Crude Oil Market Dynamics: Key Drivers and Restraints

Other |

2026-03-16 05:41:35

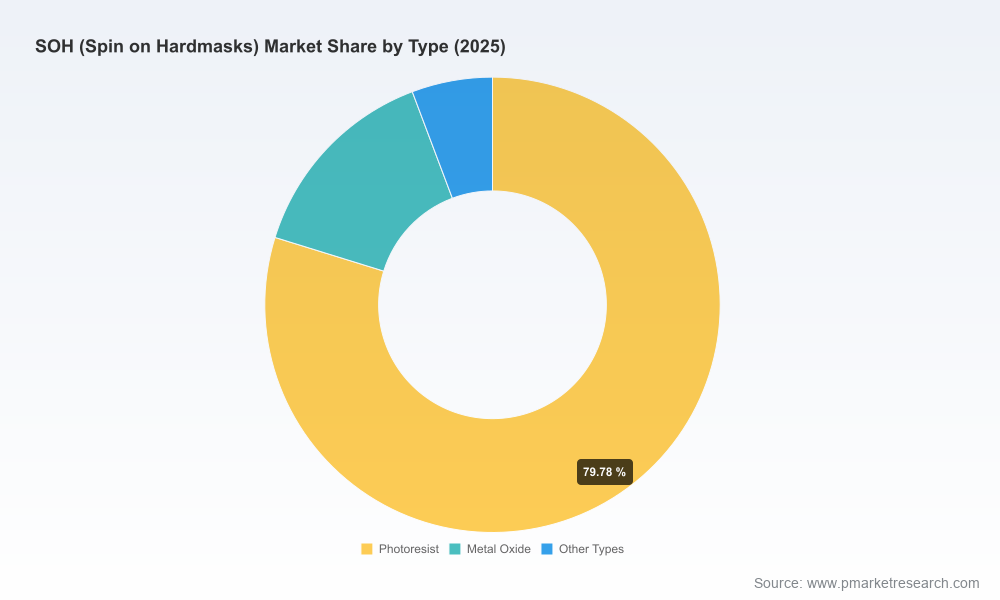

The Spin‑on Hardmask (SOH) market is entering a phase of strategic consolidation and technology maturation that will materially influence capital allocation, supply‑chain design, and R&D roadmaps in 2026 and beyond. PW Consulting’s new SOH Market study synthesizes seven years of historic performance (2020–2025) and a multi‑year forecast (2026–2032) to translate market trends into executable decisions. In brief: the addressable market expanded from a five‑year base to a robust mid‑hundred‑million USD industry in 2025, and under our base forecast the sector grows at a steady mid‑single‑digit compound annual growth rate (CAGR), reaching the upper end of its projected range by 2032. This preview outlines the study’s strategic value while preserving the proprietary segmentation and granular modelling reserved for the full report.

SOH (Spin on Hardmasks) Market

Patterning economics and throughput: SOH solutions continue to displace more capital‑intensive CVD and PVD hardmask steps in specific process flows. For fabs targeting cost and cycle‑time compression at advanced nodes, SOH enables streamlined process stacks that can reduce capital equipment touchpoints and accelerate qualification cadence.

SOH (Spin on Hardmasks) Market

EUV / High‑NA readiness: Next‑generation hardmask chemistries are converging toward EUV and High‑NA EUV compatibility. Early customer engagements and initial qualifications are emerging in 2026–2027, which means OEMs and fabless firms must plan product‑qualification roadmaps today to avoid being late to node migrations.

SOH (Spin on Hardmasks) Market

Risk and resilience: SOH suppliers are embedded in geographically diversified supply chains that are sensitive to raw‑material price volatility and evolving environmental regulation. Procurement strategy in 2026 must balance cost optimization with multi‑sourcing and technical qualification buffers.

PW Consulting’s base‑year analysis shows the SOH market reached a material scale by 2025. Under our forecast horizon (2026–2032) the market grows at a 7.25% CAGR, driven by continuing semiconductor manufacturing investments, broader adoption of spin‑on approaches for certain patterning steps, and incremental use cases in 2.5/3D‑IC and MEMS. For decision‑makers this means predictable top‑line expansion combined with pockets of rapid change where materials and process qualifications converge.

Two implications follow: first, R&D and procurement planning horizons should be extended to capture multi‑phase qualification cycles; second, corporate finance teams must incorporate scenario buffers for both accelerated adoption and slower, regulatory‑driven rollouts.

Regulatory and policy tailwinds: Supportive government programs — including major semiconductor sovereignty and incentive initiatives — continue to underwrite fab capacity expansions in key geographies. These policies sustain demand for SOH as part of new tool chains, but they also elevate documentation, environmental compliance, and traceability requirements for suppliers and chemical partners.

Supply chain and formulation advances: Established suppliers are investing in high‑planarization SOC (spin‑on carbon) and metal‑oxide formulations for sub‑5nm EUV multi‑patterning. The consequence for buyers is that supplier roadmaps are as important as current product performance; vendor selection must incorporate technical development pipelines and foundry qualifications.

Raw material and sustainability pressure: Volatile specialty chemical costs and amplified ESG scrutiny are pressuring margins and procurement strategies. Buyers should model total cost of ownership (TCO) that includes waste treatment, emissions compliance, and substitution risk for critical precursors.

