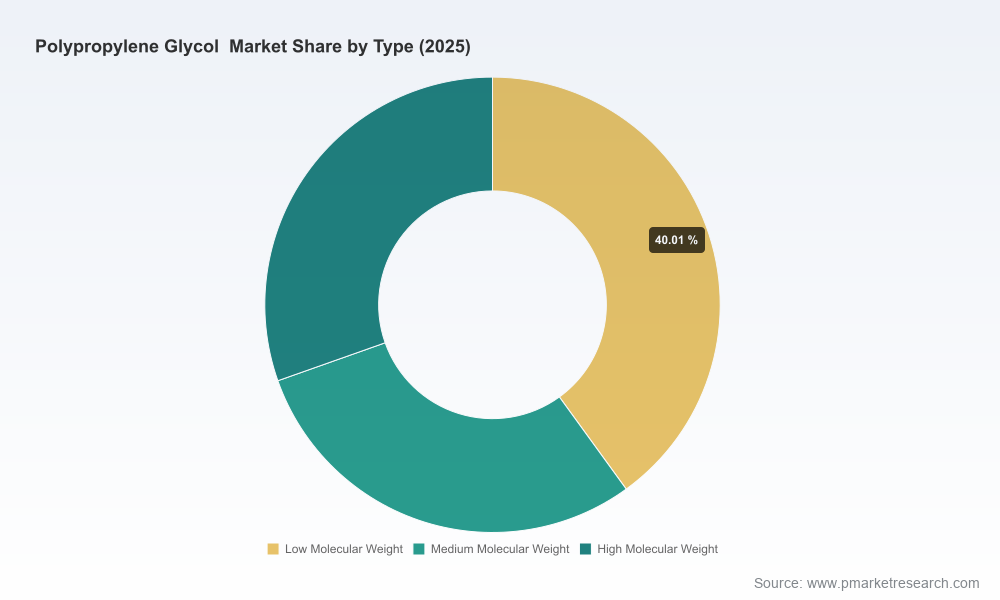

Polypropylene Glycol Market — Strategic Outlook for 2026 Decision-Makers

As companies set budgets, capital plans, and product roadmaps for 2026, the polypropylene glycol (PPG) value chain sits at a crossroads of steady demand growth, tighter sustainability expectations, and episodic supply shocks. PW Consulting’s newest market study frames these dynamics with a granular, decision-oriented lens: the global PPG market — having expanded from roughly USD 3.1 billion in 2020 to about USD 3.9 billion by 2025 (base year) — is forecast to continue its upward trajectory, reaching approximately USD 5.75 billion by 2032 at a compound annual growth rate (CAGR) of 5.8% over the 2026–2032 forecast horizon. For executives preparing 2026 strategies, that projection is not an abstract statistic; it is the backbone for capacity planning, sourcing strategies, product-portfolio prioritization, and M&A screening.

Polypropylene Glycol Market

Why this study matters for 2026 choices

Three practical realities converge in 2026 to make PPG strategic rather than tactical for chemical producers, downstream formulators, and strategic buyers:

Polypropylene Glycol Market

- Sustained growth with differentiated pockets of opportunity. The market’s mid-single-digit CAGR masks variation by end-use and grade. Identifying where premium margins will appear — whether in engineered polyols for high-resilience foams, functional fluids, or formulated personal-care intermediates — is essential before committing capital or signing long-term offtake agreements.

- Regulatory openings and compliance burdens. Recent regulatory movement — including the European Commission’s February 2026 amendment approving certain polypropylene glycol uses in food-contact plastics — creates new addressable markets while raising compliance and traceability requirements across supply chains. Companies that align early to these regulatory vectors can capture first-mover advantage in value-accretive niches.

- Sustainability as a price of entry and a differentiation lever. Mass-balance and bio-based product introductions by major players are shifting buyer expectations. Certification (e.g., ISCC PLUS) and verified supply chains are fast becoming procurement pre-requisites rather than marketing add-ons.

What the report delivers — operational, not academic

We designed this study as a commercial playbook for 2026 rather than a purely descriptive market map. The report synthesizes market-level forecasts and scenario analysis with actionable modules aimed at specific corporate functions:

Polypropylene Glycol Market

- Demand forecasting models (2026–2032) by grade family and end-use cluster, with sensitivity runs for raw-material price shocks and substitution risk.

- Supply-side and capacity-mapping tools that translate plant reliability, certification status, and ramp schedules into expected volumes available to the market under normal and stressed conditions.

- Feedstock and cost-to-serve analytics that quantify the margin impact of ethylene oxide, propylene supply volatility, and energy pricing under multiple scenarios.

- Regulatory compliance checklist and a stepwise roadmap for food-contact approval pathways, mass-balance tracing, and documentation required for ISCC-style certifications.

- An M&A and JV screening matrix that ranks targets by strategic fit, capacity vintage, geographic stretch, and integration complexity — plus a priced model for payback under conservative demand cases.

- Commercial playbooks for buyers and sellers: negotiation levers for long-term supply agreements, clause language for force majeure and allocation, and go-to-market templates for sustainable PPG grades.

- Supplier risk heatmaps and contingency planning templates to manage outages, logistics disruption, and rapid demand surges.

Note: to preserve commercial value and encourage direct engagement, the report presents full regional and application-level breakdowns and company-level volume tables in the paid dataset. The executive narrative here illustrates the strategic implications while intentionally withholding the granular tables and split-data that buyers rely on for operational decisions.

