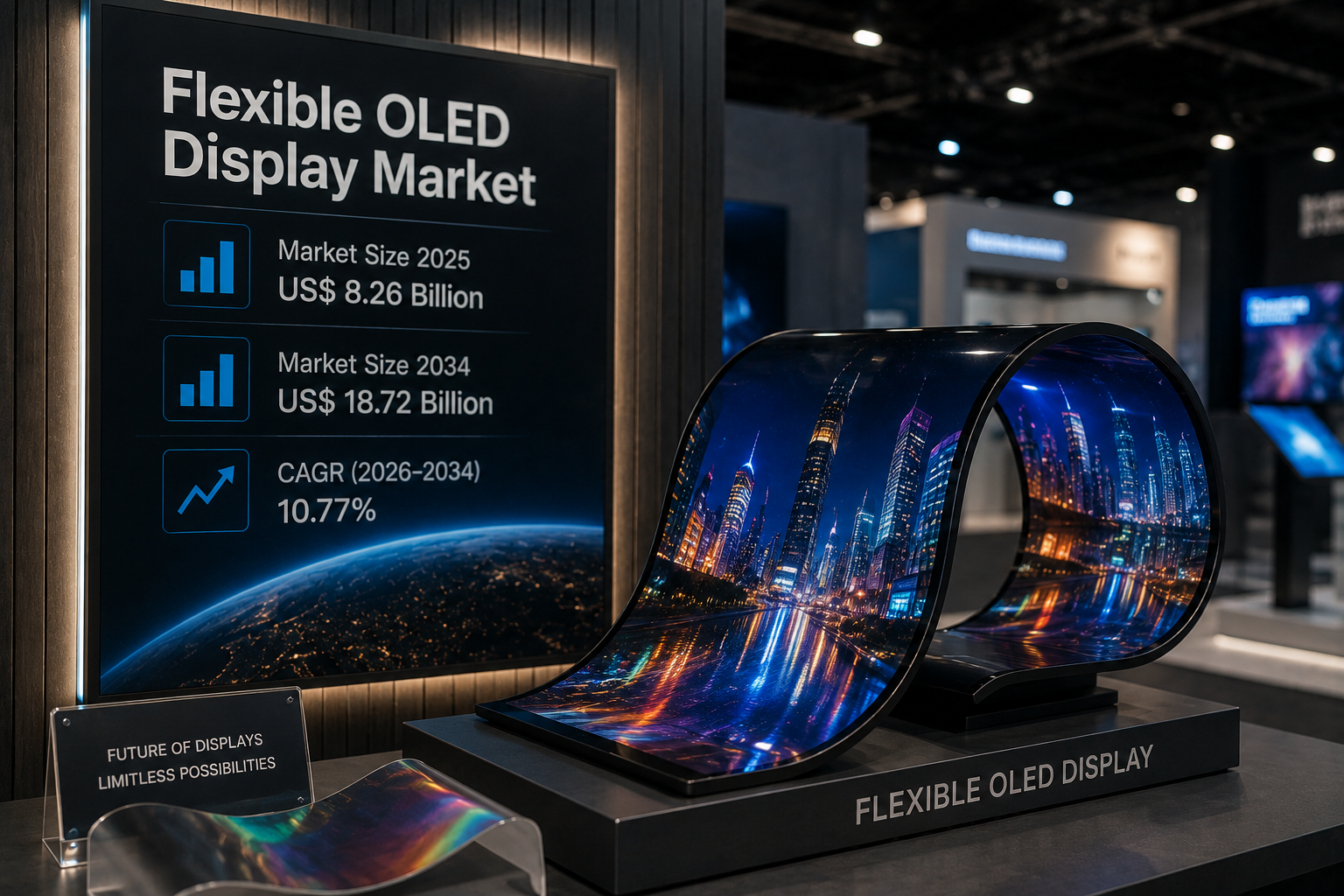

North America Flexible OLED Display Market Size, Share, and Future Growth Opportunities