Technology validations and cross‑platform integration: Recent technology validations—such as silicon‑organic hybrid integrations on silicon photonics platforms—signal that cross‑domain compatibility (photonic‑CMOS, 3D‑IC stacks) will become a differentiator for SOH materials designed for heterogeneous integration.

The SOH supplier ecosystem spans large diversified chemicals groups, specialty material houses, and targeted innovators. Market concentration remains modest: the top few firms do not yet dominate the majority of market value, indicating room for nimble entrants and differentiation through tech performance or supply assurance.

Samsung SDI (Seoul): Leveraging integration experience and coating know‑how, Samsung SDI positions SOH materials as a pathway to streamline wafer‑level patterning and displace certain CVD steps where throughput and cost are decisive.

Merck Group (Darmstadt): With a deep portfolio in thin‑film hardmasks and spin‑on carbon chemistries, Merck’s qualifications at Tier‑1 foundries underscore its role as a straight‑line partner for fabs pursuing volume transition plans.

JSR Corporation (Tokyo): JSR focuses on carbon‑rich SOC formulations with low outgassing and high planarization targeted at EUV workflows, positioning itself for advanced node multi‑patterning demands.

Shin‑Etsu Chemical (Tokyo): Known for foundational resist and underlayer products, Shin‑Etsu’s SOH offerings are aimed at integrating middle and under‑layer functionality into nanofabrication stacks.

Brewer Science (Rolla): Brewer Science’s OptiStack multilayer systems emphasize process integration—combining SOC and silicon hardmask layers for advanced pattern transfer and multilayer lithography.

Pibond Oy (Helsinki): As a specialist in spin‑on metal oxide hardmasks, Pibond is carving a niche in 2.5/3D‑IC and MEMS markets where unique stencil and planarization properties are required.

Nano‑C (Los Alamos): Nano‑C’s fullerene‑based SOC chemistries target etch‑selectivity improvements and are attractive to process engineers seeking incremental yield gains in plasma etch sequences.

For strategic procurement and R&D teams the takeaway is straightforward: supplier selection should be scored on a matrix of technical readiness, foundry qualifications, roadmaps to EUV/High‑NA compatibility, and supply‑chain resilience — not purely on price per unit.

This report goes beyond descriptive market sizing to provide tools and frameworks that directly inform 2026 decisions. Highlights include:

Decision playbooks for OEMs, foundries, and fabless companies covering supplier qualification timelines, milestone gates, and contract templates for staged adoption.

Technical maturity maps that align material chemistries to process nodes and lithography classes (incl. EUV/High‑NA scenarios), with pragmatic recommendations on qualification sequencing.

Supplier scorecards and negotiation levers—covering technical, commercial, and ESG dimensions—designed to accelerate sourcing cycles while protecting margin and continuity.

Scenario‑based financial models and TCO calculators that capture raw‑material volatility, waste‑handling costs, and capex/opex tradeoffs for replacing CVD steps with spin‑on flows.

Playable risk mitigations for supply‑chain shock scenarios and regulatory tightening, including dual‑sourcing templates and chemical substitution ladders.

Executive dashboards and quick‑reference decision logs tailored for board‑level briefings and investment committees assessing fab expansions or vertical‑integration choices.

Embed SOH qualification into node migration plans now. Execute parallel qualification tracks (pilot line + multi‑foundry validation) to avoid getting behind the 2026–2027 window when EUV/High‑NA engagements accelerate.

Shift supplier evaluation from price to resilience. Require transparent sourcing of precursors, emissions footprints, and continuity plans as part of RFQs and long‑term supply agreements.

Fund modular R&D collaborations. Partner with specialist suppliers on co‑development agreements that share qualification costs and expedite integration—especially for SOC and metal‑oxide blends tailored to multi‑patterning.

Model procurement under volatility. Use the report’s TCO templates to run stress tests on raw‑material shocks and regulatory cost exposures, then bake flexible clauses into contracts (e.g., price collars, pass‑throughs tied to defined indices).

Prioritize manufacturability and metrology readiness. Ensure that inline metrology and etch recipes are part of early OEM/foundry discussions so that SOH adoption does not create downstream yield cliffs.

Consider this article a strategic trailer: it reveals key directions, competitive posture, and the programmatic tools required to act in 2026, while reserving the granular, commercially sensitive segmentation and detailed supplier scoring for the full SOH Market report. The full study contains the exact segmentation matrices, regional and application breakouts, modelled qualification timelines, and downloadable spreadsheets that procurement, R&D, and corporate development teams will use to operationalize the strategies outlined above.

For teams preparing capital plans, supplier contracts, or R&D roadmaps in 2026, our advice is immediate and concrete: incorporate SOH pathways into node migration scenarios today, stress‑test supplier commitments against regulatory and cost volatility, and prioritize partnerships that deliver foundry‑level qualifications rather than point performance wins.

If you are evaluating fab expansions, technology partnerships, or procurement strategies in 2026, schedule a briefing with PW Consulting to walk through the full report, model outputs, and a tailored action plan for your organization.

Accessing the report unlocks our supplier scorecards, scenario models, and a 12‑month qualification timeline template you can adapt to your internal gate process.

PW Consulting’s SOH Market study is designed to convert market intelligence into executable corporate actions. The sector’s steady CAGR and clear technology inflection points create an advantageous context for organizations that move early, partner smartly, and build resilience into their supply models. The full report provides the data, models, and playbooks you need to make those 2026 decisions with confidence.

For detailed analysis of this topic, please visit the official page:SOH (Spin on Hardmasks) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com