Discover One of the Best Strip Clubs in London for a Premium Night Out

Party |

2026-06-30 09:30:44

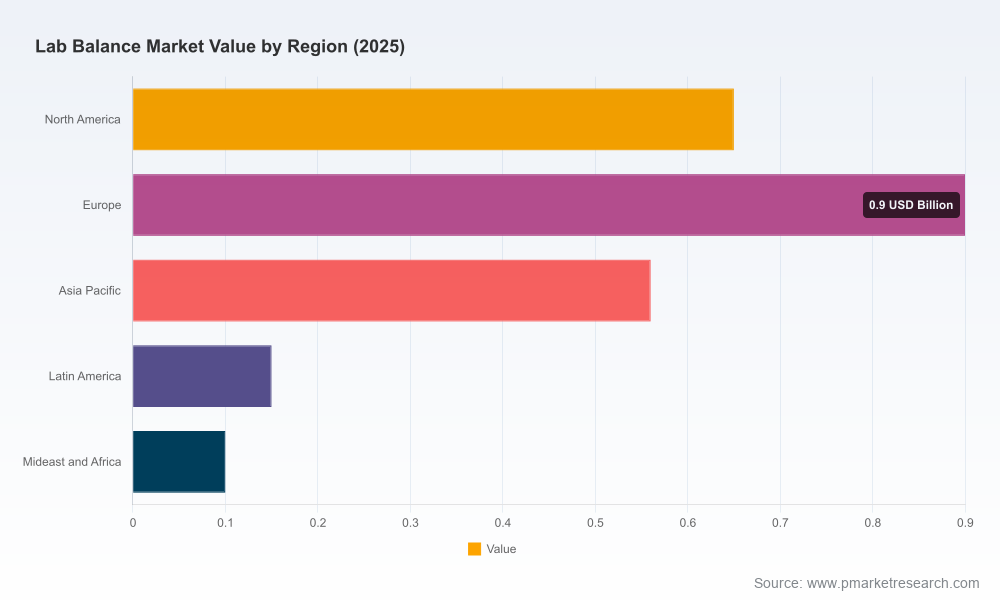

As organizations reset capital plans and compliance roadmaps for 2026, understanding the lab balance market’s trajectory is no longer a procurement exercise — it’s a strategic capability decision. PW Consulting’s Lab Balance Market research synthesizes five years of historical data (2020–2025), a calibrated base year (2025), and a 2026–2032 forecast to translate macro dynamics into boardroom actions. The market expanded from approximately USD 1.85 Billion in 2020 to USD 2.36 Billion in 2025 and, at a compound annual growth rate of 4.7%, is projected to reach roughly USD 3.25 Billion by 2032. This brief highlights the report’s strategic value for 2026 while intentionally preserving the detailed segmentation and datasets to encourage direct engagement with the full study.

Lab Balance Market

Regulatory inflection point: Mandatory enforcement of revised pharmacopoeial guidance and pharmaco‑regulatory alignment in early 2026 materially changes minimum sample weight determination and site qualification practices. Organizations must reassess installed base compliance and qualification cadence now, or risk production and release delays during audits.

Lab Balance Market

Shift from capital purchase to capability delivery: Buyers increasingly view balances as instruments within a broader analytical workflow — demand is shifting toward configurable platforms, embedded qualification workflows, and integrated calibration traceability rather than standalone price‑driven units.

Lab Balance Market

Service-driven economics: As compliance burdens rise, calibration, software validation, and lifecycle qualification services become a meaningful recurring revenue opportunity for suppliers and a predictable OPEX line for end users. TCO models must be revisited to include regulatory-driven service frequency.

Consolidation and concentration: The segment is meaningfully concentrated at its top tier, creating both barriers and strategic openings for mid‑market players pursuing niche differentiation or adjacencies.

Market sizing & forecast: Historical reconciliation (2020–2025), base‑year normalization (2025), and probabilistic forecasting (2026–2032) with sensitivity bands around the 4.7% central CAGR.

Scenario analysis: Three practical market scenarios (baseline, accelerated adoption, and regulatory‑intensive) with trigger events, likelihoods, and decision trees for procurement and R&D sequencing.

Regulatory impact playbook: Line‑by‑line translation of revised pharmacopoeial requirements into purchase specifications, validation protocols, and internal SOP updates that procurement, QA, and QA‑regulatory teams can operationalize.

Buyer personas & procurement cycles: Segmented buyer archetypes (from QC lab managers to central procurement), procurement calendars, approval thresholds, and negotiation levers mapped to vendor value propositions.

TCO & lifecycle models: Configurable financial templates that capture capital, calibration, validation, downtime, and replacement risk to compare vendor proposals on a like‑for‑like basis.

Competitive intelligence & supplier scorecards: In‑depth profiles, capability assessments, and a supplier decision matrix focused on compliance readiness, modularity, service footprint, and software ecosystems.

