WiFi Wireless Speakers Market: Strategic Briefing for 2026 Decision‑Makers

As PW Consulting’s Senior Strategic Advisor and Head of Industry Analysis, I present a concise but high‑impact briefing designed to orient corporate leadership and transaction teams entering 2026. This piece distills the macro trajectory, competitive shifts, and supply‑chain stressors shaping the global WiFi wireless speakers market — enough to inform an executive conversation today, and intentionally curated to steer readers to our full study for the granular segmentation and deal‑level intelligence required to execute decisions.

WiFi Wireless Speakers Market

Market snapshot — where the market stands and where it’s headed

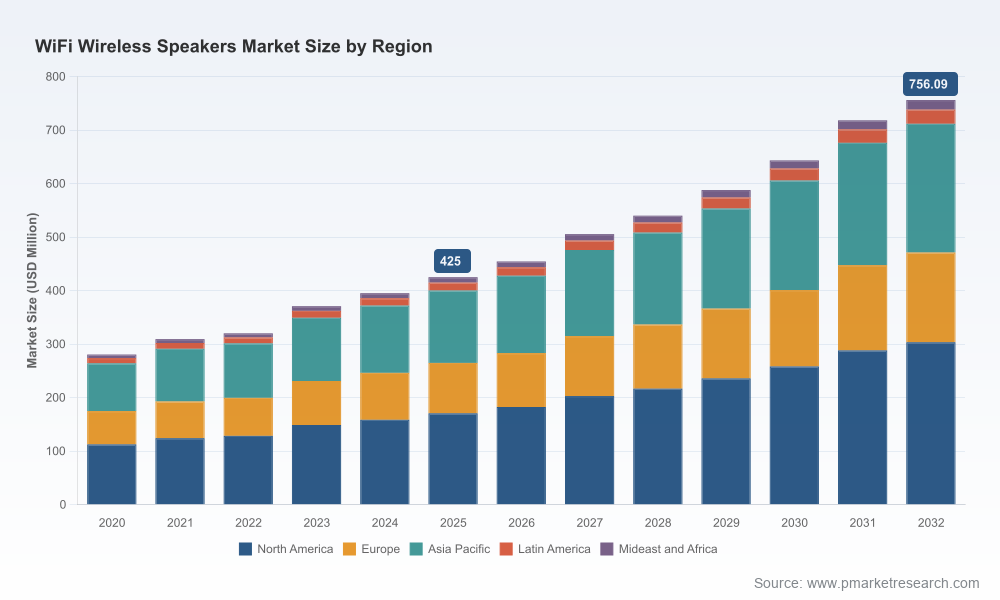

Using 2025 as the report’s base year (historical window 2020–2025, forecast period 2026–2032), our top‑line estimate shows the global WiFi wireless speakers market maturing through an expansion phase driven by streaming adoption, smart‑home integration, and product upgrades across consumer and commercial channels. The market reached USD 425.0 Million in 2025 and is projected to continue its expansion into the forecast window. Over the 2026–2032 horizon the market is expected to grow at a compound annual growth rate (CAGR) of 8.5%, reflecting sustained demand for multi‑room solutions, voice assistant integration, and higher‑fidelity connected speakers.

WiFi Wireless Speakers Market

These aggregate dynamics mask important inflection points: 2024–2026 has been a period of product refreshes and competitive repositioning, while 2027–2030 looks set to amplify ecosystem plays (software + services) and premiumization pressures. Our modelling accounts for macro‑economic scenarios and supply‑chain constraints; the result is a robust, probabilistic view of market size and growth that informs capital allocation, product roadmaps, and M&A timing.

WiFi Wireless Speakers Market

Key dynamics and near‑term risks executives cannot ignore

- Component scarcity and design shifts: The Class‑D amplifier IC shortage that peaked in 2024 pushed audio‑grade chip lead times beyond 60 weeks, forcing many original design manufacturers (ODMs) to redesign speaker boards and delaying mid‑tier product launches. That structural shortage materially alters unit economics and time‑to‑market assumptions for 2026 product programs.

- Raw materials and regulatory volatility: Export controls introduced in 2025 concerning certain rare earth elements created sharp price dislocations and sourcing uncertainty for magnet and motor components. Although those controls were suspended following diplomatic engagement, the episode elevated counterparty and geopolitical risk premia for upstream procurement.

- Platform convergence and software economics: Voice assistants, smart‑home hubs, and media platform integrations are becoming primary basis of competition. Hardware is increasingly a conduit for recurring services (voice commerce, music subscriptions, spatial audio experiences), shifting the value pool from device margin toward ecosystem monetization.

- Channel and consumer segmentation pressure: The confluence of premium audio seekers and mass‑market streamers splits product strategies: one trajectory emphasizes audio engineering and multi‑room fidelity; the other prioritizes affordability, portability, and AI features. Decision frameworks that ignore either vector risk misallocating R&D and go‑to‑market spend.