Technology |

2026-06-24 13:02:13

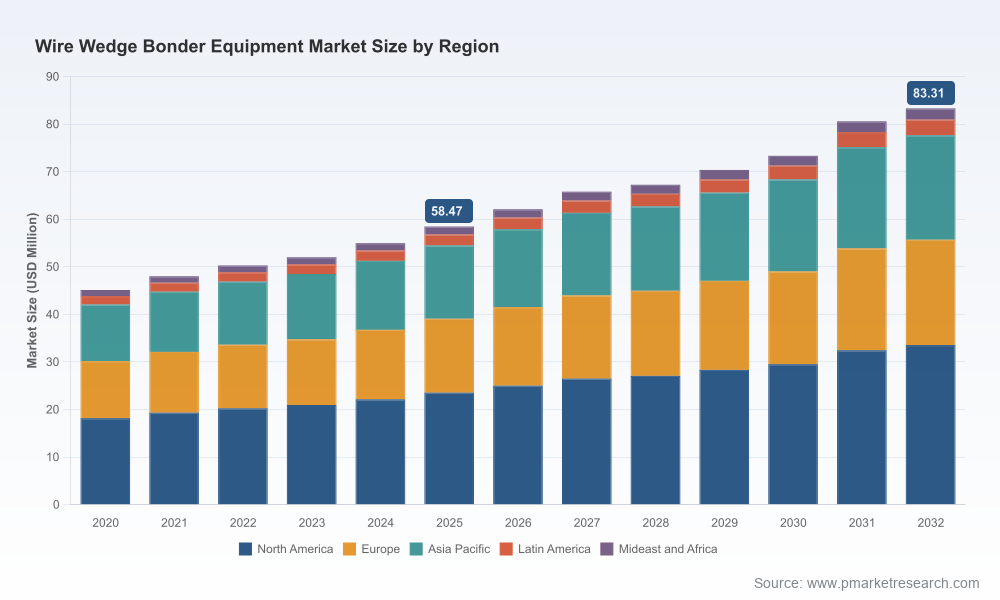

As organizations set capital allocation and product roadmaps for 2026, understanding the Wire Wedge Bonder Equipment market is no longer a niche engineering exercise — it is a strategic imperative. PW Consulting’s latest market research uses 2025 as the base year, tracks historical performance from 2020–2025, and projects the market through a 2026–2032 forecast window. The market delivered steady expansion through the historical period and is projected to grow at a compound annual growth rate (CAGR) of 5.2% over the forecast horizon. Our topline sizing shows a sustained, technology‑led upswing from the early 2020s into the next decade, reflecting both advanced packaging demand and the increasing precision requirements of power and photonic device assembly.

Wire Wedge Bonder Equipment Market

Capital intensity and timing. Wire wedge bonders are foundational capital equipment for semiconductor packaging and power device assembly. Procurement lead times, technology refresh cycles, and retrofit windows are now synchronized with broader industry inflection points — from power semiconductor transitions to higher UPH demands in wafer‑level workflows.

Wire Wedge Bonder Equipment Market

Risk management. Tariff shifts, component trade flows, and certification regimes are creating discrete risk pockets across supply chains. Boards and procurement chiefs need granular scenarios to quantify the impact of trade policy and local content pressures on equipment TCO.

Wire Wedge Bonder Equipment Market

M&A and partnership plays. Equipment makers, automation integrators, and materials suppliers are repositioning through targeted product launches and ecosystem partnerships. Buyers and investors need a compass to separate strategic acquisitions from tactical tuck‑ins.

Operational leverage. Manufacturers deciding between manual, semi‑automatic and fully automatic topologies must weigh throughput, yield, and floor‑space tradeoffs. This research translates market dynamics into actionable procurement and retrofit checklists for 2026 CapEx cycles.

Several structural trends underpin the market trajectory. First, automation and throughput remain primary value drivers: equipment that increases units‑per‑hour (UPH) while preserving bond integrity commands adoption in high‑volume fabs and power device lines. Second, the technical needs of power semiconductors, photonics and advanced packaging are diverging, creating differentiated demand profiles for heavy‑wire, ribbon and fine‑wire bonding modalities. Third, regulatory and trade developments have altered sourcing economics and logistics; buyers must now build contingency routing into procurement plans. Finally, the vendor landscape exhibits moderate concentration — the top three to five suppliers account for a meaningful share of installed base and R&D momentum — making competitive shifts disproportionately impactful on OEM sourcing strategies.

Understanding vendor capabilities and roadmaps is vital for sourcing, partnerships, and M&A diligence. The ecosystem combines legacy bond specialists, automation leaders, and regional innovators. Key players include:

Kulicke & Soffa Industries, Inc. (Philadelphia, PA, USA) — offers advanced solutions for power semiconductor bonding, including vertical wire options and inline inspection capabilities tailored to high‑reliability applications.

ASM Pacific Technology Ltd. (Singapore) — pushes next‑generation automation and high‑throughput bonders designed for modern semiconductor manufacturing lines.

Hesse Mechatronics GmbH (Germany) — known for its Bondjet series, integrating fine‑wire and heavy‑wire ultrasonic wedge bonding with automation for challenging RF and telecom assemblies.

