Food Gelatin Market: Strategic Preview for 2026 Decision-Making

PW Consulting’s Food Gelatin Market study (base year 2025, historical window 2020–2025, forecast 2026–2032) maps a market in transition — expanding, structurally shifting, and navigating regulatory pressure. This preview outlines why the research is an essential input for executive teams, corporate development groups, and procurement leaders preparing 2026 strategies. We reveal the analytical posture and the types of actionable outputs included in the full report while deliberately holding back granular subsegment data that are accessible only in the source report.

Food Gelatin Market

Market snapshot: measured growth, clear trajectory

The global food gelatin market has demonstrated steady expansion through the historical window, rising from USD 163.15 Million in 2020 to USD 215.0 Million in 2025 (base year). Our forecast work projects a continued upward trajectory to an estimated USD 344.8 Million by 2032, underpinned by a 6.98% compound annual growth rate over the 2026–2032 forecast period. Those headline metrics encapsulate a category benefitting from steady demand in core food applications, growing interest in value-added collagen derivatives, and periodic supply-side dislocations that influence pricing and sourcing strategies.

Food Gelatin Market

Why this matters for 2026 corporate strategy

- Budgeting and investment sizing: With a mid-single-digit-to-high-single-digit CAGR, the category is attractive for targeted capex and M&A, but requires precision: different strategic moves (capacity expansion, specialty product development, captive sourcing) carry materially different returns that we model in the full report.

- Supply-security and procurement: Recent raw-material dynamics mean procurement must shift from tactical spot-buying to a portfolio approach (index-linked contracts, multi-sourcing, forward purchase agreements) to protect margins and continuity of supply.

- Regulatory and product-compliance risk: Evolving EU rules and emerging contaminant limits introduce compliance complexity that is operationally material for exporters and formulators selling into regulated markets.

What the PW Consulting report delivers (operationally oriented)

- Proprietary market model — top-line sizing by year (historical and forecast), with transparency on drivers and scenario alternatives. We provide base, upside, and downside cases to stress-test capital allocation and product launch decisions.

- Value-chain analysis — from raw hides/skins sourcing through rendering, hydrolysis and refinement, to concentration points and logistics constraints. The model identifies where margin pools sit and which nodes are most exposed to disruption.

- Regulatory impact assessment — granular mapping of recent regulatory changes and plausible near-term amendments, together with operational checklists to maintain market access and label-compliance in major jurisdictions.

- Supplier and capabilities matrix — a qualitative and quantitative assessment of global manufacturers, differentiating commodity producers from specialty and peptide-focused players, with supplier scorecards for quality, flexibility, traceability and sustainability.

- Risk-adjusted M&A and investment playbooks — valuation frameworks, integration checklists, and synergies stress-tests calibrated for a market with low-to-moderate concentration and diverse regional dynamics.

- Commercial strategies — commercial segmentation, pricing playbooks, and product innovation pathways (e.g., functional peptides, low-sugar gelatin systems) designed to accelerate margin capture for food manufacturers and ingredient suppliers.

- Execution roadmaps — 90–180 day tactical checklists and 1–3 year strategic milestones tailored to three archetypal buyers: multinational food processors, regional ingredient producers, and private-equity backed consolidators.

Near-term market dynamics and catalysts

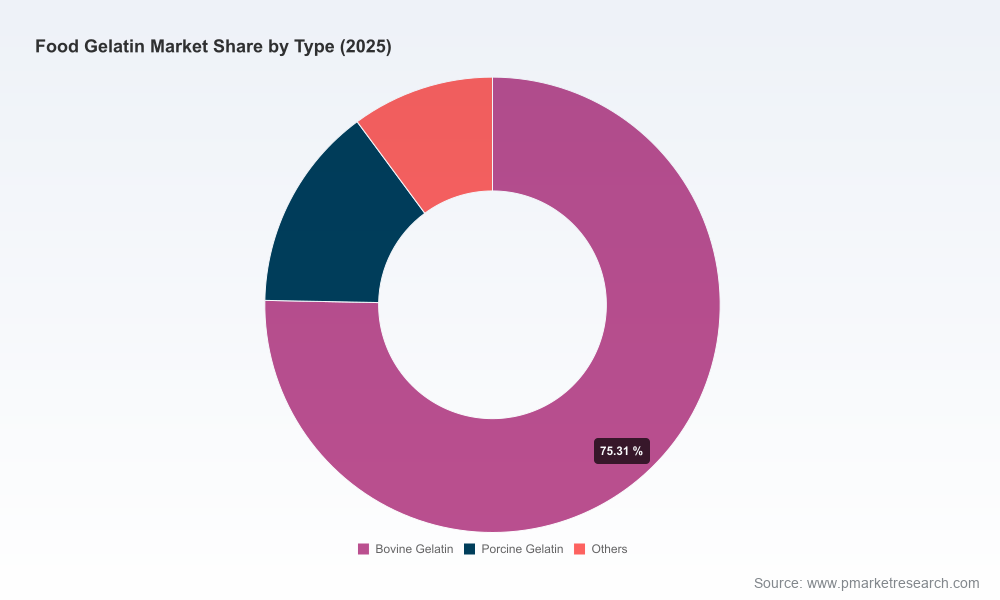

- Raw-material realignment: Industry data indicate bovine hides account for approximately 52% of raw-material sourcing for food gelatin production. Disease outbreaks (notably African Swine Fever) have constrained pork-skin availability in some regions, accelerating substitution toward bovine-derived inputs and creating short-term pricing pressure for buyers dependent on porcine supply.

