Psyllium Husk Market Forecast: Growth Potential in Emerging Economies

Food |

2026-02-23 09:16:45

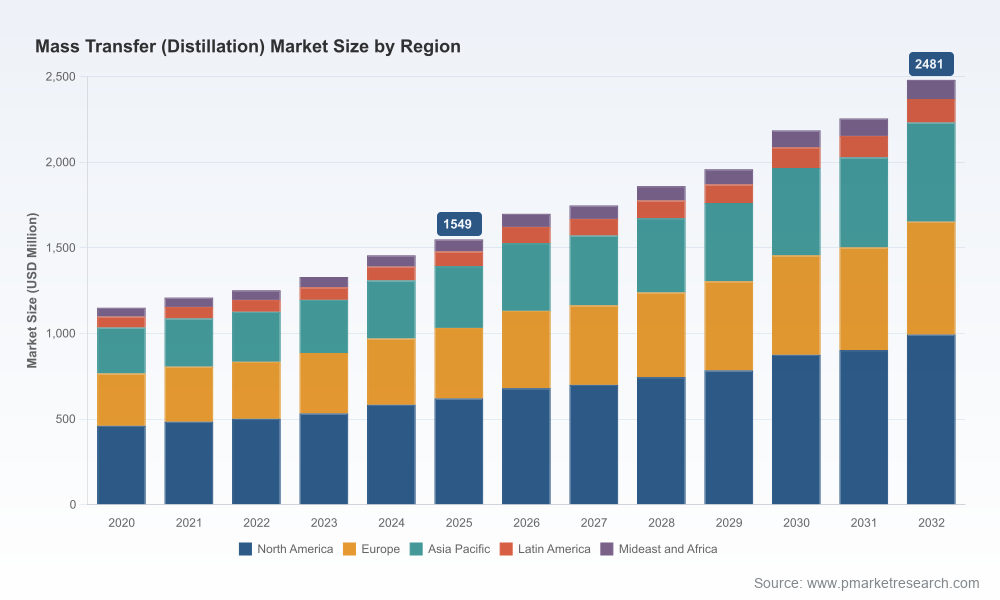

As companies map capital allocation and technology roadmaps for 2026, the mass transfer (distillation) market presents a blend of steady expansion, selective consolidation, and accelerating technology-driven efficiency gains. Our PW Consulting Mass Transfer (Distillation) Market study (base year 2025; historical 2020–2025; forecast 2026–2032) projects a compound annual growth rate (CAGR) of approximately 6.98% through the forecast window. The global market expanded from roughly 1,150 USD Million in 2020 to about 1,549 USD Million in 2025 and is modeled to surpass 2,480 USD Million by 2032 under our base case.

Mass Transfer (Distillation) Market

This briefing distills the strategic consequences of those dynamics for leadership teams preparing budgets, M&A pipelines, and R&D priorities in 2026. It also previews the practical, decision‑ready deliverables contained in the full report while intentionally withholding granular subsegment tables and specific pricing curves — the very assets that unlock tactical execution and are available through our source portal.

Mass Transfer (Distillation) Market

Managed growth with predictable tailwinds: A near‑7% CAGR signals a market that is neither commoditized nor hyper‑volatile. For investors and corporates, this profile supports disciplined growth strategies — targeted capacity additions, selective vertical integration, and staged technology rollouts rather than purely defensive cost cuts.

Mass Transfer (Distillation) Market

Consolidation and supplier power: Market concentration analysis indicates meaningful aggregation among top vendors, creating pockets of supplier pricing power and differentiated technology leadership. This dynamic elevates the importance of supplier strategy — long‑term contracts, performance warranties, and joint engineering agreements become levers to manage price and delivery risk.

Regulatory and energy vectors: Environmental regulations and energy efficiency imperatives are shaping capital allocation across refining, petrochemical, and specialty chemical value chains. Distillation remains central to compliance and product quality, and choices made in 2026 will lock in operational characteristics for a decade or more.

Our historical reconstruction (2020–2025) shows resilient demand driven by incremental refinery upgrades, petrochemical feedstock optimization, and expansion of specialty production lines. The forecast horizon (2026–2032) blends replacement demand with greenfield investments tied to new fuel and polymer projects, and a rising share of retrofit work focused on energy reduction.

Key macro drivers integrated into our modeling include:

Regulatory compliance pressures that sustain demand for solvent recovery and emissions mitigation via distillation systems.

Energy cost volatility and decarbonization pressure that accelerate adoption of lower‑energy separation technologies and electrified approaches.

Upstream feedstock swings and product quality specifications that drive selective investment in column internals and advanced packings.

Technological differentiation is moving beyond materials and geometry into integrated energy systems and process electrification. Manufacturers are showcasing solutions that combine advanced internals with electrified reboilers, process intensification techniques, and digital monitoring to deliver measurable gains in energy consumption per unit product. Our scenarios explicitly quantify energy and operating expenditure (OPEX) impacts across retrofit and greenfield cases, allowing capital planners to compare payback profiles under conservative and accelerated carbon pricing assumptions.

Noteworthy is the industry movement toward electrified distillation modules and electrically driven splitters, which our market model treats as a growing sub‑class with higher per‑unit ASPs but attractive lifecycle savings. Pilots and early commercial deployments have already influenced supplier roadmaps and procurement specifications.