Micro Point Pro Ltd (Israel) — focuses on dual‑mode systems suited for R&D and low‑volume high‑precision production, enabling deep‑access wire feed and mixed‑material bonding.

WestBond, Inc. (Anaheim, CA, USA) — specialist in wedge configurations optimized for aluminium wire bonding in microelectronics packaging.

TPT Wirebonder GmbH & Co. (Germany) — offers semi‑automatic platforms supporting multiple bonding modes aimed at flexible production environments.

Shinkawa Ltd. (Japan) — focuses on compact, high‑speed platforms that maximize UPH within constrained footprints.

Palomar Technologies, Inc. (Carlsbad, CA, USA) — precision wedge bonding solutions that address photonic and microelectronic device tolerances.

Cho‑Onpa Co., Ltd. (Japan) — advanced wedge systems for semiconductor packaging applications.

F&K Delvotec Bondtechnik GmbH (Germany) — solutions for heavy wire and ribbon bonding in power and automotive electronics.

DIAS Automation (Hong Kong) — integration‑centric providers, melding automation and bonding for scalable production lines.

The competitive frame is dynamic: the three‑and‑five‑firm concentration ratios indicate that while global leaders capture substantial share, meaningful opportunity exists for fast‑moving specialists and automation integrators to displace incumbents in targeted segments.

Product cadence: Several leading vendors refreshed portfolios in late 2024–2025. Notable examples include platform launches focused on power bonding configurations and high‑speed, compact UPH platforms. These launches signal vendors’ bets on power electronics and space‑constrained fab environments.

Standards and certifications: Select OEMs report expanded ISO and regulatory compliance for specialized markets such as RF, defense and medical assembly — a factor that will influence vendor selection where regulated end‑markets confer premium margins.

Trade and policy movement: Import tariff updates and shifts in equipment trade flows have compressed procurement windows and increased the value of dual‑source strategies. Industry events and technical workshops scheduled in 2026 continue to serve as focal points for standards discussion and supply‑chain matchmaking.

This preview is meant to position leaders for immediate 2026 choices. The commissioning report provides operational depth and decision tools, including:

Validated market sizing and scenario forecasts (base year 2025; forecast 2026–2032), with sensitivity tables and upside/downside triggers.

Technology benchmarking: performance matrices across UPH, bond types, footprint, automation interfaces, and inspection integration.

Vendor dossiers and capability maps: R&D posture, service networks, spare parts economics, and upgrade pathways for established and challenger suppliers.

Procurement playbook: RFQ templates, CapEx vs. lease decision frameworks, lead‑time mitigation tactics, and lifecycle maintenance models.

Supply‑chain risk scoring: tariff sensitivity analysis, alternative sourcing routes, and contingency workflows for critical subcomponents.

M&A and partnership heatmaps: targets ranked by technological fit, installed base synergies, and integration complexity.

Use‑case deep dives: adoption checklists for power electronics, photonics, and advanced packaging, including retrofit versus greenfield ROI comparisons.

Embed procurement agility. Given lead‑time sensitivity and evolving tariffs, companies should adopt staged ordering and hold strategic optionality in supplier contracts for Q3–Q4 2026 buildouts.

Prioritize automation where throughput drives margin. Firms with high‑volume packaging workloads should accelerate validation of fully automated topologies to capture yield and labor arbitrage.

Segment roadmaps by device family. Treat power semiconductor and photonic assembly as distinct investment tracks — each has differentiated equipment specs, service needs and certification requirements.

Use vendor roadmaps to de‑risk technology bets. Partner with suppliers that demonstrate clear upgrade pathways (vision systems, inline testing, robotics interfaces) to protect CapEx over multiple product cycles.

Consider bolt‑on acquisitions for system integration. Automation integrators and software specialists can accelerate time‑to‑value for in‑line inspection and adaptive bonding recipes.

This article is designed as a decision catalyst, not a replacement for the full intelligence asset. PW Consulting’s complete study contains the granular models, vendor scorecards, and procurement instruments executives will need to finalize 2026 budgets and partnership agreements. If you are planning CapEx, negotiating vendor terms, or evaluating M&A targets this year, the full report will convert the directional insights above into executable plans and quantified scenarios.

Boards, procurement leads, and R&D heads should request the full PW Consulting Wire Wedge Bonder Equipment Market dossier to obtain the confidential segmentation matrices, vendor financials, and scenario models that are intentionally omitted here. Those assets enable precise ROI modelling, supplier selection, and production ramp sequencing necessary for confident 2026 decision‑making.

For detailed analysis of this topic, please visit the official page:Wire Wedge Bonder Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com