Mattress Ticking Fabric Market Overview: Key Drivers and Challenges

Other |

2026-05-06 06:04:55

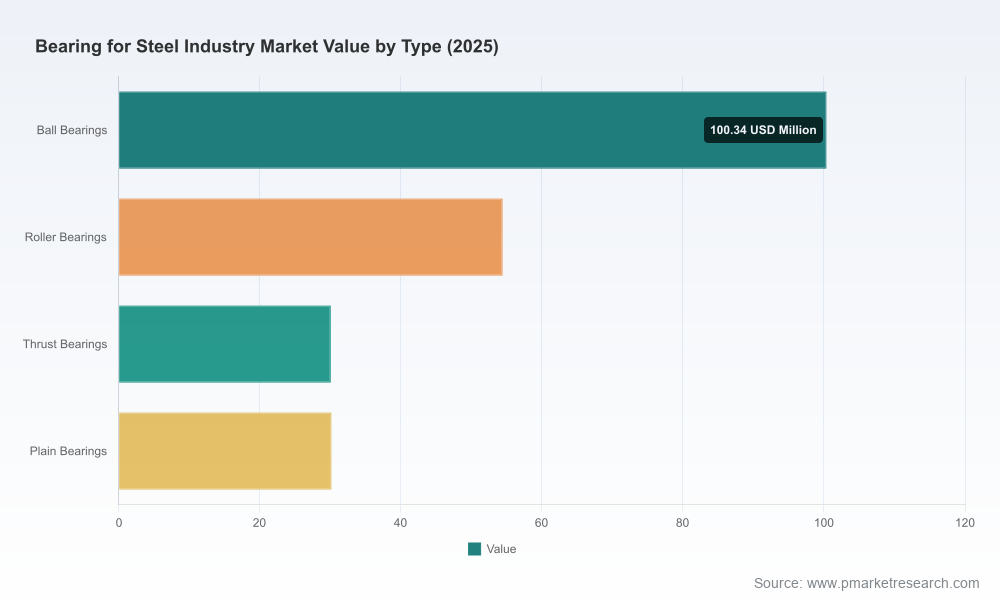

PW Consulting presents a focused primer on our new Bearing for Steel Industry Market study (base year 2025, forecast 2026–2032). This introduction explains why the research is a strategic instrument for executive decision-making in 2026: it translates macro momentum (a market expanding at a 6.98% CAGR across the forecast window) into pragmatic, time‑bound actions for procurement, product strategy, aftermarket services, and M&A. We deliberately foreground the analytical framework and the kinds of actionable insights we deliver, while reserving detailed segment tables and proprietary forecasts for the full report to preserve the value of the underlying dataset.

Bearing for Steel Industry Market

Calibration for capital allocation — The industry is in a mid‑cycle growth phase. After recovering from 2020–2024 volatility, the market base in 2025 provides a stable platform for multi‑year investments in bearing technologies, test rigs, and capacity upgrades. Our modeling shows where scale matters and where niche engineering can yield outsized returns.

Bearing for Steel Industry Market

Procurement and supplier resilience — Bearing-grade steel and precision processing are subject to concentrated upstream inputs and regulatory cleanliness requirements. Sourcing strategies that incorporate dual‑supply approaches, longer qualification timelines, and lifecycle service contracts materially reduce uptime risk in steelmaking applications.

Bearing for Steel Industry Market

Aftermarket and services as margin levers — Lifecycle solutions (reconditioning, condition‑based maintenance, coatings and retrofits) are moving from tactical cost saves to strategic revenue streams. The report quantifies expected demand for lifecycle services and maps operational playbooks for piloting reuse programs.

M&A and partnership screening — The market’s moderate concentration and a mix of global majors and specialised regional players create buy/build/partner opportunities. Our research identifies capability gaps and a screened pipeline of target archetypes aligned to scale, technology, and raw‑material integration.

From a macro perspective the Bearing for Steel Industry market demonstrates steady expansion: the 2020–2025 base establishes mid‑market momentum and the forecast to 2032 reflects sustained demand driven by heavy machinery upgrades, capacity maintenance in steelmaking, and rising expectations for equipment availability. At a 6.98% CAGR through the forecast period, demand growth favors suppliers that combine robust metallurgy, precision manufacturing and service‑led propositions.

Two structural characteristics stand out and shape near‑term choices:

Fragmentation with opportunity — Measured concentration metrics indicate that the market remains competitive, with leading groups holding meaningful but not dominant shares. This creates openings for differentiated entrants that can deliver technical performance or cost‑to‑service improvements.

Upstream integration and material quality — Availability of bearing‑grade steel and heat‑to‑heat consistency are binding constraints for premium bearing producers. Players that secure qualified steel supply chains or retrofit heat‑treatment and coating capabilities will de‑risk qualification cycles for end customers.

The study includes a structured competitive assessment of leading OEMs, specialty manufacturers and key material suppliers. Below are high‑level strategic readouts on core market participants and implications for 2026 planning:

SKF Group (Stockholm) — Continues to invest in advanced bearing steels and premium materials. Their recent launch of a bearing steel optimized for demanding industrial environments signals a push to capture high‑spec industrial applications. Strategic implication: expect SKF to target long‑term framework agreements with steelmakers and heavy‑industry EPCs.

