Antifreeze & Coolants Market — Strategic Primer for 2026 Decision-Makers

Why this study matters now

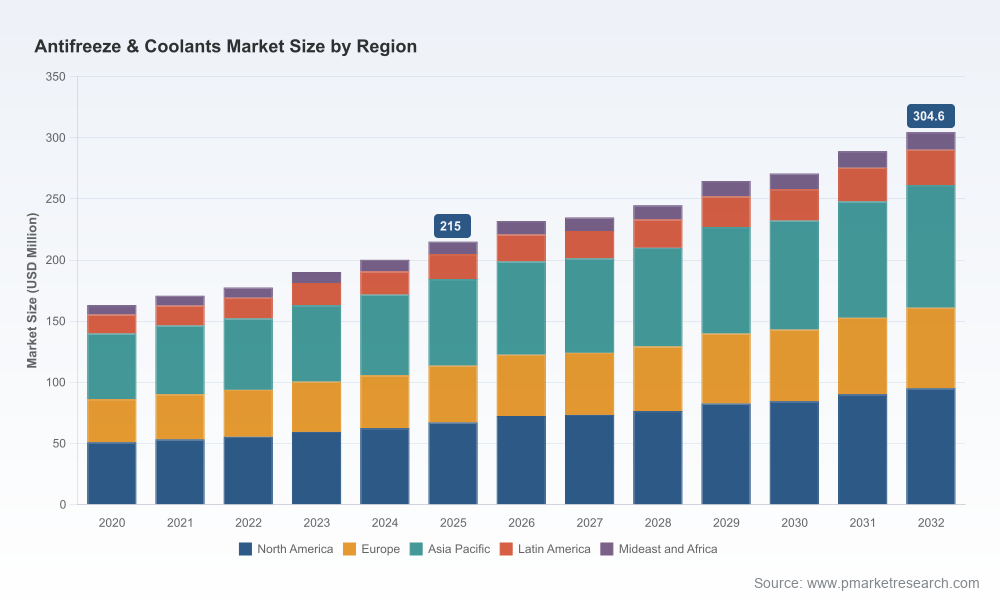

As 2026 unfolds, antifreeze and engine coolant markets are at an inflection point that will define margins, market share, and R&D roadmaps through the next business cycle. PW Consulting’s Antifreeze & Coolants Market study (base year 2025, forecast 2026–2032) provides a focused, commercially oriented view that turns macro momentum into board‑level choices. The market reached an estimated USD 215.0 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of approximately 5.23% through the 2026–2032 horizon, reaching just over USD 300 Million by 2032. These headline metrics frame a market that is neither stagnant nor hyper‑explosive—what matters now is where inside that envelope companies allocate capital, protect margins, and extract durable advantage.

Antifreeze & Coolants Market

What this introduction delivers — and what we deliberately hold back

This article functions as a strategic preview: it highlights the dynamics, competitive contours, and decision levers that senior executives, product leaders, and corporate development teams must consider for 2026. We intentionally present robust qualitative and high‑level quantitative context while withholding granular segment or regional breakdowns that form the core proprietary intelligence of the full report. That structure follows a “prequel” design: build confidence in our method and conclusions, but preserve the tactical specifics that drive trading, sourcing, and M&A decisions for subscribers and clients.

Antifreeze & Coolants Market

Practical contents of the full study (executive view)

- Market sizing and validation framework (2020–2025 historicals; 2026–2032 forecasts) with scenario modeling for conservative, baseline, and upside pathways.

- Supply‑chain heat maps: feedstock exposures, supplier concentration, freight and port bottleneck risk, and a fast‑action matrix for 12–18 month supplier negotiations.

- Regulatory and standards impact assessment—including recent ASTM revisions—and an OEM compatibility playbook for reformulations and approval timelines.

- Competitive landscape with capability and channel mapping, strategic positioning of leading players, and a CR‑based concentration analysis to inform competitive response.

- Product and packaging innovation scan: formulation trends (extended‑life, OAT, hybrid chemistries), eco‑design, and low‑waste packaging pilots to lower unit costs and improve shelf differentiation.

- Commercial intelligence tools: price elasticity models, promotional levers for B2C vs B2B channels, and a margin recovery toolkit for rising feedstock costs.

- M&A and partnership playbook: target screening criteria, valuation sensitivities, and integration risk index focused on manufacturing footprint, technical approvals, and distribution reach.

Market dynamics that should drive near‑term decisions

Several structural drivers converge in 2026 to influence strategy:

Antifreeze & Coolants Market

- Feedstock pressure and pricing volatility. Monoethylene glycol (MEG), a principal raw material for many glycol‑based coolants, has shown sharp short‑term price movement in Asia and Europe. Recent spot and CIF moves have materially increased input costs in 2026 and are forcing both formulators and contract manufacturers to reassess hedging, pass‑through policies, and purchasing cadence.

- Standards and certification shifts. ASTM International approved an updated heavy‑duty coolant specification effective in late 2025. The revision tightens test requirements for long‑life and heavy‑duty formulations and has immediate implications for OEM approval cycles, warranty exposure, and technical claims in marketing materials.

