Methylal Market 2026 Strategic Preview — PW Consulting

As companies plan budgets, capital projects, and M&A activity for 2026, the methylal value chain is re-emerging as a strategic battleground. Our updated market study, anchored on 2025 as the base year and drawing on a 2020–2025 historical window with forecasts through 2032, highlights a resilient mid-cycle growth profile (4.1% CAGR across the forecast horizon) and a set of immediate decision levers that will matter to producers, downstream formulators, feedstock suppliers and private equity investors over the next 18–30 months.

Methylal Market

Quick snapshot: what the headline numbers mean for strategy

Between 2020 and the 2025 base year the market expanded materially, and under our base forecast the market is projected to continue growing into the early 2030s. That growth is sufficient to support selective capacity additions and premium positioning for differentiated grades, but not large enough to sustain an indiscriminate build-out of commodity nameplate without a clear feedstock or offtake advantage. In plain terms: scale matters, but so does feedstock security and grade differentiation.

Methylal Market

Why this report matters for 2026 corporate decisions

- Capex prioritization: Our scenarios translate the reported CAGR and demand trajectories into utilization bands and payback windows for small-to-mid sized methylal facilities. This reveals where brownfield debottlenecking is likely to deliver faster returns than greenfield builds.

- Feedstock risk mitigation: Volatility in methanol and related intermediates has a direct and immediate pass-through to methylal margins. Our modeling gives CFOs a practical toolbox to stress-test projects under volatile methanol/formaldehyde cycles, and to weight investments in upstream integration accordingly.

- Product & market segmentation: The market supports a bifurcated commercial strategy — premium-grade product lines for electronics, pharmaceuticals and high-purity solvent applications versus cost-focused commodity supply for industrial uses. The study details playbooks for both.

- Regulatory & channel risk: Recent health and environmental regulations have already reshaped end-use eligibility in selected segments. We translate regulatory signals into revenue-at-risk and opportunity maps for 2026 planning.

What PW Consulting’s full study delivers (practical, actionable content)

- Market sizing and demand-supply balance (base year 2025; historical 2020–2025; forecast 2026–2032) with scenarios that reflect feedstock disruptions and regulatory shocks.

- Integrated pricing model that links methanol, formaldehyde and energy inputs to methylal gross margins — Monte Carlo-enabled to quantify probability-weighted outcomes for capex decisions.

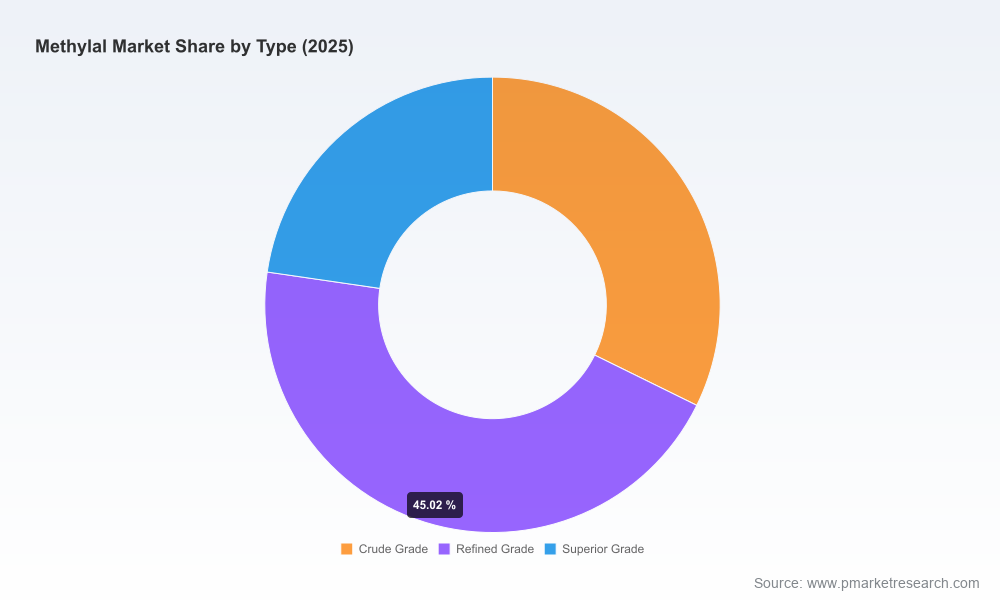

- Segment and application-level demand drivers, use-case profitability mapping and prioritized go-to-market approaches for specialty vs commodity portfolios (note: core line-item splits and regional shares are reserved for the full report to preserve commercial value).

- Supply chain heat-map and supplier risk scores — including suppliers of methanol feedstock, contract structures and logistics chokepoints.

- Regulatory impact matrix and compliance checklist that converts new laws and guidance into specific commercial actions for manufacturers and distributors.

- Competitive benchmarking and acquisition playbook: company profiles, manufacturing footprints, technology differentiators, and criteria for identifying M&A targets or JV partners.

- Investment decision dashboards: IRR/NPV sensitivity outputs, breakeven pricing thresholds, and staged-capex recommendations for safer execution under uncertainty.

Competitive landscape — dynamics and implications

The methylal market exhibits moderate concentration: the top three players control a material but non-dominant slice of global capacity, and the top five increase that share modestly. This structure creates room for both scale plays and regional specialists.

