Europe Dishwashing Detergents Market Demand Rising Across Households

Other |

2026-06-17 09:43:48

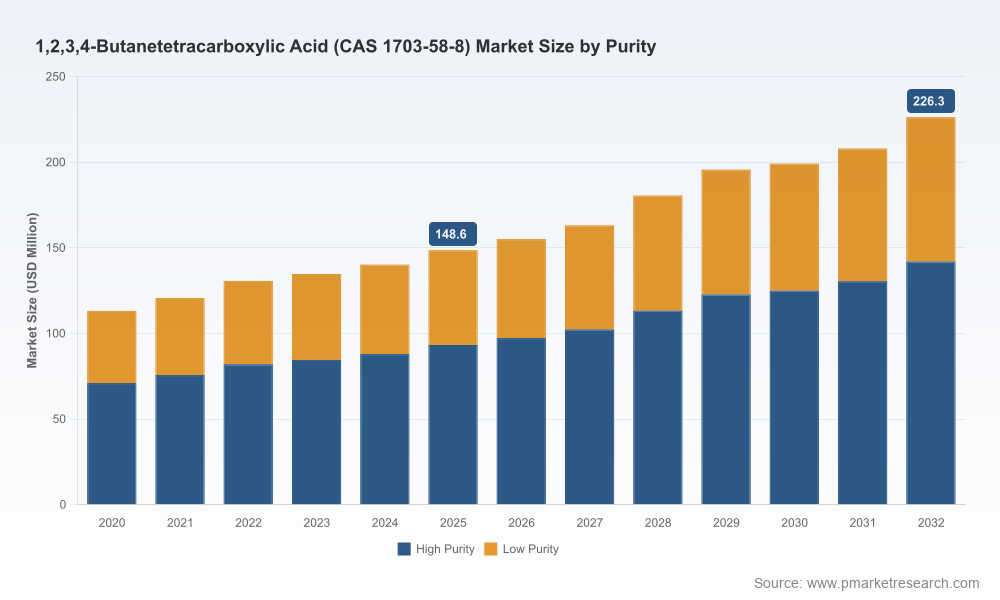

PW Consulting presents a strategic preview of the 1,2,3,4-Butanetetracarboxylic Acid market that crystallizes implications for procurement leaders, R&D heads, investors and corporate strategists preparing decisions in 2026. Built on an evidence-based time series (historical 2020–2025, base year 2025, forecast 2026–2032), this preview distills the macro trajectory—from a market measured at USD 113.15 Million in 2020, rising to USD 148.6 Million in 2025, and projected to reach USD 226.3 Million by 2032—reflecting a forecast compound annual growth rate (CAGR) of 6.3% across 2026–2032—into actionable strategic themes without exposing the granular segmentation tables reserved for the full report.

1,2,3,4-Butanetetracarboxylic Acid (CAS 1703-58-8) Market

Cross-industry applicability: 1,2,3,4-Butanetetracarboxylic Acid is no longer a niche reagent — its role extends across textile finishing, polymer cross-linking, paper chemistry, specialty chemicals and biochemical research. This breadth creates both diversified demand channels and complex go-to-market choices for suppliers and buyers.

1,2,3,4-Butanetetracarboxylic Acid (CAS 1703-58-8) Market

Specialty-versus-commodity divergence: The market is bifurcating into commodity-grade volumes and higher-margin, high-purity grades. Decisions on capital allocation, quality certification and customer segmentation will determine winners.

1,2,3,4-Butanetetracarboxylic Acid (CAS 1703-58-8) Market

Supply concentration and bargaining dynamics: The market exhibits a moderate-to-high supply concentration (CR3 ≈ 68%, CR5 ≈ 78%), producing pronounced implications for pricing resilience, supplier risk and consolidation opportunities.

Regulatory and sustainability pressure: Environmental compliance, waste-water treatment costs, and purity certifications are increasingly important cost and gatekeeping factors in supplier selection and market access.

Demand trajectory and investment timing — read the macro signal: The historical series shows steady growth through 2025 and a clear upward projection into the 2030s. For investors and C-suite planners, this implies that near-term investments (capex for purification, packaging, and export logistics) should be validated against a multi-year demand runway rather than short-term price cycles.

Supply-side structure — leverage the concentration: With a leading cluster of established suppliers and a high CR5, buyers face concentrated sourcing risk but also the opportunity to negotiate value-added service bundles (consignment, quality traceability, JIT deliveries). For sellers, consolidation or strategic alliances can capture scale economies and protect margins.

Margin pressure points — identify non-obvious costs: Energy, feedstock availability, and quality assurance (ISO/GLP certifications) are material drivers of unit economics. Firms that invest early in process optimization and waste reduction can convert compliance into a differentiator.

Geopolitical sourcing realities — diversify with intent: A substantial portion of commercial capacity is located in manufacturing hubs that also service global export markets. Procurement teams should quantify single-source exposures, map logistics corridors, and create contingency pathways for supply interruptions.

