https://www.facebook.com/Get.ManyoloMaleEnhancementCanada/

Film |

2026-07-10 20:28:36

Between 2020 and 2025 the global 1,8-diaminonaphthalene market has moved from a niche industrial commodity toward a strategically important intermediate across dyes, specialty chemicals and pharmaceutical syntheses. Our base-year analysis (2025) captures a market that has expanded materially from the start of the decade; the transition into the forecast window (2026–2032) projects sustained, mid-single-digit growth with a compound annual growth rate of 6.5% for the forecast period. Under our central scenario the market continues to scale from the high‑90s (USD Million) in 2026 to the low‑hundreds by the early 2030s, reflecting both steady end‑market demand and selective premiumization driven by pharmaceutical and high‑value specialty applications.

1,8-Diaminonaphthalene Market

Actionable timing: 2026 is the inflection year when buyers, producers and investors must choose between defensive supply‑chain hedging and offensive product differentiation. With raw material cycles and regulatory harmonization accelerating, decisions made this year will compound through the 2026–2032 forecast horizon.

1,8-Diaminonaphthalene Market

Portfolio prioritization: firms that treat 1,8-diaminonaphthalene as a strategic intermediate — rather than a commoditized feedstock — can capture margin expansion through grade segmentation, lifecycle services and co‑development with downstream formulators.

1,8-Diaminonaphthalene Market

Risk calibration: primary risks (raw material volatility, transport/regulatory friction, and supplier concentration) are quantifiable and mitigatable with discrete procurement and topology strategies; the report maps those mitigations to P&L impact with scenario sensitivities suitable for board-level planning.

Observed historical growth from 2020 through 2025 demonstrates a clear demand re‑rating: the market base expanded meaningfully, underpinned by recovery in dye and pigment manufacturing and an increased incidence of high‑purity demand from pharmaceutical synthesis. Our forecast to 2032 embeds a 6.5% CAGR, producing a market size trajectory that supports both incremental brown‑field expansions and selective green‑field projects focused on higher‑margin grades.

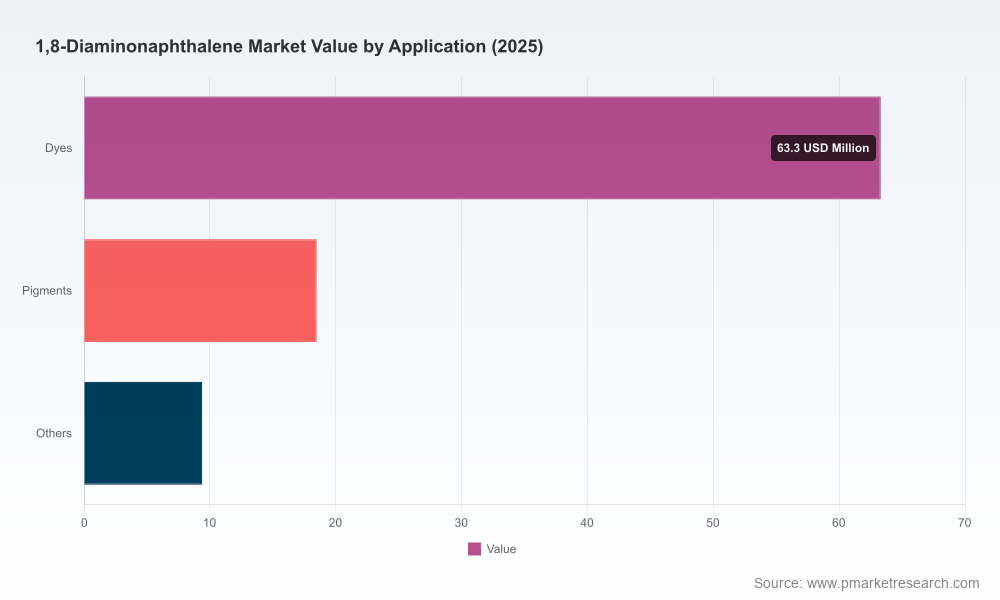

That said, the aggregate growth masks important dynamics we deliberately withhold at this teaser stage: the detailed regional distribution, application‑level shares, and per‑grade price curves. These segmentation matrices are contained in the full report because they are the tactical inputs that enable sourcing decisions, price pass‑through analysis, and capex sizing — and because they are the most commercially sensitive elements for downstream buyers and suppliers.

Raw material sensitivity: Naphthalene feedstock remains the principal driver of near‑term cost volatility. Regional price movements in 2026 indicate firm downstream demand for dye intermediates and show divergent month‑on‑month dynamics across major sourcing geographies. Procurement teams should model exposure across at least three sourcing bands (short‑term spot, mid‑term contract, and strategic inventory) and stress test margins for a realistic set of naphthalene price scenarios.

Transport and documentation: 1,8-diaminonaphthalene’s classification under international transport regulations imposes administrative friction and adds variable logistics costs. Export controls and quality documentation requirements have a pronounced effect on cross‑border lead times and working capital — a factor often underestimated by market participants.

Regulatory overlay: compliance requirements such as registration and substance evaluation frameworks impose time‑to‑market implications for product launches and reformulations. Firms engaging with European supply chains should prioritize registration, labeling and data‑sharing protocols early in 2026.

