Sodium Fluorosilicate Market: Strategic Imperatives for 2026 Decision‑Making

Executive snapshot

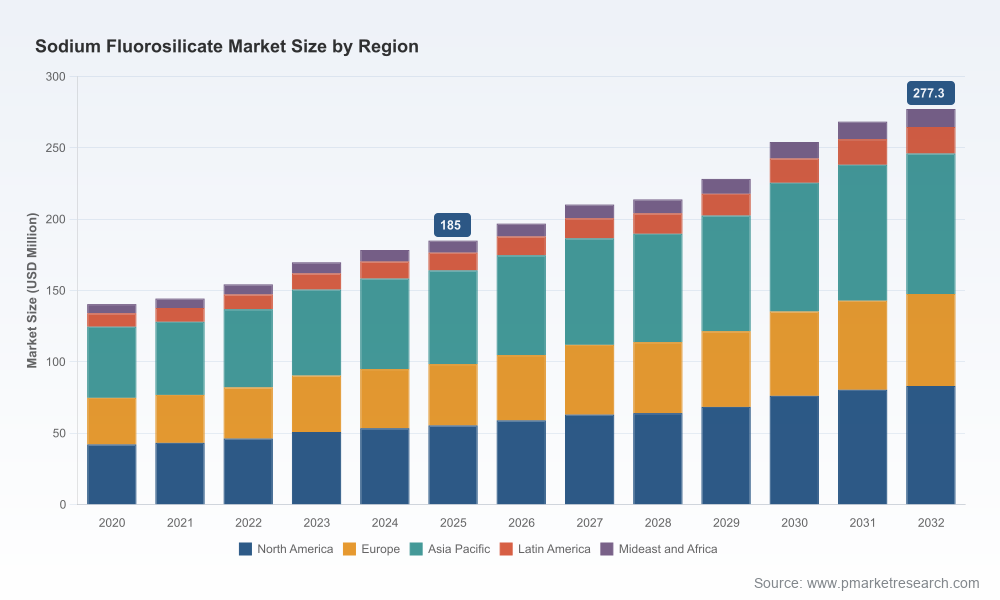

By 2025 the global Sodium Fluorosilicate market reached a defined scale—having expanded from a clear baseline in 2020 and registering sustained growth through 2025. Our base‑year assessment (2025) and the historical window (2020–2025) underpin a forward projection covering 2026–2032 at a compound annual growth rate (CAGR) of approximately 5.25% (USD, revenue unit: Million). Under the assumptions and scenarios modeled in this study, the market is forecast to continue expanding through 2032, reflecting a mix of steady demand in traditional applications and selective growth in specialty channels.

Sodium Fluorosilicate Market

Why this research matters for corporate leaders in 2026

- Timing: 2026 is a pivot year—regulatory updates, supply‑side shocks and incremental product innovations that originated in 2023–2025 are converging to redefine procurement, product development and risk management horizons.

- Decision focus: Capital allocation, contract renegotiation, plant capacity planning and M&A activity all require a harmonized view of near‑term volatility and medium‑term structural trends. This report synthesizes those vectors into actionable scenarios.

- Competitive positioning: The sector displays moderate concentration (CR3 ~37.2%, CR5 ~52.8%), which favors informed strategic moves—selective vertical integration, strategic supply agreements, or product differentiation can materially shift market standing.

What the report delivers (practical, decision‑grade content)

- Market sizing and validated baseline—granular historical reconciliation (2020–2025) and probabilistic forecast (2026–2032) under alternative macro scenarios.

- Demand‑push and supply‑side dynamics—quantified sensitivity to feedstock cost swings, logistics constraints and regulatory shifts, with break‑even analyses for key plant scales.

- Regulatory and standards matrix—clarifying implications of drinking‑water standards (e.g., NSF/ANSI, AWWA specifications), state‑level prohibitions and emerging compliance obligations for producers and municipal purchasers.

- Supplier benchmarking—qualitative and semi‑quantitative profiles of dominant and emergent producers, their capabilities, certifications and strategic differentiators (capacity, product form, approvals).

- Commercial playbook—pricing levers, contract clauses (force majeure, pass‑throughs, minimum take), hedging approaches for feedstock exposure, and procurement scorecards to reduce service disruption risk.

- Innovation roadmap—technical pathways (e.g., low‑dust granulates, slurry handling alternatives), CAPEX/OPEX implications for formulation shifts, and go‑to‑market implications for specialty grades.

- M&A and partnership screen—value creation heuristics for bolt‑on acquisitions, joint ventures with phosphoric acid producers, and strategic offtakes aligned with municipal fluoridation programs.

Market posture: growth, drivers and structural risks

The market’s recent trajectory reflects a blend of anchor demand from water fluoridation and steady industrial applications. From a 2020 baseline through 2025 the sector registered consistent expansion, and our 2026–2032 projection assumes continued underlying demand supported by public health programs, industrial use cases and incremental penetration into specialty chemical segments.

Sodium Fluorosilicate Market

Key drivers we modelled include:

- Regulatory frameworks that sustain municipal fluoridation programs, while imposing tighter product and handling standards;

- Operational innovations that reduce occupational exposure and logistics costs (for example, recent low‑dust formulations); and

- Feedstock cost variability—particularly fluorspar—that propagates through price and availability across producer supply chains.