Innovation pathways — move beyond incumbent uses: Incremental product innovation (e.g., specialty salts, modified grades for electronics or biotech) and co-development agreements with downstream formulators can unlock premium margins and sticky demand.

Regulatory foresight — pre-empt compliance costs: Anticipatory investments in emissions control and product stewardship reduce the risk of sudden capacity closures or forced retrofits that depress supply and spike prices.

Domestic industrial champions and export-oriented manufacturers: A cluster of China-headquartered manufacturers — with established export footprints, bulk packaging experience and purity-grade capabilities — dominate commercial volumes. Their strengths are scale, cost competitiveness and well-developed logistics into Asia and beyond. Strategic buyers should evaluate long-term contracts with these players while pricing in currency and trade policy exposure.

Branded, global laboratory suppliers: Global suppliers and distributors (including major life-science brands) focus on high-purity research and specialty industrial grades, leveraging global distribution, technical support and recognized product assurance. These players command trust in regulated segments, where traceability and certification are required.

State-affiliated and legacy chemical companies: Suppliers with formal quality systems and broader chemical portfolios can bundle offerings and provide scale resilience, but may carry different commercial terms and lead times compared with nimble private manufacturers.

Implication for M&A and partnerships: Strategic acquisitions should target either (a) capacity for high-purity processing and API-grade production, or (b) downstream formulation capabilities that convert a bulk reagent into a higher-margin specialty intermediate. JV models with local manufacturers offer rapid market access while mitigating greenfield risks.

Procurement: Implement a tiered supplier strategy that blends contracted volumes from established bulk producers, spot access to regional mills, and strategic slots with branded distributors for critical high-purity lots. Insist on quality certificates and sample retention policies.

R&D/Product Development: Prioritize feasibility studies that test new derivative grades for polymer cross-linking or specialty textile finishes. Early collaboration with downstream customers reduces time-to-market and secures volume offtake.

Strategy & Corporate Development: Use valuation trees that treat specialty grades differently from commodity streams. Target acquisitions or minority stakes to gain technical know-how rather than simply incremental tonnage.

Operations: Quantify the total cost of ownership for production upgrades (e.g., purification trains, waste treatment). Capex should be staged and tied to binding offtake or certification milestones.

Comprehensive market sizing & forward projections by year (historic 2020–2025 and forecast 2026–2032), with scenario modelling that stress-tests demand under alternate macroeconomic and regulatory outcomes.

Supplier scorecards and verified company profiles, including manufacturing footprint, purity capabilities, certification status, export channels and commercial terms — enabling shortlist creation for strategic sourcing.

Price-timing intelligence and raw-material cost drivers, with a proprietary pricing model calibrated to historical movements and sensitivity to energy and feedstock shocks.

Regulatory matrix and compliance gap analysis outlining likely cost impacts of environmental regulation pathways across major markets.

M&A screening framework, including prioritized target archetypes, likely synergies, and a transaction playbook for integration and value capture.

Commercial & procurement playbooks: contracting templates, hedging options, inventory policy benchmarks and a negotiation checklist tailored to both high-volume buyers and specialty consumers.

Conduct a rapid supplier concentration audit: map your top 10 suppliers against weighted risk factors (purity risk, logistics exposure, compliance status). Convert the audit into prioritized mitigation actions within 90 days.

Pursue a two-track sourcing model: secure baseline volumes via medium-term contracts with large producers and keep a flexible short-list of specialty suppliers for high-purity needs. Price protection clauses tied to feedstock indices reduce volatility exposure.

Invest selectively in purification and QC capabilities: even modest in-house upgradation can capture margin by enabling the sale of higher-value grades or by reducing reliance on premium third-party lots.

Explore offtake-linked capex: where growth visibility exists, use customer-backed offtakes to de-risk plant expansions or dedicated purification lines.

Embed regulatory foresight into capital plans: prioritize projects that simultaneously reduce emissions and improve product quality, thereby converting compliance into a competitive advantage.

Decision-makers in 2026 face a market that is growing, increasingly specialized and materially shaped by supply concentration and regulatory forces. This preview translates macro growth—anchored in validated year-by-year market sizing—and competitive context into a set of executable strategies. It signals where to commit capital, how to structure commercial arrangements, and what capabilities to build or acquire. At the same time, it deliberately omits granular split tables and proprietary price curves in this public summary to preserve the analytical value of the underlying datasets available in the full report.

For procurement lists, supplier scorecards, detailed segmentation by purity/region/application, full price histories, and the scenario-ready financial model that underpins our 6.3% forecast CAGR, access the PW Consulting full report. The complete dataset includes interactive dashboards and transaction playbooks designed for immediate deployment into 2026 planning cycles.

PW Consulting — translating market measurement into market advantage.

For detailed analysis of this topic, please visit the official page:1,2,3,4-Butanetetracarboxylic Acid (CAS 1703-58-8) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com