Ethylene Market Overview: Key Drivers and Challenges

Other |

2026-05-13 05:28:18

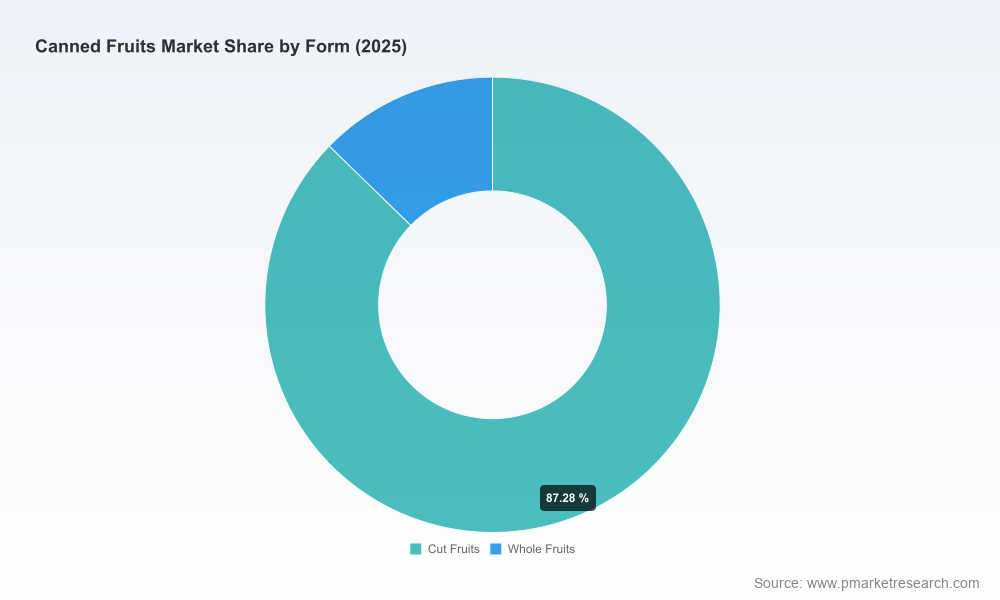

As companies set priorities for 2026, the canned fruits sector demands a recalibrated playbook. PW Consulting’s latest market study (base year 2025; forecast period 2026–2032) documents a resilient, mid-single-digit growth trajectory driven by structural consumption patterns, evolving channel economics, and renewed consolidation activity. The global market, measured in USD Billion, expanded from the low double-digits in 2020 to an estimated 12.91 billion in 2026 and is projected to reach approximately 16.17 billion by 2032 — reflecting a compound annual growth rate (CAGR) of about 4.02% over the forecast window.

Canned Fruits Market

This briefing distills the report’s actionable implications for executive decision-making in 2026 while deliberately preserving the granular segmentation tables and proprietary forecasts that are available in the full study. Consider this a strategic trailer: deep enough to align leadership around direction and risk, but designed to drive engagement for the full intelligence package.

Canned Fruits Market

Growth is steady, not explosive. The trajectory through 2025–2026 demonstrates recovery and gradual expansion rather than a sharp spike, indicating opportunities for margin capture through efficiency and portfolio optimization rather than volume-only strategies.

Canned Fruits Market

Concentration is moderate. The top-tier competitors command a meaningful share of market value, but the industry remains open to challengers and regionally strong operators. This mixed structure favors both strategic consolidation and differentiated niche plays.

Cost inflation is real and current. Recent U.S. Producer Price Index readings for fruit and vegetable canning indicate upward pressure on processing costs as of March 2026, underscoring the need for dynamic pricing, procurement hedging, and productivity investments.

Regulatory and quality risks are prominent. Class II recalls in late 2025 related to potential lead contamination underscore how quickly brand and channel access can be impaired without robust traceability and supplier governance programs.

Demand resilience and substitution dynamics: Canned fruits continue to benefit from shelf stability and value perception in both retail and foodservice. However, competition from fresh, frozen, and minimally processed alternatives — as well as shifting nutrition preferences — requires SKU-level renewal and clearer consumer propositions (e.g., low-sugar, organic, fortified options).

Channel evolution: Traditional supermarket and foodservice channels remain important, but e-commerce and convenience formats are changing assortment and pack-size economics. Retailers are leveraging private-label strategies aggressively; manufacturers must balance branded innovation with private-label cost leadership.

Input and processing economics: Rising PPI readings for canning point to margin squeeze unless mitigated by procurement strategies, yield improvements, and strategic price adjustments. Seasonal capacity and packing cadence are operational levers — extending packing seasons or investing in line efficiency can materially improve throughput during peak harvests.

Regulatory and food safety posture: Recent recalls and existing commodity specifications for canned fruit used in institutional programs highlight the commercial value of impeccable compliance and rapid-response capabilities — both for market access and contract performance under government or large-retailer programs.

