Soldering Flux Paste Market — Strategic Imperatives for 2026 Decision‑Makers

Executive snapshot

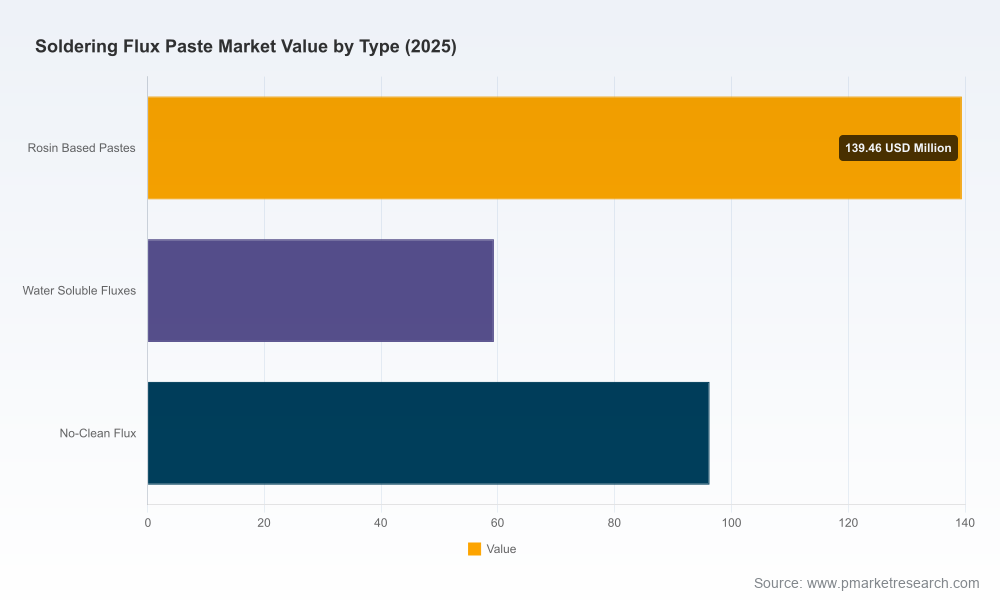

Between 2020 and 2025 the global soldering flux paste market expanded steadily, driven by ongoing electronics assembly demand and incremental improvements in flux chemistries. Our base‑year analysis (2025) shows the market at USD 295.0 Million (USD Million basis), having grown from USD 220.0 Million in 2020. Under the baseline projection the market is expected to continue at a compound annual growth rate (CAGR) of approximately 5.1% through the 2026–2032 forecast window, reaching roughly USD 418.4 Million by 2032. Market structure is moderately concentrated: the top three players control a majority share while the top five approach three‑quarters of industry sales — a dynamic that shapes competition, pricing power and M&A math.

Soldering Flux Paste Market

Why this 2026 research matters — the decision value proposition

- Speed: In an environment of commodity shocks and regulatory tightening, the ability to compress market study timelines into executable actions can determine contract profitability and product roadmaps for the next 24 months.

- Risk mitigation: The report converts macro trends (raw material price volatility, regulatory change) into quantified scenario impacts for procurement, product costing and capital planning.

- Commercial focus: We frame go‑to‑market options for premium vs. volume strategies, showing where investments in formulation, certification or service add the most ROI.

- Competitive intelligence: Benchmarking of incumbent innovators and regional challengers identifies white spaces for partnerships, licensing and bolt‑on acquisitions.

- Operational playbooks: Practical templates for supplier scorecards, hedging strategy and reformulation timelines remove cognitive load for procurement and technical teams.

Core market forces that will drive 2026 decisions

Our analysis isolates three near‑term dynamics that require active management in 2026.

Soldering Flux Paste Market

- Raw material volatility and margin pressure: Refined tin — a principal input for many solder systems — registered a material price uptick in 2025 (the New York dealer price averaged 1,600 cents per pound, about a 13% rise year‑on‑year). That movement translated into compressed input margins for flux formulators and incentivized both price pass‑through and reformulation to reduce metal dependency. Buyers and manufacturers must adopt hedging and cost‑pass‑through playbooks to protect margins.

- Regulatory push towards safer chemistries: Across 2024–2025 regulatory tightening on volatile organic compounds and certain hazardous substances forced many manufacturers to reformulate or certify alternative chemistries. Compliance risk is now a commercial differentiator: early‑mover manufacturers which achieved compliance while preserving performance have secured preferential placements with high‑reliability OEMs.

- Technology and application mix evolution: The market continues to be shaped by higher‑density SMT assemblies, advanced semiconductor packaging and evolving industrial soldering needs. These application shifts prioritize performance attributes — residue behavior, compatibility with lead‑free alloys, and reworkability — which in turn determine where incremental R&D spend yields the largest commercial payoff.

What the report delivers — practical, actionable content

This study is designed as a strategic toolkit rather than a descriptive document. Key deliverables include:

Soldering Flux Paste Market

- Integrated market model (historical 2020–2025 and forecast 2026–2032) with sensitivity toggles for commodity, regulatory and demand scenarios — enabling “what‑if” analysis in minutes.

- Supplier benchmarking dashboards covering product portfolios, certification footprints, channel reach and service capabilities for major and emerging players.