Competitive landscape — leaders, challengers, and tactical implications

The market exhibits moderate concentration: the report’s competitive overlay indicates a combined revenue share for the top three players that signals a meaningful incumbency advantage, while the top five capture an even larger portion of the market. For strategy teams, this structure implies differentiated routes to scale depending on whether the objective is category leadership, niche specialty, or value disruption.

- Amazon (Echo family) — Amazon leverages platform scale and its voice assistant to drive attachment and recurring behavioral engagement. Recent product iterations continue to emphasize spatial audio and enhanced WiFi connectivity. Strategic implications: competing on software experience and commerce integration is table stakes when facing a platform‑owner with direct retail control.

- Google (Nest / Google Home) — Google’s focus on virtual 360° audio and system integration with Google TV represents a cross‑media play that strengthens its living‑room foothold. Product announcements expected in 2026 emphasize immersive audio as a differentiator, useful for partners pursuing content and platform bundling.

- Apple (HomePod) — Apple’s HomePod strategy remains centered on premium hardware, tightly controlled ecosystem integration, and privacy‑oriented software experiences. For rivals, Apple’s playbook highlights the importance of superior industrial design and services monetization for protecting higher ASPs.

- Sonos — Sonos’s multi‑room proprietary network and recent product refreshes reassert its position in the premium, multi‑room segment. Sonos’s approach demonstrates how independent audio brands can defend margins through differentiated system architecture and brand credibility.

- Bose, Samsung (Harman), Sony — These incumbents each bring a mix of acoustic engineering, channel breadth, and OEM scale. Their strategic focus varies: Bose emphasizes premium acoustics, Samsung leverages Harman for product breadth and integration into broader AV ecosystems, and Sony plays to brand heritage and cross‑category synergies.

Recent product moves — including Amazon’s Echo Studio refresh (early 2026), Google’s announcement of a Google Home Speaker with 360° audio and TV integration (Spring 2026), and Sonos’s Era 100 launch — underscore a near‑term battleground: differentiation through audio performance married with deeper platform features. Our competitive benchmarking in the full report maps the tactical implications of these launches against go‑to‑market channels and margin pools.

What our report delivers — practical, transaction‑grade intelligence

The PW Consulting market study is built for executives who must act. It contains:

- Proprietary market sizing and forecast (historical 2020–2025; forecast 2026–2032) with scenario bands tied to supply‑chain and macro assumptions.

- Segmentation by region, type, and application with validated demand drivers and elasticities. (Note: this briefing intentionally omits the granular segment tables — these are available in the full report.)

- Competitive landscaping and product benchmarking for major OEMs, including go‑to‑market strategies, price architectures, and margin decompositions.

- Supply‑chain risk matrix and mitigation playbook addressing critical components (amplifiers, magnets, DSPs), alternative sourcing strategies, and inventory optimization models.

- Technology roadmap and IP heatmap covering voice assistants, spatial audio, proprietary wireless stacks, and low‑latency streaming standards.

- M&A screen and valuation companion piece identifying targets across categories (scale players, niche premium firms, ODM carve‑outs) with synergy modeling and integration checklists.

- Commercial playbooks: channel prioritization, partner scorecards, pricing experiments, and subscription monetization blueprints.

Each deliverable pairs quantitative models with slide‑ready, action‑oriented recommendations so leadership teams can move from insight to execution within 60–90 days.

Strategic imperatives for 2026

- Lock critical components early: Given persistent lead‑time risk for audio‑grade parts, firms should prioritize flexible supply agreements, dual‑sourcing, and near‑shoring for selected subsystems.

- Shift from device to ecosystem economics: Hardware must be evaluated as a service enabler. Investment in software, cloud features, and platform partnerships will increasingly determine lifetime value.

- Differentiate on experience, not just specs: Spatial audio, seamless multi‑room UX, and tight TV integration are emerging as primary purchase drivers for higher ASP segments.

- Reconfigure channel and promotional spend: Retail, direct, and bundled content partnerships each require different economics. Optimizing promotional intensity across channels can protect margins in a competitive landscape.

- Prioritize modular design: Reducing single‑vendor dependencies via modular architectures lowers the cost of iterative upgrades and compresses redesign cycles when components are constrained.

- Prepare for regulatory supply shocks: Scenario planning — including stress tests for rare earth and upstream material constraints — should be embedded into capital and procurement planning.

Concluding perspective

2026 represents a consequential moment for participants in the WiFi wireless speakers market: the interplay of platform competition, supply‑chain realignment, and product premiumization will define winners and laggards. Our study is expressly designed to help boards, corporate strategy teams, and PE managers convert market signal into defensible, time‑sensitive actions.

For teams preparing strategic plans, product roadmaps, or M&A diligence, the full PW Consulting report provides the segmented forecasts, company scorecards, and granular scenario outputs necessary to underwrite decisions. This briefing demonstrates the analytical spine; the full report contains the datasets, worksheets, and playbooks you will use to operationalize strategy.

For detailed analysis of this topic, please visit the official page:WiFi Wireless Speakers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com