The industry roster includes longstanding cooperatives, large processors, and multi-brand manufacturers. Key players include agricultural cooperatives and processors with deep vertical ties, national branded manufacturers with wide retail distribution, and specialized processors focused on private label and foodservice. Recent developments have accelerated consolidation and illustrate the types of moves that can quickly reshape capability maps.

Pacific Coast Producers — A cooperative with strong private-label and branded capabilities that completed a notable asset acquisition in March 2026 and operationally extended packing seasons to absorb acquired volumes. Strategic implication: targeted M&A that combines brand licensing and physical capacity can unlock immediate shelf presence but requires disciplined integration of licensing, inventory, and seasonal workforce.

Seneca Foods (including Libby’s) — A national processor-distributor with both branded and private-label reach. Strategic implication: national scale and multi-channel distribution enable margin arbitrage, but sustaining value depends on SKU rationalization and cost-to-serve optimization.

Rhodes Food Group & Tree Top — Operators focused on flexible contract packing and quality shelf-stable products for retail and foodservice. Strategic implication: co-packing and B2B service models can be defensive plays for manufacturers seeking utilization without large capital outlays.

Hunt’s (ConAgra Brands) — A brand-led manufacturer with strong retail recognition. Strategic implication: brands retain pricing power, but only when coupled with clear differentiation (ingredient quality, provenance, sustainability credentials) and disciplined marketing ROI.

Executives must translate the market’s steady growth and fluctuating cost/regulatory environment into concrete choices. Below are priority decision areas we recommend for boards and executive teams heading into 2026 planning cycles:

Portfolio and SKU rationalization: Identify underperforming SKUs and reallocate working capital toward higher-margin or higher-growth formats (e.g., portion packs, sugar-reduced offerings, value-added blends). Use SKU-level contribution analysis calibrated to channel economics.

Supply-chain resilience: Implement multi-sourcing for critical inputs, lock in seasonal contracts with growers where advantageous, and invest in traceability systems to minimize recall exposure and expedite corrective action when issues occur.

Price and cost playbook: Build a dynamic pricing model that can simulate pass-through under different PPI scenarios and margin targets. Complement pricing with productivity initiatives on the processing line to protect gross margins.

M&A and capacity strategy: Prioritize targets that offer complementary distribution, brand licensing, or seasonal capacity relief. Integration playbooks should emphasize inventory harmonization, licensing rights capture, and workforce planning — precisely what recent asset transactions have made clear.

Food safety and regulatory readiness: Move from compliance as checklist to compliance as competitive advantage. Investments in lab testing cadence, supplier audits, and rapid recall response plans reduce downside and protect buyer relationships.

Channel and customer segmentation: Differentiate GTM strategies for national retail, regional grocers, e-commerce, and foodservice. Private-label partnerships can accelerate volume growth but require relentless focus on cost management and supply reliability.

Sustainability and consumer positioning: Reinforce provenance claims, reduce packaging footprint where possible, and align sustainability metrics to procurement and marketing. These measures increasingly influence shelf placement and pricing elasticity among core buyers.

The full PW Consulting study is structured to convert insight into immediate action. Highlights include:

Robust, auditable demand model with historical calibration (2020–2025) and scenario-based forecasts to 2032.

Competitive mapping, including company profiles, capability audits, and M&A value drivers tailored for acquirers and sell-side advisors.

Supply-chain heatmaps and an operational playbook for packing season optimization, co-packing evaluation, and capacity investment decisions.

Regulatory risk matrix and compliance road map designed to mitigate recall exposure and satisfy institutional procurement specifications.

Commercial playbooks for branded vs private-label strategies, price elasticities by channel, and go-to-market recommendations to improve retailer economics.

Financial impact tools including margin scenario models that incorporate PPI movements, input cost pass-through assumptions, and capital allocation trade-offs.

The canned fruits market in 2026 presents a classic strategic choice: pursue incremental volume through channel expansion and private-label partnerships, or pursue margin-rich differentiation through brand investment, product innovation, and operational excellence. The market’s steady CAGR and the moderate concentration level mean both routes are viable, but each requires distinct capabilities — disciplined M&A and integration for scale plays, and marketing plus supply-chain precision for premiumization.

PW Consulting’s full report provides the granular segmentation, regional, and SKU-level analytics necessary to validate these strategic choices and to operationalize them through 2026 and beyond. For leadership teams that must make resource allocation decisions this year, the intelligence in the full study converts macro trends into executable 90–180 day plans and three-year roadmaps.

To access the full datasets, proprietary models, and a tailored briefing for your executive team, please visit the PW Consulting report page or contact our industry practice lead for a consultation.

For detailed analysis of this topic, please visit the official page:Canned Fruits Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com