PW Consulting: Polymer Ligating Clips Market to Reach USD 827.35 Million in 2025 with 9.45% CAGR

Health |

2026-07-09 15:18:59

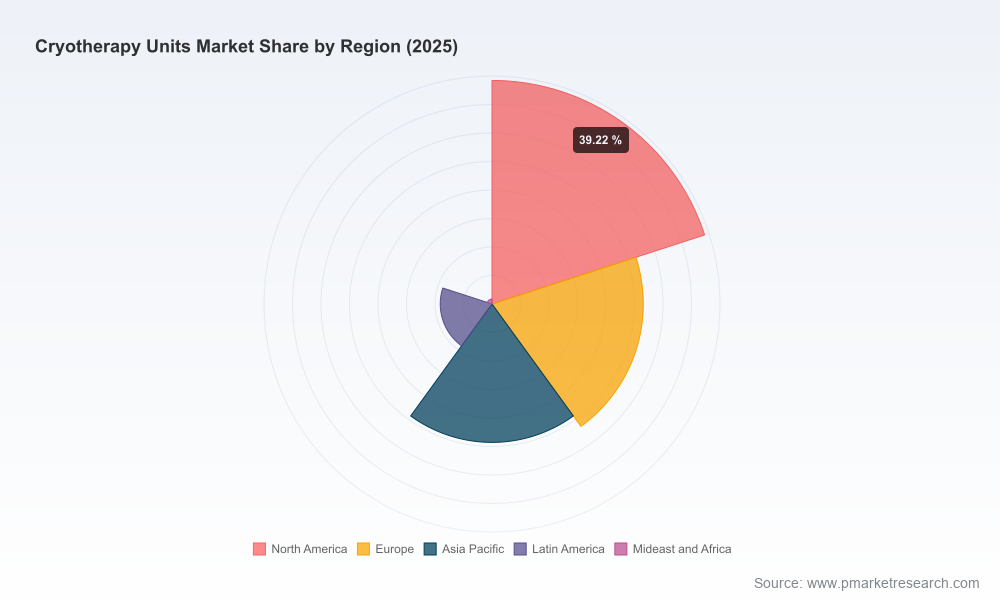

Cryotherapy units are entering a maturation phase where regulatory tightening, reimbursement shifts, and technology substitution are converging to reshape competitive advantage. Our market model — using 2025 as the base year and a forecast window through 2032 — estimates the global market to be on a clear upward trajectory, growing at a compound annual growth rate (CAGR) of 6.7%. Historical momentum since 2020 has accelerated into the mid-2020s, and the market is forecast to materially expand by 2032. Market concentration remains relatively low (CR3 ≈ 26.5%; CR5 ≈ 31.2%), signalling fragmentation and plentiful opportunities for scale plays, vertical integration, and roll-up strategies.

Cryotherapy Units Market

Regulatory compliance is now a quadrant-level business risk and value driver. From February 2026 the FDA’s Quality Management System Regulation (QMSR) and the reinforced expectation of ISO 13485:2016 for finished medical devices materially raise the bar on supplier qualification, product design controls and post-market surveillance. Executives who treat compliance as an engineering checkbox rather than a strategic asset will experience higher time-to-market and higher transaction execution risk.

Cryotherapy Units Market

Reimbursement changes are creating near-term demand pull for certain system architectures. Non-opioid device codes and specific Medicare coverage for temperature-regulated electric cooling systems open new revenue pathways for clinic and outpatient adoption. Market entrants that combine clinical-evidence programs with payer engagement can convert reimbursement coverage into sustainable installed-base growth.

Cryotherapy Units Market

Technology substitution (liquid nitrogen to electric cooling) shifts the cost curve. Electric systems remove recurring LN2 procurement and handling risks but raise initial CapEx and technical-support requirements. Procurement, OPEX modelling and service contracts must be rethought across the value chain.

Demand drivers — multi-source: Post-surgical pain management adoption (supported by emerging reimbursement codes), growth in sports/rehabilitation applications and wellness-adjacent placements (corporate and consumer-facing studios) combine to broaden addressable markets beyond traditional clinics. The net effect is a widening buyer base and diversified revenue mix across device sales, consumables, and service contracts.

Supply-side friction — compliance, capital intensity and component supply: The effective requirement for ISO 13485-aligned quality systems and the increasingly formalized 510(k) pathway create longer product development cycles and higher validation costs. At the same time, electric cooling designs concentrate supplier risk around power electronics and thermal management sub-systems, while LN2-based units carry operational and logistics burdens.

Economics — CapEx/Opex trade-offs: Buyers now evaluate lifetime cost-of-ownership not only by device price but by nitrogen logistics, staff training, safety compliance and insurance exposure. Vendors that can model and guarantee TCO improvements through bundled service agreements will gain negotiating leverage during procurement cycles.