Methylal Market

- Kuraray Co., Ltd. (Japan): With a focus on high-purity methylal under a branded line for electronics and pharmaceutical solvent applications, Kuraray exemplifies a premium-differentiation strategy. Companies competing in high-spec segments should prioritize quality certification, traceability and small-batch logistics on par with Kuraray’s model.

- Prefere Resins (INEOS, Belgium): Producing technical and pure grades for industrial solvents, this type of incumbent benefits from integration into broader chemical portfolios and existing sales channels into coatings and resin customers — a reminder that distribution relationships matter as much as production scale.

- Planet Green Holdings / Jingshan Sanhe Luckysky (USA/China): The group’s recent asset realignment and the resulting impacts on derivative operations underline an important strategic point: corporate restructurings and non-core disposals can create short-term supply shifts and acquisition opportunities for disciplined buyers.

- China-based producers (several mid-sized players): Multiple manufacturers focused on industrial-grade methylal emphasize cost competitiveness. Their presence keeps spot-price discipline in commodity channels and makes premiumization and service differentiation essential for margin expansion.

- LCY Chemical, Chemofarbe, BASF and other integrated producers: These companies highlight another viable model — leveraging methanol and formaldehyde integration, broader product suites and technology platforms to absorb feedstock swings and serve a diverse set of end markets.

Taken together, the competitive set suggests three viable strategic postures for 2026: (1) premium-specialist, (2) integrated commodity supplier, and (3) acquisition-led consolidator focused on regional scale. The right choice will depend on feedstock access, balance-sheet capacity, and appetite for regulatory complexity.

Supply-side volatility and regulatory shocks — what to expect

2025–2026 has already demonstrated how feedstock and policy moves can rapidly change margin equations. Commodity methanol and formaldehyde price swings have led to abrupt cost pushes for methylal producers in some regions, while regulatory steps in certain jurisdictions have restricted specific end uses. At the same time, innovations in feedstock pathways — demonstration projects producing methanol from CO2 and mass-balance bio-sourcing — are emerging as viable strategic hedges that could meaningfully rerate long-term cost curves and sustainability claims.

Key strategic implications:

- Prepare for asymmetric scenarios: regional feedstock shocks can coincide with local regulatory tightening, so global players should build playbooks that combine local commercial agility with centralized risk management.

- Monitor and model emergent feedstock technologies: CO2-derived methanol and mass-balance biosourced supply chains introduce optionality that can be monetized via sustainability premia in certain customer segments.

- Regulatory surveillance is table-stakes: new toxins or product-restriction laws can create near-term demand displacement; proactive reformulation and customer engagement campaigns mitigate revenue erosion.

Key strategic moves for 2026 — an executive checklist

- Run three scenario stress-tests: base-case, feedstock-price shock and accelerated-regulation. Use the study’s pricing model to quantify revenue-at-risk and capital exposure under each scenario.

- Hedge feedstock exposure: consider longer-duration methanol contracts, tolling arrangements, and upstream partnerships. Evaluate pilot investments in alternative methanol pathways where capex and timing align with strategic priorities.

- Differentiate product suite: commit to a clear specialty vs commodity segmentation, investing in quality certifications, traceable supply chains and small-batch customer service for premium grades.

- Prepare an M&A and JV playbook: target mid-market assets that provide regional scale, cost-advantaged feedstock access, or complementary grade portfolios; the market structure favors bolt-on acquisitions where integration can quickly improve utilization.

- Embed regulatory & ESG intelligence: translate new laws into product-level compliance checklists and market-exit/entry thresholds. Use sustainability claims defensibly — investing in third-party verification where customers pay for green premia.

- Revise commercial contracts: incorporate price-adjustment clauses tied to methanol/formaldehyde indices, minimum-volume commitments and flexibility to shift between product grades.

Illustrative 12–18 month actions

- Initiate a pilot with a CO2-to-methanol supplier to test blended feedstock economics and qualify product purity for high-spec customers.

- Run a targeted bolt-on acquisition screen focused on regional cost positions and technical-grade capacity, followed by integration playbooks that deliver >200 bps margin uplift within 12 months.

- Launch a regulatory-forward product stewardship program to protect sales into sensitive end-markets and to convert regulatory risk into a commercial differentiator.

Where the full study adds value

Our full report contains the detailed quantitative underpinnings behind the recommendations above, including the complete historical and forecast market series (2020–2032), granular scenario outputs, interactive price/margin models, and confidential company profiles with operating metrics and strategic diagnostics. To protect the integrity of those proprietary segmentation insights, the report delivers that data interactively and behind a gated access layer — enabling executives and deal teams to drill into the exact split by grade, region and application, and to export scenario outputs for board-level modeling.

For any executive evaluating capacity moves, partnership strategies, or M&A in 2026, the right combination of rigorous financial modeling, feedstock risk management and regulatory foresight will determine whether methylal becomes a growth vector or a volatility risk. PW Consulting’s updated study is designed to turn those uncertainties into quantified choices that boards can vote on in 2026.

To access the complete dataset, segmentation tables, and the downloadable decision dashboards referenced in this preview, please visit our full report page or contact the PW Consulting industry desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Methylal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com