Scopolamine Market 2026: Strategic Preview for Executives — What Every Decision-Maker Needs Before Q2

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive preview of our Scopolamine Market study designed to equip leadership teams with the context and decision frameworks they need for 2026. This briefing synthesizes the structural growth dynamics, competitive posture, regulatory shocks and the practical toolset embedded in the full report — while withholding granular splits and proprietary scoring that are reserved for the full publication.

Scopolamine Market

Market snapshot: scale, trajectory and concentration

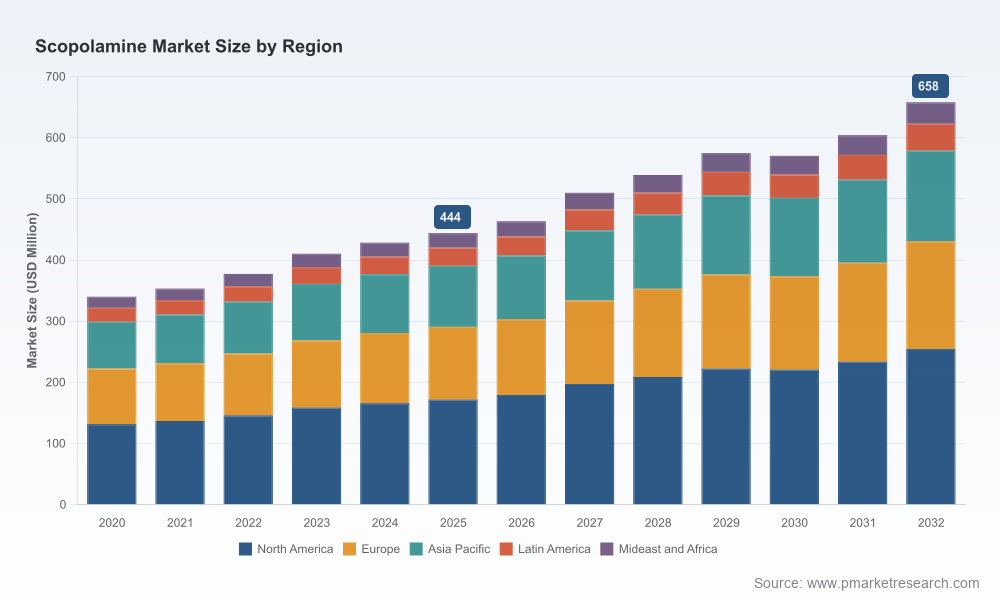

The scopolamine market has moved from a mid‑single‑hundred million USD industry in the early 2020s to a robust, more mature therapeutic-chemical market by 2025. On the basis of our model (base year 2025, historical window 2020–2025 and forecast 2026–2032), the market was approximately USD 444 Million in 2025 and is projected to reach roughly USD 658 Million by 2032 — reflecting a compound annual growth rate (CAGR) of 5.8% through the forecast horizon. The trajectory reflects steady demand in established therapeutic uses, evolving delivery forms, and a mix of supply-side consolidation and episodic shortages that periodically reprice the market.

Scopolamine Market

Market concentration is material but not monopolistic: the top three suppliers account for approximately half of the market, and the top five collectively capture roughly two‑thirds. This structure creates predictable supplier power in certain channels while leaving room for niche entrants and differentiated product strategies.

Scopolamine Market

Why this research matters for 2026 decisions

- Timing: 2026 will be the inflection year for many tactical procurement, regulatory compliance and commercialization decisions. The market’s near-term growth and ongoing structural shifts mean choices made in 2026 will materially affect cost base, supply resilience and competitive positioning into the next regulatory cycle.

- Risk management: Our study consolidates supplier risk, regulatory events and shortage scenarios into a decision-ready risk matrix. Procurement, quality and legal teams can use it to prioritize supplier audits, contingency inventories and compliance checks.

- Go‑to‑market (GTM) and portfolio strategy: For product teams, the report translates demand drivers and delivery‑form trends into a prioritized set of product development and licensing opportunities without the requirement to commit significant R&D spend on low-return permutations.

What the full report contains — actionable, not ornamental

- Validated market model (2020–2032) with scenario outputs and sensitivity analyses for pricing, shortage events and regulatory shocks.

- Supplier & vendor playbooks: scored profiles for active manufacturers and API suppliers, including USDMF/DMF status, regulatory filing footprints, manufacturing locations and known supply capacities.

- Commercial intelligence dashboards: tender intelligence, contract renewal calendars and distributor channel mapping for key markets.

- Operational tools: supplier risk matrices, inventory buffering calculators, and a step‑by‑step supplier qualification checklist tailored to scopolamine APIs and finished‑dose formulations.

- M&A and partnership filters: sector-specific criteria for bolt-on acquisitions, JV candidates and licensing deals, with financial thresholds and integration risks highlighted.

