Strontium Carbonate Market: Strategic Intelligence for 2026 Decision-Making

Executive snapshot

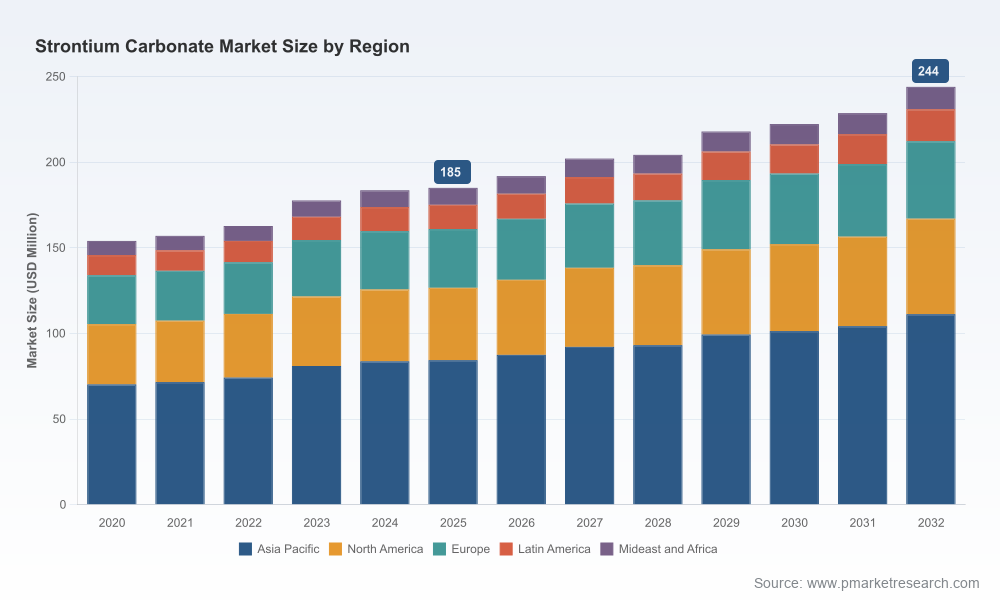

As PW Consulting’s lead industry analyst, I present a focused, strategy-ready overview of the strontium carbonate market that frames critical choices for 2026. Our proprietary base-year is 2025, the historical window spans 2020–2025, and we provide a forward-looking forecast across 2026–2032. The market is growing on a steady trajectory with a compound annual growth rate (CAGR) of 4.1% across the forecast horizon. Global market value has expanded through the past half-decade and is projected to continue rising to materially higher levels by 2032. This briefing highlights the strategic implications of that trajectory while intentionally withholding segment-level granularities to preserve the report’s gating value.

Strontium Carbonate Market

Why this matters for corporate strategy in 2026

- Timing of investment and upgrades: Regulatory forces and technical-transformation requirements introduced in 2025 have created a near-term window where production capacity, especially among legacy assets, will be constrained or undergoing modernization. For buyers and sellers alike, 2026 is a year to decide: accelerate capex to secure advantaged volume/higher-purity capacity, or pursue commercial hedges and contract diversification to mitigate supply shocks.

- Risk-reward in supply concentration: The market exhibits meaningful concentration among top industrial producers. That concentration supports margin stability for incumbents but raises supply-risk for large buyers in tight market episodes. Strategic sourcing and supplier partnerships must be re-evaluated against this backdrop.

- Product-grade premiumization: Differentiation by grade—particularly higher-purity electronic grades—remains a durable route to margin expansion. Firms that can cost-effectively certify and deliver high-purity supplies will capture disproportionate value as electronics and high-end magnet markets continue to demand tighter specifications.

Market snapshot (what the headline numbers mean)

From 2020 through 2025 the global market has shown resilient growth, reflecting steady downstream demand and intermittent supply-side constraints. The 4.1% CAGR through our 2026–2032 forecast reflects a blend of structural demand drivers (electronics, magnetic materials, specialty glass/ceramics, and select industrial uses), regulatory-driven supply rationalization in major producing countries, and incremental opportunities from substitution and recycling initiatives in adjacent chemistries.

Strontium Carbonate Market

Two structural facts underpin our view: first, strontium carbonate remains an intermediate chemical whose demand is closely coupled to end-market industrial cycles rather than purely commodity trading flows; second, changes in production processes and environmental compliance are materially influencing near-term availability and cost curves.

Strontium Carbonate Market

Key dynamics shaping 2026 decisions

- Regulatory modernization and technical upgrades: In 2025 authorities in some producing jurisdictions issued requirements to phase out or upgrade intermittent carbonization processes within constrained timelines. The immediate effect has been planned or actual production reductions and capital projects to meet compliance. For 2026, companies must factor implementation timelines, retrofit costs, and potential downtime into supply contracts and capacity models.

- Geopolitics and raw-material sourcing: Native celestite resources and the logistics of moving feedstock continue to define competitiveness. Some market geographies no longer maintain meaningful domestic production for strontium carbonate and rely on imported celestite or already-processed salts. Procurement strategies that ignore upstream mineral access will face margin and continuity risks.

- Regulatory compliance in consuming regions: Chemical governance frameworks—such as the European regulatory regime—impose stricter substance controls and registration obligations. Upstream producers targeting these markets must invest in documentation, testing, and process hygiene, which raises barriers to entry but also supports a premium for compliant product lines.