Sodium Fluorosilicate Market

Regulatory and supply‑chain shocks to watch in 2026

Our dynamics analysis flags several developments that require immediate executive attention:

- Standards and certifications: Compliance with NSF/ANSI Standard 60 and AWWA B702‑18 remains a gating requirement for water fluoridation additives in many jurisdictions. Obtaining and maintaining these approvals materially affects access to municipal tenders and can be a decisive commercial differentiator.

- Localized prohibitions and handling rules: Emerging state and local regulations—examples include prohibitions on slurry forms in some jurisdictions—are creating demand shifts toward dry, certified formulations and alternative delivery methods.

- Raw material inflation and logistics: The industry experienced significant fluorspar input cost escalation and logistics bottlenecks in recent years; producers with vertically integrated feedstock or diversified sourcing exhibited superior margin resilience.

- Geopolitical interruptions: Short‑term supply disruptions tied to geopolitical events have shown how quickly municipal supply can be affected. Risk mitigation requires robust contingency inventory frameworks and multi‑region sourcing strategies.

Competitive landscape: who matters and why

The competitive set is composed of global suppliers and regional specialists. Profiles included in our analysis emphasize product approvals, capacity footprints and go‑to‑market models:

- KC Industries, LLC (Mulberry, Florida) — positioned as a high‑capacity, NSF/AWWA‑approved supplier with a North American manufacturing footprint and municipal focus.

- Derivados del Flúor (DDF, Spain) — a global player with flexible packaging options serving ceramics, enamels and water fluoridation channels.

- Prayon SA (Belgium) — an integrated chemical producer leveraging byproduct streams from phosphoric acid operations to supply treatment markets.

- Solvay S.A. (Belgium) — offers Sodium Fluorosilicate as part of a broader inorganic fluorides portfolio with scale and channel breadth.

- Hunan Heaven Materials & Shanghai Mintchem (China) — regional manufacturers supplying industrial and high‑purity grades for both domestic and export markets.

Each player pursues distinct strategic levers—certifications and packaging flexibility, feedstock integration, or scale and channel breadth. Our competitor scorecard (in the full report) evaluates these firms on technical approvals, demonstrated municipal wins, capacity utilization and innovation pipeline.

Product and formulation trends: practical implications

Recent product innovation underscores a shift toward handling‑friendly forms. A notable launch in late 2025 introduced a low‑dust granulated Sodium Fluorosilicate, reducing airborne particulates by roughly 40% compared with traditional powder. The implications are immediate:

- Manufacturers that adopt low‑dust formats can unlock new municipal contracts constrained by occupational health rules.

- Formulation shifts can reduce field handling costs and liability exposure for water utilities and downstream industrial users.

- Packaging and dosing equipment adjustments are required—creating short‑cycle retrofit opportunities for suppliers of bulk handling systems.

Strategic recommendations for 2026 (C‑suite checklist)

- Procurement resilience: Establish multi‑sourced contracts with staggered delivery terms and include feedstock cost pass‑through clauses. Maintain contingency stock equivalent to a measured proportion of annual municipal commitments.

- Regulatory play: Prioritize NSF/ANSI and AWWA certifications for any product targeting municipal fluoridation. Track state‑level prohibitions and adapt product forms (solid vs. slurry) to retain market access.

- Product differentiation: Fast‑track low‑dust and pre‑dosed formulations where municipal or industrial customers cite handling constraints—this supports premium placement and reduces churn risk.

- Capacity strategy: Conduct a modular CAPEX evaluation—small, flexible lines that can switch between technical and industrial grades minimize capital exposure while capturing incremental demand.

- M&A and partnerships: Target upstream value capture with phosphoric acid or fluorspar partners to mitigate feedstock price volatility; consider bolt‑ons that provide certification, packaging or regional distribution advantages.

- Commercial governance: Align tender response teams with a standardized compliance checklist (certifications, packaging, dosing compatibility, MSDS) to reduce bid turnaround time and rejection risk.

What we deliberately withhold — and why

In keeping with our “trailer” principle, this introduction demonstrates methodological rigor and strategic perspective while omitting the full granular segmentation tables, regional and application‑level percentage breakdowns, and detailed revenue figures by subsegment. Those datapoints are material to customer negotiations and competitive positioning; they are intentionally reserved for the full report and the interactive dashboards accessible via our portal. Executives seeking contract‑grade intelligence, supplier scorecards and downloadable scenario models will find the complete dataset there.

How PW Consulting helps you act

- Rapid‑response briefings: 2–3 day deep dives tailored to procurement teams and plant managers to convert insights into negotiation strategies.

- Deal support: Due diligence packs and integration playbooks for M&A targets in the fluorides value chain.

- Implementation programs: Regulatory certification roadmaps, packaging transition pilots and inventory optimization sprints to reduce near‑term disruption risk.

Closing perspective

The Sodium Fluorosilicate market in 2026 is neither a simple growth story nor a crisis narrative—it is an arena of managed risks and opportunity pockets. Companies that combine disciplined supply‑chain engineering, regulatory foresight and targeted product innovation will convert modest headline growth into outsized commercial returns. PW Consulting’s full study supplies the granular intelligence and executable toolsets to make those moves with confidence; this article outlines the strategic contours and immediate actions senior leaders should prioritize this year.

For detailed analysis of this topic, please visit the official page:Sodium Fluorosilicate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com