Why Some Websites Become Your Go-To Choice Every Time

Music |

2026-07-02 08:31:17

As global seafood markets recalibrate in response to regulatory tightening, supply‑side stress and shifting consumer preferences, the shrimp sector sits at a strategic inflection point. PW Consulting’s latest Shrimp Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes quantitative foresight with operational playbooks to equip executives with the actionable intelligence required to make decisions in 2026 that will determine competitive positioning through the next business cycle.

Shrimp Market

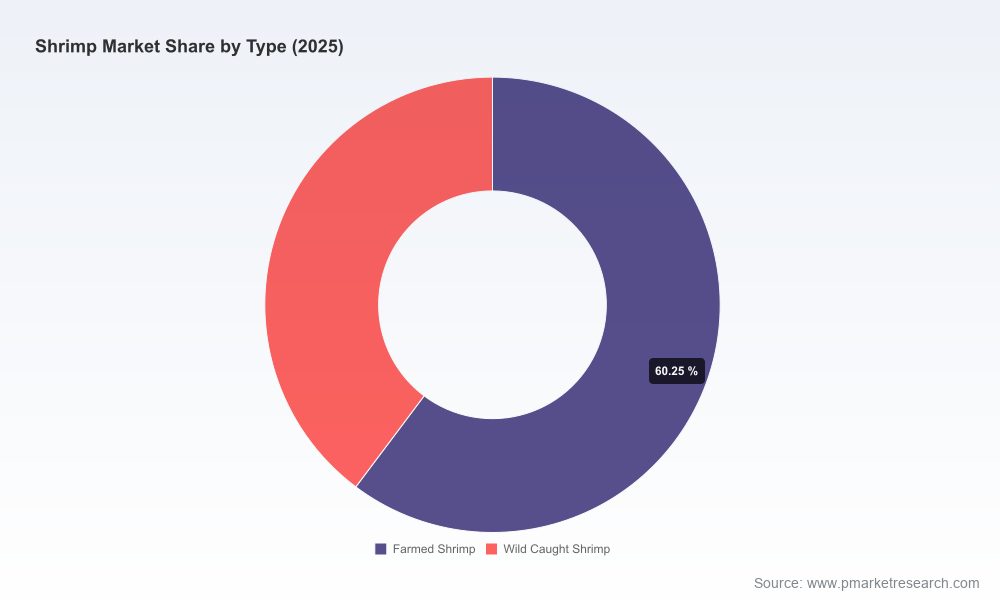

The shrimp market has expanded materially over the last half‑decade, with our base‑year sizing at USD 75.0 Billion (2025) and a compound annual growth rate (CAGR) of 5.5% projected through 2032. The forecast path anticipates the market crossing into the low triple‑digit billions by the end of the decade under a central scenario—underscoring both persistent demand and meaningful upside for firms that can navigate complexity. Market concentration remains relatively low: the top three players account for roughly one‑fifth of global revenues, and the top five for about three‑tenths, signaling significant room for regional specialists, value‑added niche players and disciplined consolidators.

Shrimp Market

Regulatory regime shifts are immediate business risks. Recent policy activity—ranging from import comparability findings and import restrictions to proposed legislative alignment and additions to official species lists—has raised compliance thresholds and reshaped trade corridors. Firms that underestimate these dynamics risk sudden market access constraints and cost spikes.

Shrimp Market

Trade and cost volatility are now structural. Rising input costs, shipping disruptions and trade barrier volatility have amplified margin risk across sourcing networks. Understanding sensitivity drivers (feed, energy, freight and labor) becomes a pre‑requisite for realistic scenario planning and contract design.

Channel and product evolution are accelerating. Retail formats, foodservice procurement models and industrial uses are all evolving—driven by consumer convenience trends, food‑safety expectations and retailer specification enforcement. This creates opportunities for differentiated packaging, ready‑to‑eat formats and premiumization, but also raises the bar on traceability and quality control.

Fragmentation equals opportunity—if you move fast. Low concentration allows well‑executed M&A, geographic expansion or selective vertical integration to materially shift competitive dynamics. That said, an acquisitive agenda requires tight integration playbooks to capture synergies and avoid operational drag.

Our study is built for decision‑makers who need both predictive rigor and field‑tested execution guidance. It combines:

Top‑down and bottom‑up market sizing with scenario variants calibrated to key macro and trade drivers—so executives can stress‑test revenue plans against regulatory shocks, price swings and biological risk events.

Supply chain heatmaps and supplier risk matrices that translate broad trade flows into actionable sourcing priorities, procurement levers and contingency thresholds.

Commercial opportunity assessments by channel and product archetype, paired with GTM playbooks for launching value‑added SKUs, optimizing private label partnerships or scaling direct‑to‑consumer propositions.