- Regulatory adjustments: The EU’s Delegated Regulation 2025/637 and subsequent regulatory activity addressing contaminants have introduced tighter compliance requirements for certain gelatin-containing formats. These rule changes raise the cost of market entry for smaller exporters and increase testing and traceability costs for formulators selling into the EU.

- Greenfield capacity and regional supply shifts: Announcements of new manufacturing capacity — for example, a sizeable edible-gelatin plant planned in Central Asia with multi-thousand-ton annual output that commences in the near term — will re-shape regional sourcing corridors and price dynamics where they come online.

- End-market product dynamics: Consumer trends toward cleaner labels and reduced sugar formulations have encouraged product reformulations and pre-made gelatin snack introductions, underscoring opportunities for ingredient innovation and co-development with large food brands.

Competitive landscape — positioning and strategic moves

The food gelatin space combines legacy, regionally-rooted producers and focused specialty players. Market concentration metrics point to a fragmented structure: the top-three and top-five players together represent a minority share of global revenues, indicating room for consolidation, regional differentiation, and niche specialization.

Food Gelatin Market

- Major global producers (examples): A set of established global companies serve broad food and nutraceutical markets, offering commodity gelatin, collagen peptides and technologically advanced texturants. These firms generally compete on scale, global supply networks, and an expanding portfolio of value-added ingredients.

- Specialists and regional champions: Firms focused on texture systems, bakery and confectionery applications, or regional supply chains differentiate through formulation support, co-development agreements, and targeted marketing to food OEMs and HoReCa channels.

- Upstream and emerging producers: New capacity announcements and entrants in cost-advantaged regions are reshaping supplier economics. For buyers, the proliferation of suppliers creates opportunity to re-negotiate terms but also increases due-diligence needs around quality and traceability.

- Recent corporate activity: Product launches and trade-show engagements from ingredient specialists, along with notable product updates from consumer-food majors, demonstrate active co-innovation and ongoing product refresh cycles that ingredient suppliers can leverage.

Strategic implications for executives in 2026

- Supply resilience is now a strategic priority: Move from single-sourced or spot-dependent procurement to layered contracts that combine flexibility with guaranteed volumes. Build inventory hedges only where financially justified by price volatility and lead-time risk modeling.

- Invest in traceability and compliance: Prioritize investments in upstream traceability (raw-material verification, chain-of-custody) and in-lab analytics to satisfy stricter regulatory regimes and to secure buyer contracts in regulated markets.

- Product and route-to-market innovation: Target two lanes — (1) premium functional ingredients (peptides, enriched gelatin systems) where margin expansion is feasible; (2) cost-competitive commodity supply with improved sustainability claims for large-volume buyers.

- Watch consolidation windows: Fragmentation and modest concentration suggest a favorable environment for roll-up strategies to capture scale benefits in logistics and procurement. Private-equity players should focus on technical capabilities and access to strategic customers as acquisition criteria.

- Scenario-plan for regulatory shocks: Build a regulatory war-room to test product portfolios against plausible tightening of contaminant limits and to define rapid reformulation paths to protect shelf-space and export routes.

Recommended 90–180 day playbook (practical steps)

- Run a supply-mix stress test: Model your supply alternatives under pork-skin constrained and bovine-surge scenarios; quantify margin and service impacts across product lines.

- Initiate strategic supplier dialogues: Open medium-term agreements with at least two suppliers in distinct sourcing regions and secure clauses for quality audits and traceability data-sharing.

- Launch regulatory readiness audit: Review existing products for compliance with the latest EU measures and emerging contaminant thresholds; prioritize reformulations where exposure is highest.

- Pilot a co-innovation program: Partner with a specialty gelatin supplier to develop a reformulated, reduced-sugar gel application to capture growing convenience-snack demand.

Longer-term options (1–3 years)

- Vertical integration: Evaluate captive rendering or pre-treatment assets in regions where raw-material access is strategic and cost-advantageous.

- Capability-led acquisitions: Target acquisitions that add peptide capabilities, clean-label formulations, or regional capacity to secure cross-border supply chains.

- Product diversification: Expand into adjacent functional ingredient categories (e.g., collagen specialties, texturants) to smooth cyclicality tied to single-use applications.

Concluding guidance

For 2026, the food gelatin category offers a mix of steady demand growth (reflected in the 2026–2032 forecast and the 6.98% CAGR) and actionable disruption driven by raw-material dynamics, regulatory tightening, and continued product innovation. PW Consulting’s full report provides the quantitative underpinnings, scenario models, supplier scorecards, and execution playbooks needed to convert these high-level insights into operational decisions. This preview is intended to orient executives to the strategic stakes and to the practical levers available — the report contains the proprietary subsegment and tactical data you’ll need to finalize 2026 allocations and M&A targets.

Contact PW Consulting to access the comprehensive dataset, detailed subsegment analysis, and client-tailored advisory support that will enable decisive action in 2026.

For detailed analysis of this topic, please visit the official page:Food Gelatin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com