Pyrethrin (CAS 8003-34-7) Market — Strategic Preview for 2026 Decision-Makers

PW Consulting presents a strategic introduction to our full Pyrethrin (CAS 8003-34-7) Market study. This briefing distills the research’s most consequential insights for corporate leaders planning actions in 2026 — from procurement and product strategy to M&A, regulatory engagement, and sustainability investments. It is deliberately structured as a “trailer”: we demonstrate forensic market understanding and actionable lines of inquiry while withholding granular sub-segment tables and proprietary price decks, which are available in the complete report.

Pyrethrin (CAS 8003-34-7) Market

Why Pyrethrins Matter Now

Pyrethrins occupy a distinctive position at the intersection of rising global demand for natural insect control and material supply fragility. The category has exhibited steady expansion: the global market grew from roughly USD 52.0 Million in 2020 to approximately USD 71.2 Million in our base year (2025), and our modelling forecasts a continuation of that growth into the next decade. Under the report’s central scenario the market expands at a compound annual growth rate (CAGR) of 6.18% over the 2026–2032 forecast window, reaching an estimated USD 110.7 Million by 2032. These topline dynamics validate pyrethrins as an investible specialty ingredient for active ingredient houses, formulators of biological pest control products, and strategic buyers focused on premium natural chemistries.

Pyrethrin (CAS 8003-34-7) Market

Structural Drivers and Supply Dynamics

- Demand pull and product differentiation: Adoption across household pest control, public health interventions, select agricultural applications, and animal health segments is being driven by consumer preference for natural or near-natural actives and regulatory pressure on certain synthetic classes. This creates pricing insulation for pyrethrins relative to many commodities, but also places a premium on verified quality and traceability.

- Raw material concentration and operational exposure: The feedstock for commercial pyrethrin is overwhelmingly cultivated in a narrow geographic band of high-altitude East African regions where hand-harvested pyrethrum flowers are produced by smallholders. That concentration amplifies supply-side volatility: weather seasonality, farm-level productivity variance, local regulation, and political stability in sourcing countries can translate quickly into global supply tightness.

- Cost structure and competitive positioning: Labor intensity and low per-hectare yields mean natural pyrethrin raw material costs are multiple times higher than many synthetic alternatives. That cost delta sustains attractive per-kilogram pricing but forces manufacturers and formulators to optimize yield, extraction efficiency, and premium positioning in end-markets.

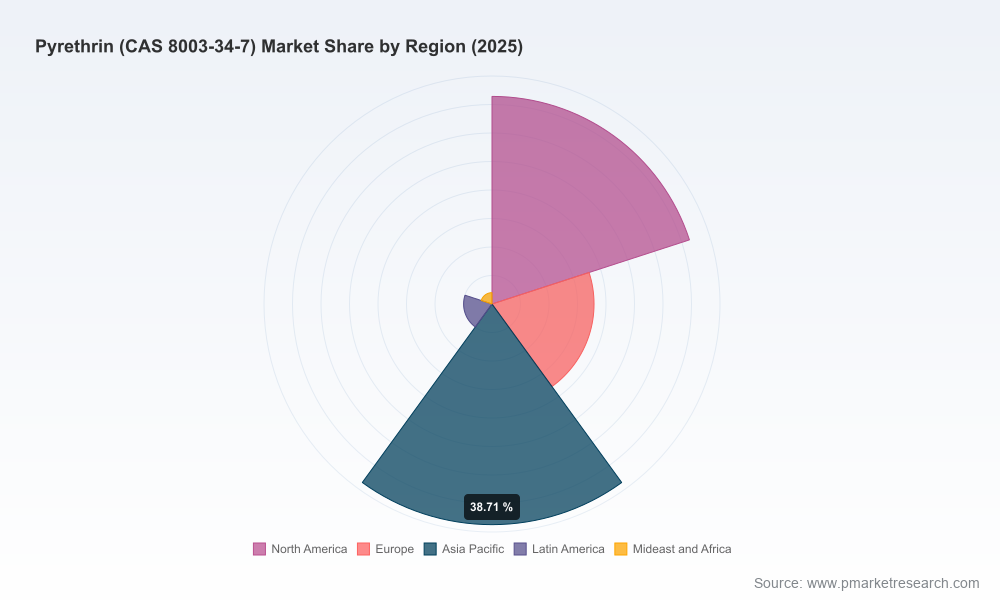

- Concentration of finished supply: The market is moderately concentrated at the supplier level — our analysis flags a top-three concentration around the high forties percentage and a top-five concentration modestly above the mid‑fifties. This structure creates both entry barriers for newcomers and targeted M&A opportunities for players seeking to secure raw material throughput or downstream formulation capabilities.

Regulatory and Institutional Context

- Regulatory reform in key producing countries is reshaping the operating environment for raw material aggregation, processing and exports. New draft regulations and legislation aim to rationalize producer licensing, traceability and quality standards — a double-edged driver that improves product integrity for global buyers while imposing compliance costs and transition risks on local processors.

- On the demand side, evolving public health priorities and pesticide stewardship frameworks in multiple jurisdictions increase the likelihood of selective procurement policies that favor certified natural actives, reinforcing long-term market support.

