Could New Drug Developments Transform the Treatment of Lazy Eye Disorders?

Networking |

2026-06-08 16:03:52

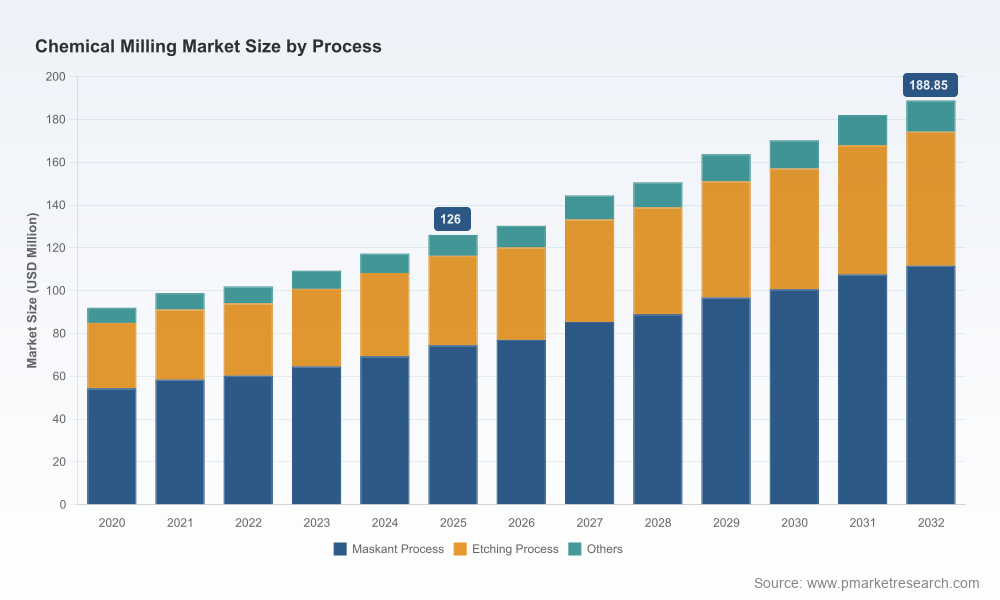

As companies map capital allocation, supplier strategies, and compliance roadmaps for 2026, the chemical milling sector presents a distinct combination of steady expansion, regulatory pressure, and supplier consolidation. PW Consulting’s latest market study (base year 2025; historical review 2020–2025; forecast 2026–2032) shows a market on a reliable growth trajectory — expanding from a low‑hundreds of millions of USD in 2020 to a larger market in 2025, with projections that continue through 2032 at a compound annual growth rate of 6.0%. This preview highlights the strategic implications of that trajectory without publishing the granular segment tables and regional/application splits reserved for the full report.

Chemical Milling Market

Predictability at scale: A mid-single-digit CAGR through 2032 creates a planning envelope that supports multi‑year investments in capacity, compliance, and automation. Companies that adopt a scenario-based investment framework in 2026 will preserve optionality while capturing volume advantages as demand scales.

Chemical Milling Market

Regulatory and raw‑material asymmetries: The sector is asymmetric — certain material-process combinations materially raise cost-to-serve and compliance burdens. Buyers and processors must price and contract around these asymmetries; strategic procurement in 2026 should move beyond unit price to include accreditation status, waste handling, and disaster‑recovery obligations.

Chemical Milling Market

Consolidation and purchasing leverage: The market shows a moderate degree of concentration (CR3 and CR5 metrics indicate that the top providers capture a meaningful share of addressable demand). For OEMs and tier suppliers, this means a concentrated set of partners can deliver scale and specialist capabilities, but also that supplier selection will need to balance availability against potential price and service elasticity.

Scale and momentum: The market has expanded steadily during the 2020–2025 review window and continues to grow under our 2026–2032 forecast. That stability supports CAPEX for new cells, robotic handling, and effluent treatment investments — but only where utilization thresholds are demonstrably reachable.

Accreditation premium: NADCAP and equivalent accreditations are not cosmetic. Across aerospace supply chains, accreditation commonly supports a material price premium. For buyers, accepting non‑accredited supply introduces program risk; for processors, accreditation purchase and maintenance are strategic cost items that must be amortized correctly.

Material‑process cost deltas: Processing different alloys and thicknesses changes chemistry, cycle time, and safety posture. Certain chemistries require more intensive handling and yield higher per‑unit processing economics; these are core drivers of differential margins across providers.

Environmental compliance as a scarcity factor: Tightening regulation on hazardous etchants and effluents is not a future possibility — it is an ongoing cost driver. Facilities face multi‑million dollar compliance investments to retain operations under increasingly stringent standards, altering the supply map and opening returns to operators who frontload compliance upgrades.

Prioritize accreditation and traceability in sourcing decisions. Contracts that attempt to shelter program timelines from supplier accreditation gaps will ultimately transfer risk to OEMs; fixed-price, milestone‑based purchasing tied to accreditation deliverables is recommended.

Model process‑level margins, not just material cost. A procurement decision that optimizes only raw material spend will underperform if it ignores etchant chemistry, cycle times, scrap rates, and treatment costs. In our modeling toolkit we recommend per‑area and per‑cycle costing layers to capture these drivers.

