Glyoxal Market 2026 Strategic Outlook — PW Consulting Industry Primer

As companies refine their strategic roadmaps for 2026, glyoxal occupies an understated but high-leverage position across multiple industrial value chains — from textile finishing and resins to select pharmaceutical uses. This primer presents PW Consulting’s distilled perspective on how macro dynamics, feedstock volatility, regulatory shifts, and competitive positioning will shape opportunity windows and downside risks through the 2026–2032 forecast horizon. The full Glyoxal Market report (base year 2025) contains the granular segmentation, scenario matrices, and model-by-model financial implications; this article highlights the strategic intelligence executives need to prioritize decisions in 2026 while preserving the proprietary detail that drives actionable advantage.

Glyoxal Market

Market trajectory at a glance

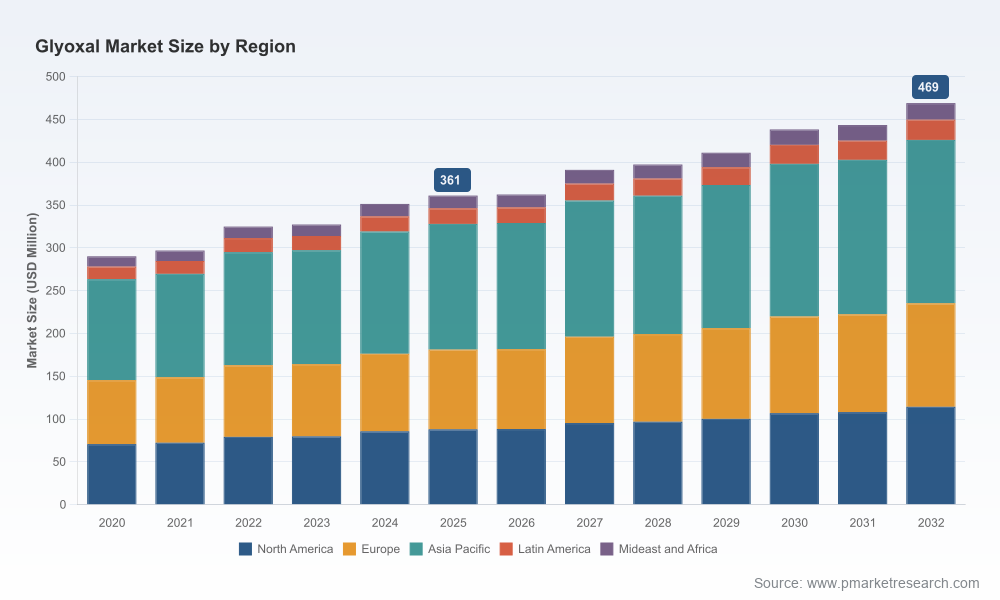

Between 2020 and 2025 the global glyoxal market exhibited steady expansion; using 2025 as the base year, our top-line demand model projects a compound annual growth rate (CAGR) of approximately 3.87% across the 2026–2032 forecast window. The trajectory reflects a blend of steady industrial demand, pockets of substitution and reformulation in sensitive end-markets, and intermittent feedstock-driven pricing cycles. For executives planning capital allocation in 2026, the forecast signals moderate but reliable volume growth — enough to justify targeted capacity investments and optimisation programs, but insufficient to support large-scale speculative builds without clear offtake guarantees.

Glyoxal Market

Why this matters for 2026 decision-making

- Capital projects: With sub-4% CAGR, timing of expansion should be tightly linked to cost curves and offtake security. Brownfield debottlenecks and focused upgrades to deliver specialty grades typically offer better return profiles than greenfield megaprojects.

- Procurement and feedstock risk: Feedstock volatility, particularly for formaldehyde and upstream methanol, materially affects margins. Buyers and manufacturers must reframe 2026 procurement strategies toward flexible sourcing and hedging mechanisms.

- Regulatory risk-management: Emerging occupational exposure reassessments and consumer-product restrictions will force product stewardship investments and selective portfolio pivots.

- M&A and partnerships: Given a medium-concentration market structure, M&A can move the needle for scale and access to specialty grades — but deals must be evaluated against regulatory and feedstock exposures.

Supply chain and feedstock dynamics — the immediate levers

Glyoxal’s economics are tightly coupled to formaldehyde and methanol markets. Recent regional price movements illustrate the immediacy of this linkage: Northeast Asian formaldehyde experienced upward pressure tied to methanol costs in late 2025, while European formaldehyde prices registered mild increases in early 2026 amid resin and wood-panel demand. In contrast, Indian formaldehyde saw a short-term correction in early 2026 followed by renewed volatility. These patterns emphasize two imperatives for 2026:

Glyoxal Market

- Operational flexibility — secure multiple feedstock pathways and consider contracts with staggered indexation clauses rather than single-source, fixed-price suppliers.

- Margin engineering — invest in formulation and process innovations that reduce equivalent formaldehyde intensity or enable blended inputs without compromising product performance.

