L‑Hydroxyproline (CAS 51-35-4) Market — Strategic Briefing for 2026 Decision Makers

As lead analysts at PW Consulting, we present a concise but forward-looking orientation on the L‑Hydroxyproline market designed to inform executive decision-making in 2026. This briefing synthesizes market momentum, production dynamics, competitive posture and the concrete levers commercial, procurement and R&D leaders should prioritize. It intentionally showcases methodological depth while reserving the granular segmentation tables, regional and application-level breakdowns, and price decks for the full report — the precise inputs you will need to operationalize strategy are available in the downloadable intelligence package.

L-Hydroxyproline (CAS 51-35-4) Market

Market snapshot — scale, pace and structure

The L‑Hydroxyproline market has moved from a niche specialty-chemical profile toward a more diversified, higher-volume commercial posture over the 2020–2025 period, reflecting broadening demand across pharmaceutical, cosmetic, food and nutraceutical uses. Our base-year assessment places the market at USD 250.8 Million in 2025. Under our central scenario, the market expands at a compound annual growth rate (CAGR) of approximately 6.4% over the 2026–2032 forecast window, reaching roughly USD 384 Million by 2032. These headline figures underline a healthy growth trajectory that justifies near-term capacity planning and mid-term product and route-to-market investments.

L-Hydroxyproline (CAS 51-35-4) Market

Market concentration remains moderate: the top three firms account for a meaningful share of global supply, and the top five firms widen that footprint further — a structure that creates both opportunities for scale players to influence price and quality trends and openings for specialized players to differentiate on purity, regulatory compliance and customer service.

L-Hydroxyproline (CAS 51-35-4) Market

Why 2026 is a strategic inflection point

- Supply-chain resilience matters now more than efficiency alone. Rapid demand growth combined with recent capacity additions in Asia – particularly China – has created a two-speed market where lead times and certification (e.g., pharmaceutical- vs. food-grade) determine commercial outcomes. Firms that assume unconstrained supply will be exposed; those that secure diversified sources and invest in supplier qualification will gain negotiating leverage.

- Quality segmentation is increasingly value-driving. End-markets such as pharmaceuticals and high-end cosmetics command stricter specifications and shorter approval cycles. Investing in fermentation platforms and downstream purification to meet these specs can materially improve margins versus commodity-grade supply.

- Regulatory and product-innovation tailwinds are active. Recent capacity expansions by major European players and new cosmetic-grade launches by incumbents signal that established chemical players and life-science specialists are both contesting higher-margin segments. This accelerates the need for clear positioning: compete on price in commodity segments, or on certified quality and service in regulated channels.

Production dynamics — what to watch

Two technical realities will shape supply and competitiveness through 2032:

- Process profile: Microbial fermentation and enzymatic biotransformation now account for a dominant share of global output. These biological routes deliver better yields and impurity profiles for high-purity applications and are central to companies targeting pharmaceutical and cosmetic customers.

- Geographic production concentration: Chinese manufacturers constitute a substantial portion of global installed capacity and have recently added significant incremental capacity between 2023 and 2025. This concentration reduces global supply friction but raises geopolitical and regulatory sourcing risks for multinational buyers.

Practically, that means procurement teams should incorporate scenario-based supply models that capture: capacity availability by technology platform, variation in compliance documentation timelines, and the incremental cost of dual‑sourcing to mitigate supplier- or country-specific risk.

Competitive landscape — strategic positions and implications

The market is populated by a mix of global specialty ingredient houses, vertically integrated amino-acid manufacturers, and regionally focused intermediates suppliers. Below we summarize the strategic posture of representative firms and what their behaviors imply for your strategy (note: this is a qualitative read; detailed company scorecards are available in the full report).

- Kyowa Hakko Bio Co., Ltd. (Japan) — Premium fermentation expertise and a longstanding reputation in high-purity amino acids position Kyowa as a supplier of choice for regulated pharma and life‑science applications. Their presence signals that premium, compliance-led supply remains a defensible niche.

- Evonik Industries AG (Germany) — A global specialty-chemicals leader that has recently expanded pharmaceutical-grade hydroxyproline capacity in Europe. Evonik’s moves underscore an institutional bet on higher-margin, regulated markets and signal platform investments that could accelerate certification timelines for European customers.

- Wuxi Jinghai Amino Acid Co., Ltd. (China) — Represents a high-volume, fermentation-driven commodity producer that also services high-purity needs. Firms like Wuxi illustrate how scale and fermentation capability can compress unit costs while maintaining acceptable quality for many end-users.

- Hebei Fangrui Biological; Shandong Jinyang Pharmaceutical; Ningbo Inno Pharmchem; Suzhou Biosynthetica; Beile Group; Nantong Puyer; Tianjing Jingye; Henan Rane Chemical; Shanghai Yingrui Biopharma (China) — This cohort covers industrial, food and pharmaceutical supply positions: from bulk intermediates to high‑purity derivatives. Their aggregate behavior — particularly in expanding capacity and competing on price — is the primary driver behind regional supply abundance and competitive tendering pressures.

Strategic takeaway: The competitive field is bifurcating. Large multinational specialty players will compete for regulated, high-margin segments. At the same time, a robust Chinese supply base will continue to anchor global commodity volumes and act as the marginal supplier influencing spot-pricing dynamics. For buyers, this creates opportunity to segment sourcing strategies: secure long-term, certified supplies for differentiated SKUs while leveraging spot/contract volumes from competitive bulk suppliers for commoditized needs.