The market exhibits a concentrated topology at the top end: the three largest players account for the majority of global revenue, and the top five capture a clear, dominant share. That concentration creates a two‑tier competitive structure: large, integrated chemical majors and large Chinese bulk manufacturers, supplemented by regional specialty players and selected custom manufacturers.

BASF SE: plays at the ultra‑high‑purity end with integrated naphthalene chemistry and stringent specifications tailored for pharmaceutical and specialty intermediates. Their technical depth and site integration make them a natural partner for pharma customers seeking quality and regulatory continuity.

Nantong Haidi Chemicals: the largest single-volume producer globally and a leading bulk supplier. Recent product extensions toward refined pharmaceutical variants signal a deliberate push up‑market — an important strategic shift because it pressures mid‑tier suppliers and accelerates premiumization in Asia‑sourced product lines.

Lanxess, Solvay and Evonik: each offers differentiated value — from GMP manufacturing and specialty formulations to customer‑centric technical services. Their presence tightens the corridor for premium, regulated applications where traceability and service define supplier selection.

Other notable players: a cohort of high‑efficiency Chinese producers and Indian bulk suppliers have consolidated cost leadership in industrial grades; several have invested in automation and solvent‑free routes to improve margin and environmental footprints. These firms will remain decisive for pricing dynamics in commodity channels.

Our competitive benchmarking in the full study maps each vendor across a calibrated set of metrics: grade breadth, regulatory certifications, capacity elasticity, geographic presence, margin profile, and partnership readiness. That vendor scorecard is designed to be directly usable for shortlist creation during RFP cycles and for M&A screening.

Product premiumization: select large manufacturers have launched refined pharmaceutical‑grade variants with improved solubility and tighter impurity profiles. These launches compress the time and investment required for downstream customers to qualify new suppliers.

Automation and capacity optimisation: recent capacity upgrades by high‑purity producers delivered double‑digit efficiency improvements and shortened lead times. For procurement and operations teams, that means reconsidering near‑term dependency on spot markets vs. contracted volumes.

Regulatory tightening: harmonized substance evaluation and transport documentation requirements are shifting the cost base. Compliance program readiness is now a commercial differentiator rather than a cost center.

Procurement playbook: implement a tiered sourcing strategy with three elements — (1) strategic contracts with premium suppliers for regulated grades, (2) spot and hedged positions for industrial grades, and (3) a strategic inventory buffer sized to protect critical production lines. Integrate raw‑material scenario modelling into monthly S&OP cycles.

Product & commercial: pursue product premiumization where feasible — whether through higher‑purity variants, co‑development of intermediates, or bundled technical services. For sellers, packaging regulatory assurance and supply‑continuity commitments with premium grades can unlock sustainable margin expansion.

Manufacturing optimization: evaluate selective investments in automation, solvent‑free processes and traceability systems that reduce cost-to-serve and accelerate qualification timelines for regulated customers. Payback windows for such investments are materially improved when synchronized with the 2026–2028 demand uptick we model.

M&A and partnerships: prioritize bolt‑on acquisitions for regional supply security and technical competency over broad, capacity-heavy deals. Strategic partnerships with logistics specialists and regulatory-compliance firms can be quicker, lower-capex routes to mitigate transport and documentation friction.

Regulatory program: allocate resources now to ensure REACH and equivalent registrations are current; build supplier assurance frameworks that document hazard communication and chain‑of‑custody to avoid shipment interruptions.

The full PW Consulting study converts the high‑level implications above into direct, executable materials: a quantified forecast model (2026–2032) with scenario toggles; a supplier scorecard with actionable shortlists for sourcing; detailed regional and application segmentation tables (note: these are gated in the teaser); a price‑curve model linked to naphthalene feedstock scenarios; regulatory and transport compliance checklists; capex sizing templates; and M&A screening criteria coupled with synergies and integration checklists. The study also contains primary interview transcripts, plant‑level site notes, and a buyer‑supplier negotiation playbook.

Board meeting: use the macro trajectory and risk matrix to set acceptable exposure limits and to approve any capex or partnership workstreams tied to the 2026–2028 window.

Commercial leadership: align go‑to‑market with grade‑specific value propositions; mobilize technical teams to convert product premiumization into price realization.

Procurement & operations: implement the three‑band sourcing approach immediately; commence REACH/transport documentation audits to avoid logistical delays.

This briefing synthesizes market sizing, concentration, supply risk and regulatory friction into a pragmatic playbook for 2026. Our full study preserves the granular segmentation and price matrices that enable execution — intentionally gated so that tactical competitors do not access our primary‑research calibrated splits. If your team is preparing sourcing renegotiations, capacity investments, or M&A activity in 2026, the full report and a complementary workshop will convert these strategic directions into an operational roadmap with quantified P&L and cash‑flow outcomes.

To request the full report, the vendor scorecard and an onboarding workshop for executive teams, contact PW Consulting’s market intelligence desk for immediate access and a tailored briefing aligned to your firm’s exposure and objectives.

For detailed analysis of this topic, please visit the official page:1,8-Diaminonaphthalene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com