Regulatory shifts: a strategic risk and a product design opportunity

Regulatory attention has sharpened. European authorities are revisiting workplace exposure thresholds for dialdehydes, prompted by health reviews that call for closer scrutiny of glycation-related effects. Meanwhile, state-level actions in the United States (notably California’s planned restrictions on some formaldehyde-releasing substances effective 2027, and parallel measures in other states) are creating market fragmentation for consumer-facing applications. For 2026 planning, this translates into three concrete actions:

- Prioritise compliance-forward product development for formulations targeting consumer markets — anticipate tighter limits and design substitutes or low-release solutions now.

- Accelerate exposure monitoring and worker-safety programs at manufacturing sites to prevent retrofits and production interruptions.

- Use regulatory foresight as a commercial differentiation — early compliant variants can command pricing premiums where they reduce buyers’ downstream risk.

Competitive landscape — positioning and playbooks

The glyoxal market is neither atomistic nor tightly oligopolistic: leading groups collectively occupy a meaningful share of supply but there remains room for specialist players and regional champions. Market concentration metrics indicate that the top three players account for a sizeable portion of industry volumes, while the top five further consolidate the midstream. This structure favors strategic moves that combine technical capability with route-to-market strength.

Key company archetypes and strategic implications:

- Integrated global giants (e.g., BASF SE, Dow, Eastman): These firms combine world-scale production, deep application know-how, and integrated supply chains. Their playbook is to protect margin through downstream integration, leverage cross-selling into resin and polymer value chains, and invest selectively in specialty derivatives. For competitors, this raises the bar on scale and cross-portfolio synergies; for buyers, it often means more stable supply but less price flexibility.

- Specialist producers and distributors (e.g., WeylChem, Silver Fern Chemical): These players focus on reliable supply of industrial and pharmaceutical grades, paired with global distribution. They are attractive partners for firms seeking supply security without the price premiums of fully integrated suppliers.

- Regional champions and niche manufacturers (notable producers from China, India, Taiwan): These firms often compete on cost-competitive offers for textile, leather, and resin applications. They are agile and can be preferred partners for high-volume, cost-sensitive consumers — but buyers must stress-test supply continuity, quality controls, and regulatory compliance.

- Specialty and high-purity suppliers (e.g., Otto Chemie): High-purity glyoxal for laboratory and pharmaceutical uses remains a defensible niche with higher margins and stronger barriers from quality and regulatory compliance.

For 2026, an optimal commercial strategy is layered: secure a primary offtake with an integrated producer for core volumes, maintain secondary relationships with regional suppliers for flexibility, and source specialty grades from certified niche providers for regulated applications.

Report contents — what PW Consulting delivers

Our full Glyoxal Market study goes beyond headline forecasts to provide the operational playbook that executives need in 2026:

- Robust demand models (historical 2020–2025 base and granular forecasts to 2032) with sensitivity analyses across three macro scenarios;

- Comprehensive supply mapping and capacity overlays, including plant-level vintage, technology intensity, and restart/debottleneck economics;

- Detailed feedstock cost models and break-even analyses that link formaldehyde and methanol price trajectories to producer gross margins;

- Regulatory impact assessments and product stewardship requirements by market (including actionable timelines for compliance-driven reformulation);

- Commercial intelligence on supplier capabilities and partnership-type matrices to evaluate JV, tolling, and long-term supply agreement options;

- Playbooks for procurement, pricing, and product portfolio optimization with sample contract clauses and hedging approaches;

- Investment appraisal templates and M&A scorecards to prioritise targets under different market scenarios.

Practical recommendations for 2026 planning

- Tie investment decisions to secured demand: Prioritise brownfield capacity and specialty-grade upgrades that can be monetised quickly rather than speculative greenfield projects.

- Hedge intelligently: Replace single-factor indexation with hybrid pricing mechanisms that incorporate upstream indices and fixed floors/ceilings to dampen volatility impacts.

- Stress-test product portfolios: Identify SKUs at highest regulatory risk and develop compliant formulations or alternative chemistries that can be commercialised ahead of regulatory deadlines.

- Layer sourcing strategies: Combine capacity-linked contracts with spot and regional suppliers to maximise resilience, particularly for customers in highly regulated geographies.

- Leverage collaboration: Explore tolling, licensing, or JV structures with specialty producers to access technical grades without full capital exposure.

Concluding perspective

Glyoxal’s market evolution through 2026 will be shaped less by headline demand surges and more by a confluence of feedstock variability, regulatory tightening, and targeted product innovation. For executives, the decisive moves are those that reduce exposure to volatile inputs, anticipate regulatory pivots, and capture upside in specialty and compliance-driven niches. PW Consulting’s full report delivers the granular segmentation, plant-level economics, and contract templates required to convert the strategic direction outlined here into executable programmes.

To access the complete data set, proprietary segmentation, and the investment-grade scenario models that inform recommended actions for 2026, visit the PW Consulting Glyoxal Market report page. The supplemental materials include downloadable templates and a supplier scorecard that buyers and corporate development teams can put to use immediately.

For detailed analysis of this topic, please visit the official page:Glyoxal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com