- Downstream demand mix and substitution risk: Demand growth in electronics and magnetic materials (including magnets used in motors and certain electronic assemblies) leads to higher demand for electronically specified grades. Conversely, some traditional applications remain sensitive to price and can substitute alternative chemistries if supply tightness or pricing persists.

- Market concentration and commercial leverage: The top-tier producers account for the majority of market volume, creating periods of tightness that favor sellers. Large buyers must therefore incorporate supplier scorecards, dual-source strategies, and contractual protections to avoid price and availability shocks.

Competitive landscape — what matters to 2026 sourcing and M&A

Our analysis profiles the leading industrial players who will shape access, pricing, and technology through 2026. Rather than a simple directory, the strategic lens assesses each player’s role in supply security, technical capability, and potential partnership value.

- Kandelium GmbH (Bad Hönningen, Germany) — As one of the largest global producers, Kandelium is strategically important for buyers seeking calcined granules and specialized sulfide-free grades used in high-end glass and ferrite magnet manufacture. Their capacity and technical know-how make them a logical counterparty for long-term offtake or JV arrangements focused on premiumization and process upgrades.

- Química del Estroncio S.A. (Cartagena, Spain) — With access to local mineral resources and a diversified product mix spanning pigments, pyrotechnics, and ceramics, Química del Estroncio represents a supplier that combines feedstock advantage with regional market reach. For buyers targeting European compliance-ready supplies, this profile is attractive.

- Hebei Xinji Chemical Group (Shijiazhuang, China) — A major exporter for industrial applications, this company typifies the supplier impacted by 2025 retrofit mandates. Its operational status in 2026 will influence global freight flows and pricing; due diligence on specific plant availability and environmental CAPEX commitments is essential for buyers reliant on Asian-sourced material.

- Sakai Chemical Industry (Osaka, Japan) — A producer oriented to higher-purity SW-class grades, Sakai is a strategic partner for electronics-grade demand. Their performance on quality, traceability, and consistency positions them well for OEM supply agreements where material specification is mission-critical.

- Chemical Products Corporation (Cartersville, Georgia, USA) — Serving North American industrial applications, this firm’s integration from celestite (where available) into finished strontium products provides a commercial option for regional buyers seeking reduced logistics complexity and REACH-compatible documentation for exports to regulated markets.

These suppliers vary in terms of technical certification, compliance investment, and geographic risk. Our full profile assessments include plant-level capacity, certification status, compliance timelines, and negotiated pricing benchmarks—elements critical to any 2026 sourcing or M&A decision.

What the full PW Consulting report delivers (practical, transaction-ready outputs)

- Integrated demand-supply model calibrated to 2020–2025 history and stress-tested across 2026–2032 scenarios, with price sensitivities and capacity ramp profiles.

- Regulatory-impact mapping that quantifies the effect of recent 2025 mandates and regional chemical governance on plant availability, compliance capex, and permitted production techniques.

- Supplier due-diligence deep dives: production technology, product-grade matrix, certification status, environmental compliance schedules, and contract negotiation playbooks.

- Commercial strategy frameworks: procurement scorecards, hedge and inventory strategies for buyers, and value-capture templates for producers considering premium-grade plays.

- M&A assessment tools: target-screening criteria, accretion/dilution modelling tailored to grade-mix, and integration checklists focused on process harmonization and regulatory alignment.

- Go-to-market and pricing playbooks for new entrants or incumbents seeking to expand into electronics-grade or specialty ceramic markets.

Actionable recommendations for 2026

- Buyers (OEMs, distributors, converters): Execute supplier resilience reviews now. Negotiate rolling contracts with clearly defined force majeure, retrofit-related downtime clauses, and quality audits. Consider strategic inventory buffers for critical grades while maintaining working capital discipline with structured payment terms.

- Producers: Prioritize compliance spend that unlocks market access (e.g., REACH-ready certification and modernization of carbonization processes). Explore premium electronic-grade product lines where higher ASPs offset CAPEX. Evaluate partnerships or toll-manufacturing to alleviate near-term capital intensity.

- Investors and M&A teams: Target assets with demonstrable compliance roadmaps and access to celestite feedstock. Price-in retrofit timelines and quantify the value of premium-grade conversion capabilities; these are the most reliable levers for margin expansion through 2026 and beyond.

- Policy and risk teams: Monitor ongoing regulatory guidance closely—enforcement timelines and technical standards can materially change production economics. Build contingency scenarios for protracted retrofit timelines or phased implementation that create medium-term supply tightness.

Conclusion — the strategic imperative

2026 will be a year of tactical portfolio shifts rather than purely strategic patience. The combination of stable mid-single-digit market growth, regulatory-driven supply adjustments, and concentrated supply-base dynamics creates both risk and opportunity. Firms that move early to secure compliant, high-purity supply, or to accelerate premiumization strategies, will capture asymmetric returns. Conversely, those who defer will face tightening supplier leverage and potentially higher acquisition or spot-market costs.

PW Consulting’s full Strontium Carbonate Market report provides the granular, transaction-grade intelligence—plant-level assessments, contract templates, price and volume scenarios, and supplier scorecards—required to convert this strategic imperative into executable plans. For organizations making capital, sourcing, or M&A decisions in 2026, the report is designed to be the operational playbook that translates market signals into competitive advantage.

Next step

To access the complete dataset, segmented forecasts, and the full suite of strategic tools and appendices, visit our report page. The executive briefing above is a curated preview that demonstrates the analytical depth and practical relevance of our research while preserving the proprietary segment-level insights that your team will need to act with conviction in 2026.

For detailed analysis of this topic, please visit the official page:Strontium Carbonate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com