Aspirin Market Overview: Key Drivers and Challenges

Other |

2026-04-20 06:18:11

The global Gasket and Seal market has moved from post‑pandemic recovery into a structural growth phase. Between 2020 and 2025 the market expanded from approximately USD 49.1 billion to USD 60.8 billion. Our base year is 2025 and, under the central case in this study, the market is projected to grow to roughly USD 64.8 billion in 2026 and to about USD 83.0 billion by 2032 — reflecting a compound annual growth rate of 4.5% over the 2026–2032 forecast window.

Gasket and Seal Market

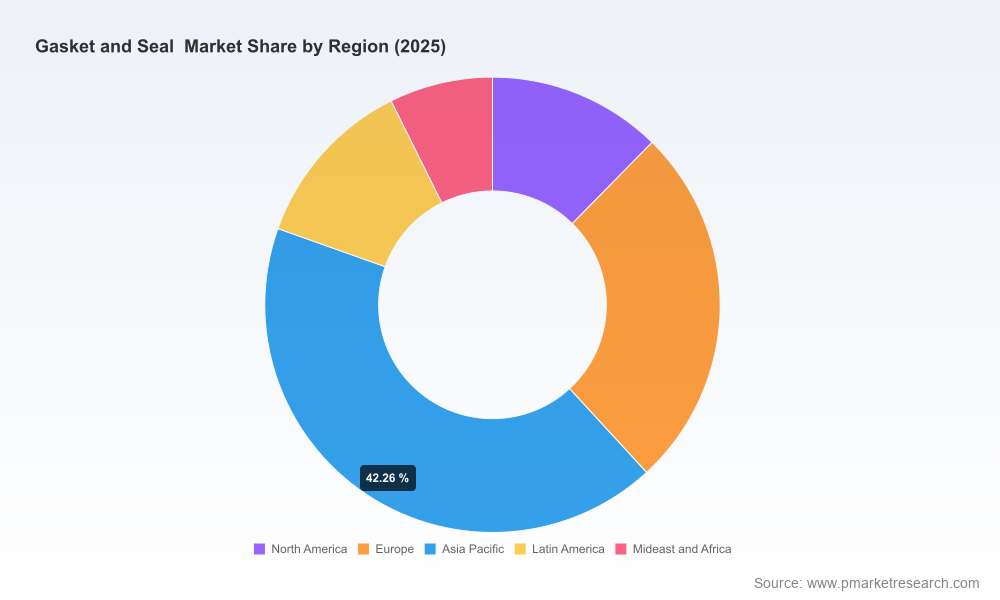

These headline numbers matter for 2026 planning because they are not just directional: they underpin capital allocation, capacity planning, supplier negotiations and M&A prioritization for incumbent manufacturers and new entrants alike. The market exhibits moderate concentration (CR3 ≈ 35%; CR5 ≈ 42%), which means scale advantages exist but there remains substantial room for regional specialists and technology-focused challengers to win meaningful slices of value.

Gasket and Seal Market

Regulatory tightening. Global environmental standards (REACH, RoHS) and emerging restrictions on per- and polyfluoroalkyl substances (PFAS) are accelerating reformulation requirements across sealing materials. For suppliers and OEMs this is a near‑term capex and R&D reality: reformulation cycles, qualification timelines and validation runs will compress in 2026–2027.

Gasket and Seal Market

Raw material volatility. Synthetic rubber and specialty elastomers represent a dominant share of production cost for seals and gaskets — our sector analysis estimates these materials account for roughly 60% of input spend. Natural rubber price volatility (around 234 USD cents/kg as of mid‑2026) is contributing to margin pressure and creates an imperative for robust raw‑material hedging, substitution pathways and close supplier collaboration.

Trade and supply‑chain reshaping. Tariff changes implemented in April 2025 under reciprocal trade frameworks have raised the cost and complexity of rubber‑based imports into certain markets. Coupled with nearshoring trends and the search for reduced lead times, many manufacturers are reassessing manufacturing footprints and regional distribution strategies in 2026.

Customer mix and technology shifts. Electrification, renewables and tighter emissions standards are changing sealing requirements (temperature profiles, media compatibility, lifetime expectations). Suppliers offering high‑performance elastomers, fluoropolymers and advanced composite gaskets are gaining preferential access to OEM programs.

Scenario model suite: three macro scenarios (Base, Accelerated Transition, Protectionist) that translate to demand, pricing and margin outcomes by 2032 and provide sensitivity levers for raw materials and tariffs.

Commercial playbooks: supplier negotiation templates, price‑indexation clauses, and aftermarket monetization frameworks for service and replacement cycles.

CapEx & footprint workbook: demand-driven capacity planning tools that convert top‑line forecasts into site‑level capacity, utilization and ROIC outcomes over 3–7 year horizons.

Regulatory impact matrix: action plans to address REACH/RoHS and PFAS compliance, including reformulation timelines, qualification testing, and cost‑to‑serve estimates.

Raw material stress test: cost build‑ups and hedging strategies tied to elastomer and rubber price scenarios, and a supplier‑risk scorecard.

Competitive & M&A screen: profiles of strategic and financial acquirers, valuation benchmarks and a prioritized target list based on capability gaps and geographic fit.