Competitive Landscape — Who to Watch

Our proprietary company profiling focuses on producers and processors that collectively define capacity, quality leadership, and market channels. Representative players include:

Pyrethrin (CAS 8003-34-7) Market

- KAPI Limited (Kenya) — The world’s largest single pyrethrum extract producer by throughput, operating solvent extraction facilities and a substantial smallholder contracting footprint in Kenya’s Rift Valley. Recent trade show participation underscores its active global commercial outreach and farmer aggregation model.

- Botanical Resources Australia Pty Ltd (Tasmania) — A major global supplier noted for high-purity extracts produced at scale in Tasmania. Industry recognition in 2025 reaffirms its importance as a counterweight to East African supply and a key node for quality-focused buyers.

- Horizon Sopyrwa (Rwanda) — An East African exporter supplying high-quality natural insecticide extract with strategic proximity to core growing regions and a growing role in continental supply chains.

- Pyrethrum Processing Company of Kenya (PPCK) — An aggregator and value‑adder that supports farmers, produces semi‑refined extract and is a focal point for national industry revival initiatives that have recently received renewed government support.

- Kentegra Biotechnology (Naivasha, Kenya) — Positions itself on the pharmaceutical-grade end of the spectrum, supplying pyrethrins that meet stringent quality requirements for treated nets, indoor residual sprays and other WHO-oriented applications.

Recent industry events — from trade exhibitions to government-backed revival programs and draft regulatory frameworks — illustrate two things: (1) major suppliers are actively upgrading commercial and quality assurance capabilities, and (2) national policies in producer countries are moving toward more formalized, licensed and traceable supply chains. Both trends have direct implications for sourcing, contract design and supplier due diligence in 2026.

What the Full Report Contains (Practical, Operative, and Ready-to-Use)

- Topline market sizing and outlook (2020–2032) with scenario‑based forecasts and sensitivity to supply shocks and regulatory regimes.

- Commercial intelligence: supplier scorecards, capacity maps, and an indexed risk register for upstream aggregation points.

- Price and cost models: global price desk, landed cost calculators by region, and breakpoint analyses for formulation economics.

- Regulatory matrix: country-by-country compliance checklist, likely timelines for regulatory change, and implications for product registration.

- Supply‑chain playbook: contracting templates for forward-buying, recommended KPI dashboards for quality and traceability, and practical mitigants for seasonality and harvest risk.

- Strategic options and M&A playbook: target screening criteria, synergies estimates, and a phased integration roadmap tailored to asset types (processing, contract farming, downstream formulation).

- Scenario planning and stress tests: quantified outcomes for supply disruption, synthetic displacement, and price collapse, plus recommended hedging and diversification responses.

Note: the full report includes granular regional and application splits, granular pricing by product form and purity, supplier-level contract templates and proprietary financial models. These proprietary components are intentionally omitted from this preview to protect commercial value.

Actionable Strategic Priorities for 2026

- Secure supply without overpaying: Use a layered procurement approach — strategic forward commitments with quality-linked pricing, combined with small spot allocations to capture upside when markets ease. Prioritize suppliers that can demonstrate upstream traceability and stable farmer networks.

- De-risk through diversification: Balance East African sourcing exposure by developing alternative channels with Oceania processors and by exploring toll‑processing partnerships that shift logistics and currency risks.

- Invest in value capture: Consider partial vertical integration — from aggregation investments to minority stakes in extraction assets — to improve margin capture and control over quality specifications essential for premium end-markets.

- Regulatory readiness: Build a compliance playbook aligned to forthcoming producer-country regulations and global public-health procurement standards. Certification and documented traceability will be tangible commercial differentiators.

- Product & market differentiation: Layer pyrethrin-based offerings with enhanced stewardship guarantees (e.g., chain-of-custody, residue testing) and focus on end-markets willing to pay premiums for certified natural actives.

- M&A and partnership screen: Target companies that either broaden geographic sourcing, add downstream formulation capability, or provide certified access to public-health procurement channels. Moderate supplier concentration at the top creates tactical exit and consolidation opportunities.

Risk Radar — What Keeps CFOs Awake

- Supply shock from crop failure, political disruption or abrupt policy change in key producing countries.

- Price volatility driven by mismatch between high-cost natural feedstock and cyclical demand in agriculture and household segments.

- Regulatory non-compliance risk as national frameworks in producer countries are formalized, increasing the stakes of supplier selection.

- Technical substitution risk in lower-margin use cases if cheaper synthetics regain regulatory favor or see innovation-led performance gains.

Closing — The Strategic Imperative for 2026

For executive teams evaluating resource allocation in 2026, pyrethrins represent a niche with asymmetric opportunity: the market is large enough to be strategically meaningful and growing at a mid‑single-digit CAGR, yet concentrated and supply-sensitive enough that correctly timed investments in sourcing, quality assurance and targeted consolidation can yield outsized returns. The tactical window for securing advantaged positions — through offtake, equity stakes in processors, or preferential supply agreements — is open now and is likely to narrow if regulatory formalization or a supply disruption materializes.

To operationalize these insights in your context — including access to supplier-level scorecards, full regional/application splits, price decks, financial proxies and contract templates — consult the PW Consulting Pyrethrin (CAS 8003-34-7) Market full report. It contains the actionable detail required to convert strategic intent into 2026-ready programs.

For detailed analysis of this topic, please visit the official page:Pyrethrin (CAS 8003-34-7) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com