Consolidation opportunity: Low market concentration implies acquisitive routes to scale are available. Strategic acquirers can chase geographic coverage, channel control (clinics and studio chains), consumables lock-in, or capabilities (R&D for electric cooling).

Zimmer MedizinSysteme GmbH (Neu-Ulm, Germany) — a long-established player in clinical and sports markets with a broad portfolio of whole-body and localized systems. Their January 2026 product expansion toward electric, multi-use clinical chambers is a strategic signal: incumbents are migrating to electric platforms to capture reimbursed use-cases and reduce operator burden associated with cryogens.

CRYO Science (Poland; North American operations) — focused on both nitrogen and electric models for clinical and wellness customers. Their presence illustrates a dual-platform strategy that many mid-sized vendors are using to hedge technology transition risk while protecting installed-base revenue.

CRYONiQ s.r.o. (Slovakia; US operations) — provides whole-body and localized systems with an emphasis on manufacturing standards (ISO 9001). Their hybrid channel approach (professional and home-use systems) highlights the tension between regulated clinical adoption and the high-growth consumer/wellness segment.

Cryo Innovations (Newport Beach, CA) — targets clinics, chiropractors and athletic programs with XR-family chambers. Their focus on clinician workflows and compact localized devices suggests an emerging segmentation by place-of-care and channel-focused product design.

CryoBuilt (USA) — a US-based electric whole-body chamber manufacturer with a significant installed base in clinics and studios. Companies like CryoBuilt demonstrate that domestically manufactured electric platforms can accelerate adoption when combined with turnkey installation and service offerings.

For leaders making resource allocation, M&A, product development or GTM decisions in 2026, the following priorities should be considered non‑optional:

Immediate compliance audit (0–90 days): Map product portfolios and supplier contracts to ISO 13485:2016 and FDA QMSR expectations. Identify gaps in technical documentation, supplier controls, and post-market surveillance that will delay 510(k) activities or contract wins.

Reimbursement-first product validation: Prioritize clinical evidence generation for use-cases that attract non-opioid device codes and Medicare coverage (e.g., post-operative pain). Structure trials to measure endpoints recognized by payers and to support cost-effectiveness claims.

CapEx/Opex commercial models: Develop financing and subscription offers to offset higher initial pricing for electric platforms. Offer service bundles that convert CapEx into predictable recurring revenue while demonstrating lower lifetime costs for buyers.

Channel and installed-base playbook: Build service networks and consumables ecosystems to monetize after-sale. Consider regional service hubs and remote diagnostics to reduce downtime and increase attachment rates for consumables and upgrades.

M&A screening criteria: Target asset-light service providers, localized manufacturing capabilities, or niche application specialists. Because the top firms do not dominate the market, disciplined consolidation can rapidly increase scale while creating distribution advantages.

Product roadmap: Accelerate electric cooling R&D focused on modularity, safety interlocks and remote monitoring to meet both regulatory and payer expectations. Design for ease-of-installation and minimal facility modification to lower adoption friction in outpatient settings.

Market sizing and forecast model (2020–2032): a reproducible model calibrated to 2025 base-year data with scenario sensitivity to key inputs such as adoption rates for electric platforms and reimbursement penetration.

Regulatory and reimbursement playbook: step-by-step checklists for ISO 13485 alignment, 510(k) readiness, and payer engagement templates tailored to non-opioid device code submissions.

Commercial due diligence toolkit: buyer and seller checklists for M&A, a prioritized list of targets by strategic fit, and a valuation sensitivity matrix reflecting service-revenue attachment and installed-base monetization.

Procurement and TCO calculators: CapEx vs Opex models comparing LN2 and electric architectures, including scenarios for financing, service agreements and consumable consumption rates.

Competitive benchmarking: profiles of leading vendors, product feature-maps, distribution footprints and go-to-market strategies — sufficient to inform strategic choices without disclosing proprietary customer lists.

Strategic growth playbook: go-to-market approaches for clinics, hospital outpatient departments, sports organizations and consumer-wellness chains, plus a 90–365 day tactical plan for commercialization.

The combination of a mid-single-digit CAGR, a historically expanding base, regulatory tightening and reimbursement opportunities makes 2026 a pivotal year for positioning. Firms that move early to align product design, evidence generation and commercial models with the new regulatory and payer environment will convert structural changes into durable competitive advantages. Conversely, firms that defer compliance investments or ignore the CapEx/Opex trade-offs between LN2 and electric systems risk margin compression and slower adoption.

PW Consulting’s full Cryotherapy Units Market research provides the granular tools, model files and playbooks executives need to convert insight into execution. For boards and leadership teams planning capital allocation, product roadmaps or inorganic growth this year, the study functions as both a risk-mitigation manual and an opportunity map. Access the full intelligence pack to obtain the detailed scenario models, validated supplier lists, and M&A screening outputs needed to govern decisions across 2026.

For detailed analysis of this topic, please visit the official page:Cryotherapy Units Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com