and etch recipes tighten thermal uniformity tolerances, heater performance (multi-zone control, embedded sensors, low-impedance layouts) becomes a critical differentiator for equipment OEMs and their supplier selection.

Supply-chain resilience and second-source strategies are now board-level topics. The market is not highly concentrated: incumbent leaders exist, but capacity and capability are distributed across specialized manufacturers—creating both opportunity and procurement risk.

Several structural forces underpin the 7.2% CAGR and the projected USD ~402 Million endpoint in 2032. First, the semiconductor equipment cycle remains the primary growth engine—AlN heaters are mission-critical in CVD, ALD and PECVD toolsets where temperature uniformity, low thermal mass and contamination control are non-negotiable. Second, the growth of adjacent high-reliability sectors (medical devices, high-temperature power electronics, aerospace) broadens end-market diversity, improving overall resilience to cyclical downturns.

On the supply side, improvements in hot-pressing, direct-sintering and multilayer ceramic manufacturing have driven higher yields and more complex multi-zone architectures. Innovations such as embedded RTDs, tungsten trace integration, and thick-film patterning expand functional differentiation, enabling suppliers to command technical premium and drive migration from legacy heater materials.

The competitive set combines legacy ceramic specialists, diversified industrial ceramics players, and focused tier-two innovators. Market concentration measures indicate a moderately fragmented market: leading groups capture meaningful share, yet there is room for technology-led competitors to scale quickly.

NGK Insulators, Ltd. — A recognized leader for high-purity AlN heaters used in CVD/ALD/PECVD. Their strength is in multi-zone, custom modules tailored to semiconductor equipment suppliers. Strategic implication: strong OEM relationships and deep process knowledge make them a preferred first-call supplier for high-spec toolsets.

Sumitomo Electric Industries, Ltd. — Notable for recent capacity expansion (a 31% uplift in 2024 targeting 300mm wafer applications). This move signals aggressive pursuit of the advanced wafer market and raises the bar for delivery capability when large-scale OEM qualification windows open.

CoorsTek, Inc. — Large-scale manufacturer offering hot-pressed and direct-sintered AlN components; claims a significant share of global AlN heater production capacity. Their scale translates to faster lead-times and the ability to support larger program volumes—an advantage in OEM sourcing strategies.

MARUWA, MiCo Ceramics, Fralock, Heatron, Watlow, Kyocera and Xiamen-based innovators — These firms differentiate via high-conductivity substrates, embedded sensors, multilayer architectures, and tailored geometries for cleanroom applications. Several specialize in second-source and niche configurations attractive to equipment integrators seeking redundancy.

Emerging Chinese and US players — A growing cohort of suppliers provides flexible, custom manufacturing and competitive pricing. For buyers, this increases negotiating leverage but also increases the importance of qualification and supply assurance processes.

Given the current fragmentation and the presence of technically capable mid-sized suppliers, procurement strategies should evolve beyond single-supplier cost negotiation. Companies that will win in 2026 adopt a portfolio sourcing approach combining:

Product evolution in AlN heaters is concentrated around three axes: thermal performance (uniformity, ramp rates), integration (embedded RTDs and traces, compatibility with wafer handling), and manufacturability (yield, scalability, supply lead-times). For R&D and product management teams, the practical priorities for 2026 are:

PW Consulting recommends a set of executable options for market participants depending on their starting position—supplier, OEM, or investor. These are actionable and directly linked to the market trajectory we forecast:

The comprehensive study extends the insights summarized here into a practical playbook for 2026. Deliverables include:

Note: This preview intentionally abstracts core split-level data and proprietary scenario outputs. For practitioners who need the granular segmentation, regional demand curves, and model-access to run customized scenarios for 2026 approval cycles, the full report is the operational tool you’ll use.

AlN ceramic heaters are no longer a marginal component; they are a strategic element that affects equipment performance, yields and time-to-market for advanced processes. With the market on a steady growth path (CAGR ~7.2% through 2032) and multiple capable suppliers, 2026 is a decisive year for locking in supply, differentiating product offerings and securing program economics.

To convert these insights into an executable plan, request the full PW Consulting report and the interactive forecast model. The report contains the granular segmentations, supplier scorecards, and scenario tools necessary to finalize 2026 capital allocations and supplier strategies.

For detailed analysis of this topic, please visit the official page:Aluminum Nitride Ceramic Heaters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com