- Regulatory tracker & scenario playbook: a dynamic timeline of recent enforcement actions, product discontinuations and USDMF/Type II DMF statuses, along with recommended mitigation pathways.

Competitive landscape — themes and strategic implications

The competitive structure blends established API producers, regional specialty players and a small number of finished-dose manufacturers that control critical channels such as transdermal systems. Key industry players profiled in the report include—but are not limited to—Alchem International Pvt. Ltd., Transo‑Pharm Handels GmbH, Aspen API, Alkaloids Private Limited, Phytex Australia, Vital Laboratories, Fine Chemicals Corporation, Zhejiang Ausun Pharmaceutical, Teva Pharmaceuticals and Zydus Lifesciences.

- API heavyweights and regulatory footprints: Several API manufacturers maintain active USDMF/DMF statuses and are routinely relied upon by finished-dose producers. Active filings and type classifications are discussed in the report and used to rank supplier suitability for regulated markets.

- Finished-dose competition and form factor control: A handful of manufacturers dominate the transdermal patch segment and hold critical regulatory dossiers for generic transdermal systems. Control of patch supply chains can create downstream ripple effects for hospital and retail channels, especially during brand discontinuations or shortages.

- Regional manufacturing nodes: Production is geographically distributed across Asia, Europe, Australia and select other nodes. This diversification reduces systemic supply risk but introduces variability in regulatory inspection risk and transport logistics.

- Concentration and strategic openings: With the top three players accounting for about half of demand and the top five nearing two‑thirds, there is strategic room for specialized entrants — particularly those that can offer regulatory-ready DMFs, reliable batch release metrics, or differentiated formulation expertise (e.g., alternative delivery systems).

Recent developments and what they signal for 2026

- Antitrust enforcement: A 2025 European Commission enforcement action resulted in fines for one supplier for cartel behavior involving price‑fixing and quota allocation. This event elevates compliance risk in procurement decisions — buyers should now treat historical supply behaviors as a vector of regulatory exposure and factor legal contingency into supplier evaluation and contract terms.

- Formulation and supply shocks: The discontinuation of certain branded transdermal patches has already triggered payer and health-system level substitution decisions (for example, some health plans moved to prefer generic patches in response to distribution delays). Expect episodic demand spikes for alternative suppliers and formulation types when brand products exit or experience supply disruptions.

- Regulatory dossier visibility: Multiple suppliers have active USDMF/Type II DMF statuses for scopolamine entities. Active filings are a leading indicator of who can credibly support rapid regulatory submissions in major markets — an operational advantage that the report highlights and scores for practical procurement use.

Practical strategic moves for 2026

Depending on your role — procurement, commercial, R&D or corporate development — the following actions should be prioritized in 2026:

- Procurement: Implement a tiered sourcing strategy that combines at least two qualified API suppliers with overlapping regulatory filings, and embed penalty/escape clauses specific to anti‑competitive revelations and force‑majeure supply interruptions.

- Commercial: Reassess pricing and contracting strategies for finished-dose products, especially transdermal systems. Scenario‑test payer substitution behavior and prepare rapid relaunch kits for alternative formulations.

- Quality & Regulatory: Map active DMF/USDMF statuses across prospective suppliers and require transparency on inspection histories and corrective action timelines. Prioritize suppliers with Type II or equivalent dossiers for expedited registration support.

- Corporate Development: Use our M&A filters to examine small API manufacturers with clean compliance track‑records as bolt-ons. Look for assets that expand regulatory reach (DMFs) or add capacity in under‑institutionalized regions.

How to use the full PW Consulting report in your 90‑day plan

- Week 1–2: Run the supplier risk heatmap against your current spend and identify single‑source exposures.

- Week 3–6: Initiate conditional supplier qualification for top alternate providers and negotiate contingent supply contracts tied to confirmed DMF status.

- Week 7–12: Deploy the commercial playbook to update GTM scenarios, adjust pricing ladders and brief payers on continuity plans in case of product discontinuations or enforcement events.

Closing: what this preview does — and does not — provide

This preview establishes the strategic contours of the scopolamine market going into 2026: a growing market (CAGR ~5.8%), measurable concentration among a few suppliers, and heightened regulatory and supply fragility driven by enforcement and product discontinuations. The full PW Consulting Scopolamine Market report contains the proprietary segmentation, vendor scores, financial modeling and region/application-level intelligence that will convert this strategic overview into executable tactics. For procurement checklists, supplier scorecards, and the complete modeled scenarios used to produce our growth trajectories, please consult the source report.

PW Consulting’s research is designed to be directly deployable: it tells you where to act first, what to measure, and which suppliers to engage — without exposing the confidential granular tables that drive competitive advantage. If your 2026 planning cycle includes supply decisions, regulatory filings or M&A activity tied to scopolamine, this study should be your primary reference document.

For detailed analysis of this topic, please visit the official page:Scopolamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com