Capex allocation: Prioritize modular, retrofit‑friendly technologies where project obsolescence risk is high; reserve large fixed investments for projects with clear feedstock visibility and long‑term off‑take commitments.

Supplier management: Move from transactional procurement to strategic partnerships with tier‑one internals and packing suppliers. Contracts should incorporate performance milestones, shared risk on energy guarantees, and options for technology upgrades.

M&A and JV tactics: Given market concentration and technology clustering, consider bolt‑on acquisitions to secure intellectual property on advanced internals or to expand service footprints in key industrial hubs. Joint ventures can accelerate entry into emerging product streams such as sustainable aviation fuel (SAF) distillation capacity.

Operational modernization: Accelerate digital upgrades that enable condition‑based maintenance of internals and real‑time energy benchmarking. These investments typically unlock operating margins faster than hardware replacements alone.

PW Consulting’s full report combines strategic context with actionable deliverables designed for procurement leaders, technical directors, and corporate strategy teams. Highlights include:

Transparent market sizing and scenario models (base year 2025, forecast 2026–2032) with sensitivity analyses for energy prices, feedstock shifts, and carbon pricing.

Investment decision frameworks including NPV/IRR templates for retrofit vs greenfield projects and standardized capex/OPEX assumptions tailored to distillation assets.

Supplier scorecards and negotiation playbooks built on capability, lead time, cost, and TCO considerations — benchmarked across the leading providers.

Practical tools: equipment selection guides, retrofit checklists, and commissioning KPI sets for measuring vendor performance post‑installation.

Case studies demonstrating proven energy savings from electrified and intensified solutions, with quantified payback ranges under alternative energy cost scenarios.

Note: In keeping with our "trailer" approach, the executive brief above intentionally omits granular subsegment tables and supplier pricing curves. These are core assets of the full report and are accessible via the PW Consulting portal for subscribers and license holders.

The distillation equipment and internals market is dominated by several established engineering firms and specialist vendors. Competitive positioning rests on three axes: technology breadth (internals, packings, trays), project execution capability, and aftermarket/service reach. Top competitors include global engineering and internals specialists that have demonstrated strategic investment in both product innovation and large project delivery.

Sulzer Ltd. — A technology leader in column internals and energy‑efficient mass transfer solutions, with active development of electrified distillation modules. Recent corporate results underscore strong margins and a focus on distillation/absorption technology lines, signaling continued R&D and commercialization of lower‑energy systems.

Koch‑Glitsch — Known for comprehensive tower internals and phase‑separation solutions, with strength in large refinery and petrochemical retrofit scopes. Their engineering depth makes them a primary partner for complex rearrangement projects.

RVT Process Equipment GmbH — German engineering capability with a focus on trays and packing systems; competitive in Europe for bespoke internals and engineered assemblies.

De Dietrich Process Systems — Combines column fabrication with internals delivery and has a visible presence in chemical and specialty sectors; active exhibitor and technology promoter in industry forums.

Chane Terminal Botlek B.V. — Operator‑centric provider offering toll processing and terminal distillation services, relevant for offtake and third‑party capacity strategies (e.g., SAF processing expansions).

Sepco Process Inc. — Specialist in random packing and separation solutions, playing a key role in retrofit and aftermarket channels.

Recent corporate developments reinforce these strategic themes. Sulzer’s strong 2025 results and selection for large polymer projects underline technology monetization, while Chane’s terminal expansions for sustainable aviation fuel illustrate how third‑party processing capacity can alter project feasibility. Participation by firms such as De Dietrich at major trade shows signals continued investment in customer engagement and solution commercialisation.

Regulation: U.S. environmental programs (e.g., NESHAP and Clean Air Act frameworks) are explicitly driving demand for solvent recovery and emissions‑compliant distillation capacities. These rules create near‑term retrofit needs and long‑term design constraints for new installations.

Technology: Electrified distillation and process intensification are more than lab concepts — early commercial deployments demonstrate substantive energy savings. Adopting these technologies can materially alter lifecycle costs and regulatory compliance profiles.

Infrastructure: Product specification changes (for example, tightening sulfur limits in fuels) continue to impose specialized distillation requirements, affecting column internals selection and service intervals.

Procurement teams should use the market sizing and supplier scorecards to establish long‑list and short‑list partners, while technical teams should apply retrofit checklists and energy scenarios to prioritize pilot investments. Strategy groups will find the scenario models useful for shaping M&A screens and JV deliberations. Executives preparing capital budgets should adopt a two‑track approach: fund critical compliance and energy efficiency projects now, and allocate optionality for technology adoption contingent on pilot outcomes and energy price paths.

This briefing outlines the strategic contours you need for 2026 decision‑making: a growing market with predictable expansion, concentrated supplier dynamics, and a clear technology inflection toward electrification and intensification. The full PW Consulting Mass Transfer (Distillation) Market report delivers the missing granular intelligence — subsegment revenue curves, supplier pricing matrices, detailed CAPEX/OPEX models, and executable procurement playbooks — resources that convert insight into deliverable action plans.

Access to the full dataset and operational toolkits is available through our report portal. For teams preparing capital plans and supplier strategies this year, those assets can shorten decision cycles, reduce procurement risk, and improve the speed of realizing energy and compliance benefits.

For detailed analysis of this topic, please visit the official page:Mass Transfer (Distillation) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com