Procurement and supply risk heatmap: tier‑1/2 mapping, single‑sourced commodity exposure, and alternative‑sourcing playbooks.

Note: to preserve the value of the full intelligence package, this briefing intentionally omits the granular regional and application breakdowns that drive program‑level decisions. Those segmented figures and interactive tables are available in the full report.

The market’s leading suppliers are executing a mix of capacity expansion, portfolio consolidation and selective divestment to sharpen focus. Below we summarize strategic postures and recent moves by major participants covered in our analysis.

Freudenberg Sealing Technologies (Weinheim, Germany) — a materials and systems player focused on elastomers, fluoropolymers and engineered gaskets. Recent investments include a new seal manufacturing facility in Querétaro (announced 2026) and automation of logistics for Corteco, signaling emphasis on cost‑efficient regional supply and just‑in‑time capability. (https://www.freudenberg.com)

Parker Hannifin Corporation (Mayfield Heights, Ohio, USA) — leverages deep engineering in fluid power and aerospace seals. Their competitive edge is program integration with OEMs and a serviceable aftermarket network, making them a preferred partner where performance and qualification depth matter. (https://investors.parker.com/)

Trelleborg Sealing Solutions (Trelleborg, Sweden) — pursuing inorganic growth to broaden polymer and application reach; notable is the acquisition of a sealing specialist (announced 2026), strengthening capability in engineered seals for extreme conditions. Expect continued bolt‑on M&A to fill material or channel gaps. (https://www.trelleborg.com)

SKF Group (Göteborg, Sweden) — recently completed divestment of non‑core operations and announced a rebrand for its automotive business, signaling a tighter focus on sealing and bearing synergies. SKF’s playbook is operational efficiency plus selective portfolio sharpening to improve margins. (https://www.skf.com)

ElringKlinger AG (Dettingen an der Erms, Germany) — specialist in metallic and composite gaskets with a strong footprint in engine and thermal‑management sealing. Their strength is materials and thermal‑cycle expertise, relevant for high‑temperature and combustion applications. (https://www.elringklinger.com/)

John Crane (Smiths Group plc, London) — focused on mechanical seals for oil & gas, chemical and power sectors where uptime and reliability command premium pricing. They remain a go‑to for critical rotating equipment sealing. (https://www.smiths.com/)

Hultec (Houston, Texas, USA) — executed a large capacity expansion (new 167,500 sq ft facility in Spring, Texas, 2025) aimed at pipeline gaskets and infrastructure demand. This is emblematic of regional players capturing infrastructure aftermarket growth. (https://hultec.com/)

Dana Limited, Flowserve, Bruss, Flexitallic and others — these companies cover vehicle drivetrain seals, pump/process sealing, high‑performance industrial gaskets and spiral‑wound metallic solutions respectively. Each occupies differentiated niches where material science, production precision and qualification capability create durable advantages. (https://www.dana.com/, https://www.flowserve.com/, https://www.bruss.de/, https://www.flexitallic.com/)

Supply‑chain resilience is non‑negotiable. Reassess single‑sourced elastomer exposure, add nearshore alternatives for key SKUs, and implement contractual hedges for natural rubber and specialty elastomers.

Invest in reformulation and qualification lanes now. Regulatory timelines mean reformulation costs and qualification test cycles must be budgeted in 2026 capital plans to avoid program delays or disqualification from OEM approvals.

Prioritize automation and flexible manufacturing. Automation reduces labor sensitivity and improves throughput for short lead‑time orders; modular cell designs enable rapid retooling for alternative materials.

Monetize aftermarket and services. Aftermarket replacement cycles and service contracts are higher‑margin revenue pools; manufacturers should productize inspection, renewal and performance monitoring offerings.

Use M&A selectively to buy capability, not just capacity. Targets that add proprietary materials, validated OEM channels, or geographic access will accelerate program wins more effectively than low‑value bolt‑ons.

Embed regulatory and quality milestones into commercial agreements. ISO 9001/TS‑16949 standards remain procurement prerequisites in automotive and industrial programs; contract clauses should allocate responsibility for compliance upgrades and timelines.

Week 1–3: Run the scenario suite with your raw‑material inputs and validate the group's revenue sensitivity to elastomer pricing and tariff exposure.

Week 4–8: Execute supplier scorecards and begin renegotiation using our price‑index templates; launch one qualification project for PFAS‑free formulations.

Week 9–12: Finalize 2027 CapEx submissions using the footprint workbook and prioritize M&A targets from our screened list for follow‑up diligence.

This briefing highlights strategic levers, market trajectory and competitor movement to support executive choices in 2026. To preserve the commercial integrity of the intelligence and to encourage direct engagement, this summary intentionally withholds the detailed regional and application revenue splits, itemized pricing models by material grade, and the full company‑level segment revenue tables that underpin program and bid decisions.

For teams preparing budget allocations, sourcing mandates or transaction mandates in 2026, the full PW Consulting Gasket and Seal Market report contains the granular, workbook‑ready datasets, interactive scenario models, and supplier dossiers required to move from insight to action.

For detailed analysis of this topic, please visit the official page:Gasket and Seal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com