Go‑to‑market frameworks: Regional execution playbooks, channel segmentation strategies, and partner selection criteria for vendors and resellers looking to accelerate adoption in priority markets.

M&A and partnership roadmaps: Identification of bolt‑on targets (calibration networks, software validation houses) and partnership archetypes that de‑risk entry into service‑heavy business models.

Standards and enforcement: The revised USP chapters and reinforced pharmacopoeial requirements have reframed repeatability and minimum sample weight definitions toward site‑specific metrics. Regulatory agencies have signaled strict adherence beginning in 2026, making documented traceability (ISO/IEC 17025) and internationally accepted uncertainty estimation methods (e.g., EURAMET/ASTM approaches) non‑negotiable.

Platformization and software: Buyers reward modular platforms that reduce validation time and enable remote monitoring. Connectivity, secure data handling, and audit-ready qualification workflows are now procurement differentiators, not optional extras.

Service as a moat: The frequency and rigor of calibration and validation have risen, creating a durable service revenue stream and an OPEX liability for buyers. Vendors with scale in calibration networks or strong channel partners are positioned to convert compliance needs into recurring contracts.

Concentration and competition: With the top tier holding a clear share of the market, mid‑tier players are either doubling down on niche technical differentiation (static control, moisture analysis) or moving upmarket via compliance‑focused product enhancements.

Sartorius (Göttingen, Germany): Emphasizes configurable, pharmaceutical‑grade modular balances that integrate qualification workflows and compliance interfaces. Recent product updates and alignment to new pharmacopeial requirements position them as a go‑to supplier for regulated enterprises prioritizing out‑of‑the‑box compliance.

Mettler‑Toledo (Columbus, Ohio, USA): Continues to invest in sensor technology and connectivity across its analytical series, consolidating legacy portfolios into modernized lines that emphasize internal adjustment, electromagnetic force compensation, and regulatory support — a classic defender strategy focused on enterprise requirements.

OHAUS Corporation (Pine Brook, New Jersey, USA): Competes on operational ergonomics and lab productivity features (motorized leveling, touchless sensors, ionization). Its value proposition centers on speed, throughput, and lower total validation time for high‑volume labs.

RADWAG (Poland): Leverages technical awards and specialized products (including moisture analyzers) to build credibility in precision niches; industry recognition enhances brand trust in regions valuing independent validation.

A&D Company (Tokyo, Japan): Differentiates on precision hardware and static control, appealing to demanding R&D and analytical environments where environmental controls dictate measurement integrity.

Market concentration metrics: The top three and top five vendors command substantial cumulative shares, creating a competitive environment where scale, service coverage, and regulatory support matter as much as baseline accuracy.

Immediate compliance triage (0–90 days): Conduct a rapid installed‑base audit keyed to site‑specific repeatability requirements; prioritize high‑risk labs for re‑qualification and identify units nearing end‑of‑life for phased replacement.

Procurement strategy (90–180 days): Shift RFPs to value‑based scoring that weights compliance readiness, integrated qualification workflows, and lifecycle service SLAs. Use PW Consulting’s TCO templates to harmonize supplier proposals.

Service & supplier partnerships: Build or acquire calibration capacity tied to ISO/IEC 17025 accreditation, or lock long‑term service agreements with top suppliers to secure priority calibration slots and predictable OPEX.

R&D/product roadmap: For OEMs, prioritize modular designs with configurable compliance bundles and secure connectivity. For buyers, insist on demonstrable audit trails and factory‑supported qualification packages.

M&A and strategic investments: Target calibration networks, software validation specialists, and niche instrument makers to expand recurring revenue and accelerate compliance offerings.

Our Lab Balance Market report translates the market’s macro trajectory (historical growth to USD 2.36 Billion in 2025 and a forecast to ~USD 3.25 Billion by 2032 at a 4.7% CAGR) into decision‑ready artifacts: validated models, procurement scorecards, compliance playbooks, and deal‑ready M&A targets. The report’s competitive intelligence synthesizes vendor strategies and recent product and regulatory events to illuminate where differentiation, price pressure, and service opportunity will emerge over the next 18 months.

Pretending full disclosure in a trailer undermines the decision process — so we’ve intentionally withheld the granular segmentation and proprietary datasets that buyers and investors need to finalize bids and valuations. Access to those detailed tables, regional breakouts, and application‑level forecasts is available through the full Lab Balance Market report and associated advisory sessions, where our analysts will walk your team through scenario modeling customized to your asset base, regulatory exposure, and commercial priorities.

Schedule a briefing with PW Consulting to review the full dataset and receive a tailored 90‑day action plan for your organization’s lab balance estate. The briefing will include an interactive TCO model, supplier shortlists aligned to your regulatory footprint, and playbooks for procurement and validation.

For detailed analysis of this topic, please visit the official page:Lab Balance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com