Competitive landscape and what it means for incumbents and challengers

The PPG industry sits between commodity and specialty chemistries: concentration ratios indicate a moderately fragmented market (three‑company share and five‑company share measures place market control well below dominant oligopoly levels). That structure creates room for both scale-driven players and niche specialists. Our assessment of leading players highlights how different strategic postures will play out into 2026 and beyond:

- Dow Inc. — With global manufacturing scale and recent ISCC PLUS-certified outputs, Dow has repositioned parts of its PPG platform to serve sustainability-sensitive customers. Their Thailand certification and mass-balance product introductions indicate a deliberate move to protect premium positions in polyurethane and consumer markets. For 2026, Dow’s playbook will likely emphasize certified product penetration, long-term contracts with OEMs, and selective value-added chemistries integrated into broader polyol systems.

- BASF SE — BASF’s launch of biomass-balance PPG grades shows a parallel strategy among European majors: use of certified pathways to defend margins as buyers demand greener inputs. BASF’s strength in process technology and R&D positions it to commercialize differentiated grades for coatings and functional fluids — areas where formulation nuances command premium pricing.

- Covestro AG and Huntsman Corporation — These firms leverage brand relationships with polyurethane producers and elastomer formulators. Their strategic emphasis in 2026 is expected to center on co-development agreements, service offerings (technical support for foaming and elastomer systems), and geographic optimization of production to serve regional foam ecosystems efficiently.

- LyondellBasell, INEOS Oxide, Shell Chemicals — These players bring feedstock integration and global logistics networks to the table. INEOS’s 2025 Cologne production halt — and resultant force majeure declarations — is a cautionary case study: integrated players reduce some upstream risk but are still exposed to site-level operational failures. Shell and LyondellBasell will likely continue to monetize supply-chain strength while selectively upgrading product portfolios toward specialty and certified variants.

Recent developments that should shape boardroom priorities in 2026

- Certification and mass-balance product introductions by majors are accelerating buyer expectations for traceability and sustainability claims. Procurement teams must update RFP templates to reflect verifiable sustainability criteria.

- BASF’s biomass-balance product launch demonstrates that scale can be brought to green products; smaller suppliers without accredited pathways risk being sidelined in strategic accounts unless they partner or obtain equivalent certifications.

- INEOS Oxide’s 2025 production halt underscores the materiality of single-site outages. Risk management for 2026 should include capacity insurance, multi-sourcing for critical grades, and contractual protections for allocation and make-good clauses.

- The European Commission’s 2026 amendment that expands approved uses (including certain food-contact applications) materially changes addressable markets in Europe. Compliance, labeling, and documentation workloads will increase for any supplier intending to serve food-contact and consumer-packaging end-uses.

- Broader industrial decarbonization projects (e.g., large green hydrogen investments in Germany) signal that access to lower-carbon energy and feedstocks will become an increasingly important factor in site economics and in customer selection criteria by 2028–2030.

Five immediate actions for 2026 planners

- Update demand-sensing and procurement rules: incorporate certified-supply premiums and build scenario-based hedges for feedstock volatility into 2026 procurement budgets.

- Pursue certification where it matters: map your customer base to identify which accounts will pay for ISCC or biomass-balanced product attributes and prioritize certification investments accordingly.

- Stress-test supply chains against single-site failures: require dual-sourcing for critical grades and introduce contractual clauses that protect margin and continuity during force majeure events.

- Accelerate regulatory readiness: for companies targeting food-contact applications, assemble a cross-functional team (regulatory, legal, QA, and commercial) to operationalize the documentation and testing pathways introduced in early 2026.

- Scan M&A selectively: with market concentration still relatively modest, smaller bolt-on acquisitions and JVs can rapidly buy capability (certified production, local distribution, technical-service teams) without the structural premium of a large-scale buyout.

How PW Consulting’s study supports execution

The practical value of our study rests on its executable outputs: calibrated forecast models you can run under your own input assumptions; supplier-impact matrices that translate force-majeure events into product allocation curves; and a prioritized list of commercial actions tied to ROIs under multiple demand scenarios. We deliberately structure the paid dataset to feed into procurement systems and corporate strategy models so that finance teams can run real‑time decision support ahead of 2026 contract renewals.

We intentionally withhold granular regional and application split tables in this executive narrative because those slices are the primary commercial intelligence embedded in the full dataset. If your 2026 decisions depend on which end uses or geographies will deliver premium growth or risk-adjusted returns, the full report contains the primary evidence you need: the grade-by-end-use forecasts, company-level supply overlays, and contract-risk scoring that convert macro projections into boardroom-ready choices.

Conclusion — from insight to 2026 advantage

PPG is not a passive commodity; it is a set of chemistry platforms whose economics and market access are increasingly defined by certification, regulatory standing, and supply resilience. With the market forecast growing from about USD 3.9 billion in 2025 to roughly USD 5.75 billion by 2032 at a 5.8% CAGR, the question for 2026 is not whether demand will exist — it will — but whether your company will be positioned to capture the higher-margin segments and defend supply continuity when shocks occur. PW Consulting’s study is built to translate that market trajectory into clear, accountable actions for procurement, commercial, and corporate strategy teams. For the full segmentation, company-level tables, and the downloadable models that operationalize this intelligence, consult the complete report and dataset.

For detailed analysis of this topic, please visit the official page:Polypropylene Glycol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com