NSK Ltd. (Tokyo) — Piloting lifecycle programs focused on reconditioning and reuse at customer sites. This reflects a shift toward service‑led models that reduce total cost of ownership for steelmakers. Strategic implication: OEMs and service providers should model the commercial impact of reuse on spare inventory policies.

The Timken Company (North Canton, Ohio) — Reinforcing engineered bearing capabilities and industrial motion systems for heavy sectors. Timken’s reported focus reinforces a segmentation strategy around engineered, high‑duty solutions rather than high‑volume commodity bearings.

Schaeffler Group (Herzogenaurach) — Expanding production footprints for large‑size spherical roller bearings and introducing advanced coatings—moves designed to capture heavy‑duty steel and cement industry needs. Strategic implication: regional production and certifications are central to winning long‑cycle OEM contract bids.

JTEKT, NTN, Nachi (Japan) — These players maintain technology depth and diversified product portfolios. Their strategies center on material partnerships, precision grinding capacity and aftermarket networks to sustain competitiveness.

RBC Bearings, Universal Stainless, Aichi Steel, Sanyo Special Steel, Dongbei Special Steel — These companies play roles across precision bearings, specialty alloys, and upstream steel supply. Integration points with bearing manufacturers (material qualification, specialty alloy grades, heat treatment) are decisive in shortening qualification cycles for high‑demand applications.

Across competitors, notable tactical themes include: product launches focused on metallurgy and coatings; regional capacity expansion for large diameters; and trials of reuse/reconditioning programs at major steel producers. These moves are responses to both operational needs of steelmakers and tighter lifecycle/environmental mandates.

The full study is structured to be directly operational for commercial, supply chain, engineering and investment teams. Key modules include:

Market sizing and growth model (2020–2032) with segmented demand scenarios and sensitivity analysis.

Supply chain mapping — upstream steel sources, heat treatment, grinding, and coating nodes with supplier risk scores and lead‑time benchmarks.

Competitive benchmarking — capability matrices, product roadmaps, recent development timelines and strategic intent analyses for leading firms.

Regulatory & standards register — qualification requirements (ISO rolling bearings cleanliness, industrial certification touchpoints) and their commercial implications.

Go‑to‑market playbooks — procurement negotiation templates, tender evaluation frameworks, and aftermarket service pilot designs.

M&A and partnership screen — target archetypes, valuation multiples observed (anonymized), and integration risk checklists aligned to strategic objectives.

Scenario planning workshop toolkit — three to five credible market futures (including demand contraction, accelerated digitization of maintenance, and raw material shock) with decision triggers and contingency actions.

Standardization and cleanliness requirements: ISO‑level standards for rolling bearings in steelmaking continue to tighten. This elevates the importance of heat‑to‑heat consistency and clean room handling in qualification programs.

Material integration: Several steel producers now supply semi‑finished, bearing‑grade alloys into integrated supply chains. Buyers should model supplier tightening and potential advantages for vertically integrated manufacturers.

Labor and maintenance economics: Pilots on in‑field reconditioning are shifting the calculus on spare inventory and mean time between overhaul. Narrowing in on pilot metrics (downtime avoided, reconditioning yield, lifecycle cost) is a practical first step.

For OEMs and steelmakers — initiate supplier tiering and two‑path qualification: secure a qualified primary source for high‑spec bearings while running parallel trials with service providers for reconditioning to reduce total lifetime cost.

For bearing manufacturers — accelerate coating and material R&D; prioritize regional production lines for large diameters where qualification cycles are lengthy and localization drives procurement decisions.

For investors and M&A teams — focus on targets that provide one or more of the following: metallurgy IP, large‑diameter manufacturing capability, or scalable reconditioning/service platforms that can be rolled into existing aftermarket networks.

Q1 — Use our demand sensitivity scenarios to set inventory policy and capital expenditure floors.

Q2 — Run supplier qualification and dual‑source pilots informed by the supply‑chain maps and material risk scoring from the report.

Q3 — Launch lifecycle service trials or engagement with verification programs to test reuse economics and service margins.

Q4 — Reassess strategic partnerships and finalize any M&A or JV moves using the target screens and integration playbooks in the study.

PW Consulting’s Bearing for Steel Industry Market study is designed to be a hands‑on toolkit for 2026: not just “what” is changing, but “how” executives should act. The research combines market economics (with a clear growth trajectory), supplier and material dynamics, competition analysis, and practical playbooks—while preserving the confidential segment matrices and granular data that underpin our recommendations.

To access the full intelligence set—regional and application splits, detailed segment tables, scenario model files, and the supplier scorecards—please visit the report page to request the complete study and supporting datasets. PW Consulting clients can also schedule a strategy workshop to translate findings into a tailored 12‑month execution plan.

For detailed analysis of this topic, please visit the official page:Bearing for Steel Industry Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com