Regulatory and compliance trackers that map the practical implications of recent measures (import comparability findings, proposed inspection equivalence legislation, species list updates) to procurement, labeling and certification workflows.

M&A and partnership shortlists, valuation frameworks and integration checklists tailored to the sector’s operating realities—ideal for corporates and private equity seeking inorganic growth routes.

Operational modules on aquaculture best practices, disease management, feed economics, cold‑chain optimization and automation levers to improve unit economics and resilience.

The global shrimp value chain is populated by a mix of vertically integrated producers, specialized processors and global distributors. Key players highlighted in our analysis include established processors and distributors that exemplify distinct strategic models:

Aqua Star (Seattle, WA) — frozen specialty producer/distributor with active processing and sourcing operations; notable for channel reach in North American retail and foodservice.

Clearwater Seafoods (Halifax, NS) — vertically integrated wild‑catch producer with coldwater processing capabilities; useful benchmark for premium wild product strategies and traceability claims.

Mazzetta Company (Highland Park, IL) — importer/distributor with value‑added product focus and sustainability positioning; represents an import‑led commercialization model with branded and private label footprints.

Nordic Seafood (Hirtshals, Denmark) — global importer/distributor that demonstrates the logistics and sourcing agility required to navigate shifting trade corridors.

Surapon Foods (Bangkok, Thailand) — large producer/exporter illustrating the scale and cost competitiveness of certain production hubs.

High Liner Foods (Lunenburg, NS) — processor and marketer of value‑added frozen seafood, with an emphasis on branded innovation in frozen convenience formats.

Wild Ocean Direct (Titusville, FL) — regional processor with dock‑to‑door logistics—an archetype for short supply chains and freshness‑led differentiation.

Our competitive analysis overlays these firm profiles onto capability matrices (sourcing, processing, distribution, brand/margin architecture) and highlights where competitive advantage is durable (e.g., proprietary cold‑chain assets, long‑standing supplier relationships) versus where it is transient (e.g., price competitiveness in spot markets).

Regulatory action has moved from signaling to enforcement: comparability findings and proposed import‑inspection parity measures materially raise compliance costs and can re‑route trade flows within weeks of implementation.

Industry forums and market updates are revealing new patterns: conference agendas and market briefs underline the growing polarity between commodity bulk flows and premium, traceable offerings.

Commercial innovation continues—from ready‑to‑eat packaging rollouts to curated export strategies—demonstrating that product and packaging can be a rapid differentiator when combined with credible sustainability claims.

Immediate (0–3 months): Conduct a regulatory compliance and market‑access audit against the most likely enforcement scenarios; lock in short‑to‑medium term supply contracts with flexible clauses for force majeure and inspection changes.

Near term (3–12 months): Implement a sourcing diversification plan with clear triggers for supplier substitution; pilot traceability solutions (blockchain or serialized labeling) on high‑margin SKUs; accelerate SKU rationalization to reduce cold‑chain complexity.

Medium term (12–36 months): Evaluate targeted M&A to acquire processing capacity, cold‑chain assets or proprietary brands; invest in aquaculture resilience (biosecurity, feed efficiency) to mitigate disease and input cost exposure; roll out premiumized product lines where margins justify traceability and certification costs.

Continuous: Build a monitoring dashboard of leading indicators—feed price indices, freight rates, inspection restriction notices and two‑week lagged order book volatility—to trigger pre‑agreed commercial responses.

Clients leverage the Shrimp Market study in three distinct ways:

Risk mitigation: use the scenario models and supplier heatmaps to quantify probable revenue and margin outcomes under specific regulatory or biological shocks, then hard‑wire hedges and contract clauses.

Growth capture: apply channel playbooks and SKU economic tables to identify the most attractive commercial launches, private label bids or retailer partnerships for 2026 rollout.

Strategic transactions: deploy the M&A shortlists, valuation frameworks and integration checklists to execute accretive deals—either via roll‑ups that consolidate processing capacity or bolt‑ons that extend brand and channel reach.

The 2026 strategic challenge for shrimp sector participants is not simply growth—it is optionality. Firms that build flexible sourcing, deploy robust compliance processes, and invest selectively in product and operational capabilities will retain optionality to accelerate when conditions favor expansion and to pull back with minimal structural damage when shocks arrive. Our Shrimp Market study is designed to be a practitioner’s roadmap: it does not merely forecast volumes and prices; it prescribes the governance, commercial and operational steps necessary to convert market movement into shareholder value.

For executives seeking the granular segmentation, regional and application breakouts, supplier‑level analysis and downloadable modeling tools referenced throughout this introduction, the full report provides the necessary datasets and appendices. Contact PW Consulting or visit our report page to access the complete intelligence package and the decision tools that will shape your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Shrimp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com