- Segment‑level demand drivers and adoption curves (by formulation type and application class) converted into investment horizon recommendations for R&D and manufacturing capacity.

- Regulatory compliance roadmaps — timebound actions to address VOC and hazardous substance restrictions, plus certification sequencing to secure premium OEM contracts.

- Price and margin models that map refined tin, resin and additive costs to finished paste pricing, with recommended hedging bands and contract clauses for manufacturers and large buyers.

- Commercial playbooks for distributors and manufacturers: SKU rationalization, channel incentives and co‑innovation frameworks to accelerate adoption of next‑generation fluxes.

- M&A and inorganic growth playbooks tailored to different acquirers (strategics vs. financial sponsors), including target archetypes, valuation drivers and integration checklists.

Competitive landscape — what incumbents and challengers are doing

The market is characterized by a small set of well‑known global manufacturers and a broader layer of regional specialists. Notable profiles we analyze in depth include:

- Kester (Philadelphia, PA) — a long‑standing leader with broad capability in no‑clean and tacky formulations compliant with IPC classifications. Kester’s strength is deep application engineering support and global channel reach, which sustains premium positioning in high‑mix assembly settings.

- Indium Corporation (Clinton, NY) — known for innovation in halogen‑free and high‑reliability flux pastes. Recent recognition underscores its R&D momentum: one of its formulations received industry awards in early 2026 and it launched a new no‑clean product line in December 2025 targeted at reflow and hand‑soldering applications. These moves exemplify how product awards and timely introductions convert into procurement shortlist status with OEMs.

- MG Chemicals (Vancouver, BC) — competes on targeted formulations and supply reliability for both leaded and lead‑free alloys, appealing to both electronics manufacturers and industrial users where service consistency matters most.

Across the competitive set, three differentiating axes emerge: formulation science (performance vs. sustainability), application engineering (integration and rework support) and commercial model (direct sales vs. distributor ecosystem). The market concentration metrics highlight that scale — with the top three controlling a majority share — provides negotiating leverage on raw material procurement and the ability to invest in compliance and new product introductions.

Strategic recommendations by corporate role — what to prioritize in 2026

- Flux manufacturers: Prioritize reformulation roadmaps that meet tightening VOC/hazard standards without sacrificing key performance metrics. Allocate a portion of R&D to low‑capex retrofit kits that can convert existing SKUs for compliance. Establish longer‑term raw material contracts with indexed pass‑through clauses and explore vertical relationships upstream for critical inputs.

- OEMs and EMS providers: Treat flux selection as a source of quality and cost advantage. Insist on validated lifecycle profiles and supplier contingency plans. Use the projected baseline growth and scenarios to size safety stocks and contract durations.

- Distributors: Differentiate via engineering services, certification support and inventory financing for customers migrating to compliant chemistries. Build bundled offerings that include flux, process audits and rework training.

- Private equity / strategic acquirers: Look for regional formulators with strong OEM relationships and proprietary chemistries as bolt‑on targets. Value accretion is most predictable where scale can be applied to procurement, compliance overhead and cross‑selling into adjacent assembly consumables.

Scenarios and triggers — watch these to pivot fast

- Upside scenario: Faster adoption of halogen‑free, no‑clean fluxes in emerging packaging results in higher‑than‑expected premiumization, accelerating market value beyond baseline.

- Downside scenario: A sustained commodity shock (sharp tin appreciation or supply disruption) compresses margins and delays non‑essential capital projects across OEMs, softening demand growth.

- Regulatory trigger: New VOC or hazardous substance thresholds enacted in key manufacturing hubs could accelerate requalification cycles and create short‑term shortages for noncompliant SKUs.

- Innovation trigger: Breakthroughs in flux chemistry that materially reduce metal dependency or enable superior reworkability would re‑rank supplier positioning quickly.

How to use the report in 2026 — practical next steps

- Run a 90‑day strategic workshop with procurement, R&D and commercial teams using our scenario model to quantify exposure and opportunity.

- Adopt the supplier scorecard from the report and field a rapid audit of top suppliers for compliance and continuity against the report’s checklists.

- Use the price/margin calculator to renegotiate supply agreements with indexed passthroughs or to set hedging thresholds for refined tin and resin inputs.

- Commission a tailored M&A screen built from the report’s target archetypes if inorganic expansion is part of your 12–24 month plan.

Conclusion — why PW Consulting’s solder flux intelligence matters for 2026

Decision windows in 2026 will be defined by speed and precision. Manufacturers who can translate commodity and regulatory stress into structured reformulation, contractual protections and targeted commercial plays will gain disproportionate advantage. Our report converts the market’s macro trajectory — a mid‑single‑digit CAGR and a clear concentration among incumbents — into operational tasks and investment priorities that can be executed within quarters, not years. For teams planning procurement cycles, product roadmaps, or M&A activity in 2026, the study provides the modeling, templates and competitor insight necessary to move from analysis to action.

For the full segmented intelligence — including regional and application breakdowns, product‑level pricing curves, and supplier scorecards — access the complete report and supporting datasets on our website. The public summary here is intentionally selective to preserve the tactical data that will directly inform negotiation and investment decisions.

For detailed analysis of this topic, please visit the official page:Soldering Flux Paste Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com