Practical content of the full PW Consulting report

Our full market study is designed to be operationally actionable for corporate functions (strategy, M&A, procurement, supply chain, R&D). Key deliverables include:

- Multi-scenario market model (2020–2032) with forecasted volumes and revenues under conservative, central and accelerated demand scenarios.

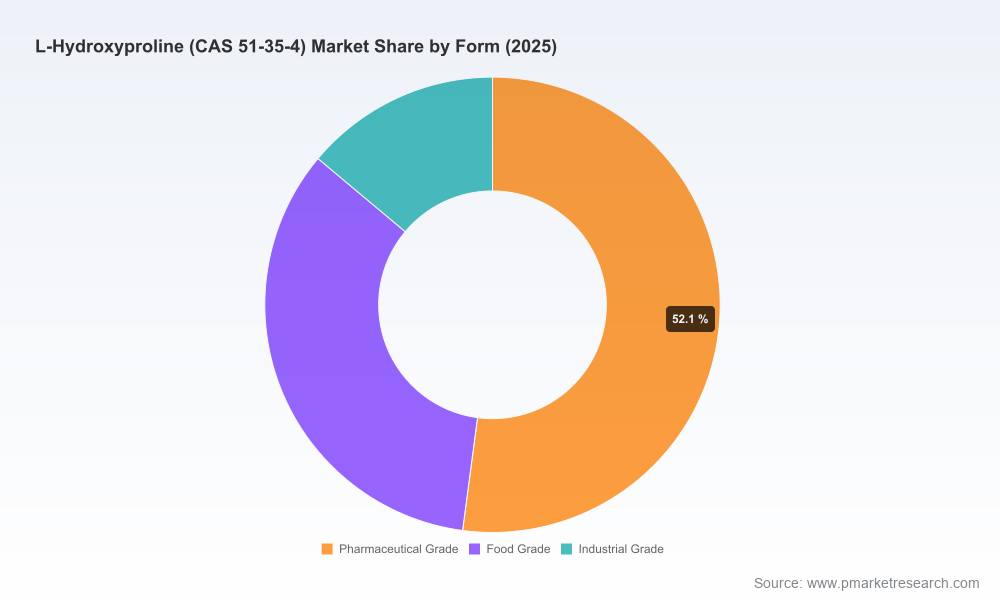

- Segmented demand and pricing matrices by form, application and region — useful for SKU-level margin analysis (note: these segment tables are intentionally excluded from this preview).

- Capacity map and manufacturer profiles with production technology overlays (fermentation vs. enzymatic vs. chemical synthesis), enabling supplier qualification and dual-sourcing design.

- Competitive scorecards for the leading manufacturers, including product specs, approval statuses, typical lead times, and commercial terms.

- Supply‑risk heat map — including geopolitical, regulatory and feedstock risk vectors — with recommended mitigation playbooks.

- Go‑to‑market and commercial playbooks for companies seeking to enter or expand in pharmaceutical, cosmetic and food-grade channels.

- M&A and partnership screening tool: quick filters to identify high‑value targets (technology, capacity, regulatory certificates) and an accompanying valuation sensitivity model.

How to convert insight into 2026 decisions

- Procurement leaders: Move to a two‑tier sourcing strategy: (1) long‑term, certified supply agreements for high‑value SKUs with clear audit and qualification milestones; (2) flexible spot/short-term contracts with competitive bulk suppliers to manage cost volatility.

- R&D and product teams: Prioritize formulation work that leverages the higher-purity profiles enabled by fermentation/enzymatic routes to create differentiated, higher-margin offerings (e.g., advanced nutraceuticals and cosmeceuticals).

- Operations and investment committees: Evaluate near-term capacity expansions only where technology advantage or regulatory certification creates durable differentiation. For market entrants, consider toll-manufacturing and partnership models to reduce capital intensity.

- Corporate development: Use the report’s M&A screening framework to identify targets that add either: certified production capacity, process IP (fermentation or enzymatic know-how), or market access in under-served regulatory regions.

Regulatory and market signals to monitor

- Capacity expansions by established specialty players in Europe and Japan — these will change certification lead times and customer expectations for pharmaceutical-grade supply.

- New product introductions targeted at cosmetic and anti‑aging segments — they signal demand creation that can quickly pull specification expectations towards higher-purity inputs.

- Concentration of production capacity by region — a double-edged sword for global buyers, offering cost advantages but increasing exposure to localized disruptions and compliance risk.

Final perspective — why the full dataset matters

L‑Hydroxyproline is no longer a niche input; it is a strategic raw material whose supply-chain architecture, production technology and quality tiers will materially affect product economics across pharmaceuticals, cosmetics and food-related segments through the rest of the decade. The headline growth rate (6.4% CAGR, 2026–2032) and the scale of the market by end‑2025 are enough to justify active strategy work — but operational decisions require the granular, SKU- and region-level inputs we have compiled.

PW Consulting’s full report delivers those inputs: granular segmentation, company-level scorecards, scenario models, and executable playbooks tailored for corporate, procurement and M&A teams. If you are planning sourcing strategies, capacity investments or portfolio moves in 2026, this intelligence is the difference between reactive decisions and proactive competitive advantage.

For access to the full dataset, modeling appendices and supplier due‑diligence templates, contact PW Consulting or visit the report landing page for licensing and bespoke advisory engagements.

For detailed analysis of this topic, please visit the official page:L-Hydroxyproline (CAS 51-35-4) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com