Design for manufacturability to reduce downstream chemical processing. Early design interventions that minimize large, deep etch areas or that partition hard‑to‑process materials can reduce lifecycle cost and regulatory exposure across program timelines.

Invest selectively in effluent and safety infrastructure. Firms that invest to meet current and imminent regulatory standards create upside through higher utilization flexibility and can defend margin under tighter compliance regimes.

Use M&A and JV structures to assemble capability stacks. Given market concentration, acquiring or partnering with accredited, specialty processors accelerates time to compliant capacity and reduces program risk for critical aerospace and defense programs.

The market is served by a mix of specialist processors, vertically integrated metal services, and precision photochemical etching houses. Below we summarize strategic positions of notable providers within the competitive topology; the full report contains comparative matrices, capability heatmaps, and audited supplier scorecards.

Valence Surface Technologies (United States): A full‑service aerospace metal finishing provider. Strengths are breadth of chemical processing across common aerospace alloys and deep program experience for commercial aviation, military, and space programs. Valence’s portfolio emphasizes certification-driven demand and program continuity.

Tech Met, Inc. (Glassport, PA, United States): NADCAP‑accredited precision chemical milling with a focus on forgings, sheet, bar and fabricated parts. Tech Met’s accreditation profile and process discipline position it as a go‑to for critical program work where auditability and repeatability are non‑negotiable.

MET Manufacturing Group, LLC (Mishawaka, IN, United States): Specializes in photo‑chemical etching and precision milling for flat components. MET’s capability to produce burr‑ and stress‑free components up to certain thicknesses makes it attractive for micron‑sensitive assemblies.

Etchit (Buffalo, MN, United States): A custom photochemical machining and milling house with cross‑industry reach. Etchit’s model is tailored to bespoke runs where tooling speed and agility are prioritized over high volume throughput.

VACCO Industries (South El Monte, CA, United States): Known for photo‑chemical etching of stainless steels and specialty materials, VACCO augments etching with micro‑laser and value‑add processes — a strategic advantage for electronics and niche aerospace subsystems.

Great Lakes Engineering (Maple Grove, MN, United States): Supplier of surface mount stencils and precision laser cut parts. Great Lakes’ manufacturing breadth supports customers requiring integrated supply of etched and laser‑cut components.

Ducommun Structural Systems Group (United States): Focused on complex aerospace and structural parts, Ducommun brings high‑value chemical milling for weight‑critical components, with demonstrated ability to deliver aggressive thickness control and structural performance.

Collectively, the supplier set demonstrates the breadth of capability available to OEMs, but also illustrates why accreditation and specialization command price and availability differentials. The market concentration metrics suggest a small number of firms capture a disproportionate amount of demand — a dynamic that will accentuate negotiated leverage by 2026.

Certification churn: The continued maintenance and expansion of NADCAP and related chemical processing accreditations remains a near‑term strategic event. Recent certification activities reported by accredited labs underscore the ongoing importance of audit preparedness and supplier validation.

Regulatory tightening: New and pending regulations on certain hazardous chemistries elevate the cost of compliance and reduce the pool of economically viable suppliers unless they invest in treatment and containment infrastructure.

Material mix shifts: Demand mixes that move toward higher‑performance alloys drive margin dispersion across the value chain; companies exposed to these alloys must price for the increased processing complexity and safety controls.

Actionable market-sizing and forecast (2020–2032) with scenario variants tied to aerospace and industrial production ramps.

Rigorous supplier scorecards and a short list of target acquisition candidates for buyers seeking accredited capacity — built from capability, geographic, and financial filters.

Cost‑to‑serve models by process family and material class, enabling buyers and processors to run what‑if pricing and margin sensitivity analyses.

Capital expenditure playbooks for greenfield upgrades and retrofit options, with payback intervals under multiple utilization scenarios.

Regulatory compliance roadmaps and recommended environmental control investments, aligned to likely permit timelines and capital intensity bands.

Negotiation levers and contract templates designed for multi‑year supply agreements that allocate accreditation, rework, and price escalation risk appropriately.

High‑value annexes: process engineering notes, etchant handling best practices, and an implementation checklist for transitioning specialty jobs between providers.

Treat this document as a strategic orientation: it outlines the dynamics that should shape 2026 decisions without exposing the granular split tables that underpin our primary forecast. If you are an OEM drafting 2026 supplier strategies, a processor planning CAPEX, or an investor evaluating M&A opportunities, the full PW Consulting report contains the calibrated, auditable figures and excutive-ready slide sets you need to operationalize the insights summarized here.

Download the full study to access detailed segmentation tables, supplier scorecards, and the scenario model (note: detailed segment-level numbers and regional/application splits are intentionally gated in the full report to preserve competitive value).

Book a workshop with PW Consulting to run a tailored cost-to-serve or accreditation impact study for your product lines and supplier network.

PW Consulting’s Chemical Milling Market study is designed to convert market forecasts into executable decisions. With an audited base year (2025), a transparent historical window (2020–2025), and a clear forecast horizon (2026–2032 at a 6.0% CAGR), the report gives leaders the tools to prioritize investments, negotiate stronger contracts, and secure compliant capacity as the market scales. For the complete data, supplier matrices, and implementation templates, please visit the report page and schedule your advisory session.

For detailed analysis of this topic, please visit the official page:Chemical Milling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com