- Product and packaging innovation as commercial battlegrounds. Manufacturers are pursuing both chemistry upgrades (e.g., organic acid technologies and hybrid inhibitors) and packaging advances designed to reduce waste and distribution costs. Recent commercial launches show an emphasis on long‑life warranties, multi‑vehicle compatibility claims, and reduced‑packaging formats that lower logistical waste.

- Channel divergence. DIY retail, OEM aftermarket, and commercial fleet channels are evolving at different speeds. Each channel values different attributes—brand trust and convenience in DIY; OEM validation in the aftermarket; total cost of ownership and service support in fleets—which requires distinct product, pricing, and service models.

Competitive landscape — what the numbers and players imply

The market displays moderate concentration by revenue: our concentration analysis indicates that roughly the mid‑50s percent of revenue is controlled by the top three suppliers, and around sixty percent by the top five. This structure creates both risks and opportunities.

- Scale matters—but so does specialization. Large integrated energy and chemical players possess distribution scale, R&D budgets, and access to feedstock that enable competitive pricing and rapid reformulation for new standards. At the same time, specialized formulators and regional brands maintain strong OEM and aftermarket relationships that are hard to replicate overnight.

- Brand and channel coherence are defensive assets. Trusted consumer brands and established B2B service agreements (especially with vehicle fleets and heavy equipment operators) command pricing elasticity advantages and reduce churn during price cycles.

- Recent competitive moves are instructive. There is an observable emphasis on packaging efficiency and OAT chemistry launches, signaling that both sustainability and long‑life performance will be key purchase drivers going forward.

Key participants covered in the report include multinational integrated energy and chemical groups, specialist lubricant and chemical brands, and regional formulators who together shape access to OEMs, retail channels, and industrial users. Our company profiles analyze product portfolios, geographic coverage, formulation competencies, channel strategies, and strategic initiatives to identify capability gaps and potential partnership targets.

Implications for strategic choices in 2026

Given the macro trajectory and the updated technical standards, leadership teams should prioritize five interconnected strategic moves this year:

- Hedge and secure feedstock access: Evaluate multi‑supplier contracts, strategic inventory, and possible vertical integration with glycol producers in markets where feedstock volatility materially erodes margins.

- Accelerate formulation compliance and OEM approvals: Fast‑track testing and certification programs for revised standards to avoid time‑to‑market lag that competitors can exploit.

- Differentiate via packaging and service: Pilot low‑waste packaging and bundled service options (e.g., fleet maintenance agreements), which can increase wallet share without competing on commodity price alone.

- Rationalize portfolio by channel: Adopt differentiated SKUs and go‑to‑market plays for DIY retail, OEM channels, and commercial fleets—each requires separate pricing, marketing claims, and inventory strategies.

- Use M&A and alliances tactically: Target acquisitions that close capability gaps—technical approvals, regional manufacturing footprints, or distribution reach—rather than pursuing scale for its own sake.

Decision tools and next steps — how PW Consulting translates insight into execution

For leadership teams constrained by time and competing priorities, the full PW Consulting deliverable is structured as an execution kit, not a passive report. Deliverables include an interactive forecast and sensitivity model, a supplier risk dashboard, a prioritized list of product approvals with estimated time‑to‑market and capex implications, and a commercial playbook calibrated to each sales channel.

Typical engagements blend a one‑day executive synthesis workshop, a deep‑dive with technical teams on reformulation and OEM approvals, and a scenario‑based supplier negotiation plan. For clients pursuing inorganic growth, we provide an M&A screening package that scores targets on technical approvals, manufacturing quality systems, and distribution overlap—plus an integration checklist that minimizes revenue leakage post‑deal.

Five questions every board should ask this quarter

- How exposed are our gross margins to a sustained rise in glycol feedstock prices, and what is our pre‑defined trigger for passing through costs versus absorbing them?

- Are our formulations and testing cadence aligned with the latest standards and OEM approval timetables to avoid reactive reformulation campaigns?

- Can we extract margin and loyalty through packaging innovation and differentiated service rather than competing solely on price?

- What parts of the value chain (manufacturing, blending, distribution) should we own, partner, or outsource to reduce cost volatility and accelerate market access?

- Which targets for bolt‑on M&A or strategic alliances will most quickly close capability gaps exposed by our scenario analysis?

Where to get the full playbook

This preview highlights the strategic leverage points that will shape antifreeze and coolant competition through 2026 and beyond. The full PW Consulting Antifreeze & Coolants Market report contains the granular segmentation, regional and channel forecasts, company scorecards, and executable templates that decision‑makers need to act confidently. We intentionally withhold the detailed segment and regional splits in this primer to protect the tactical intelligence reserved for subscribers and clients.

Contact PW Consulting to request the complete study, schedule an executive briefing, or commission a customized strategic module tailored to your portfolio. In a market where feedstock shocks and standards shifts can reprice value quickly, having a clear, executable roadmap is the difference between reaction and profitable leadership.

For detailed analysis of this topic, please visit the official page:Antifreeze & Coolants Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com