International Courier Services in Hyderabad for Reliable Global Shipping

Other |

2026-06-05 09:46:28

As companies position for 2026 and beyond, the USB car chargers market presents a mix of steady expansion, accelerating technology-led differentiation, and structural fragmentation that together create both predictable returns and selective high-value opportunities. This preview synthesizes macro-level market dynamics and executive-level recommendations drawn from PW Consulting’s latest market study (base year 2025). It is intended as a strategic primer: rigorous enough to inform boardroom decisions, but intentionally selective in detailed segment-level data to guide you to the full report for tactical execution.

USB Car Chargers Market

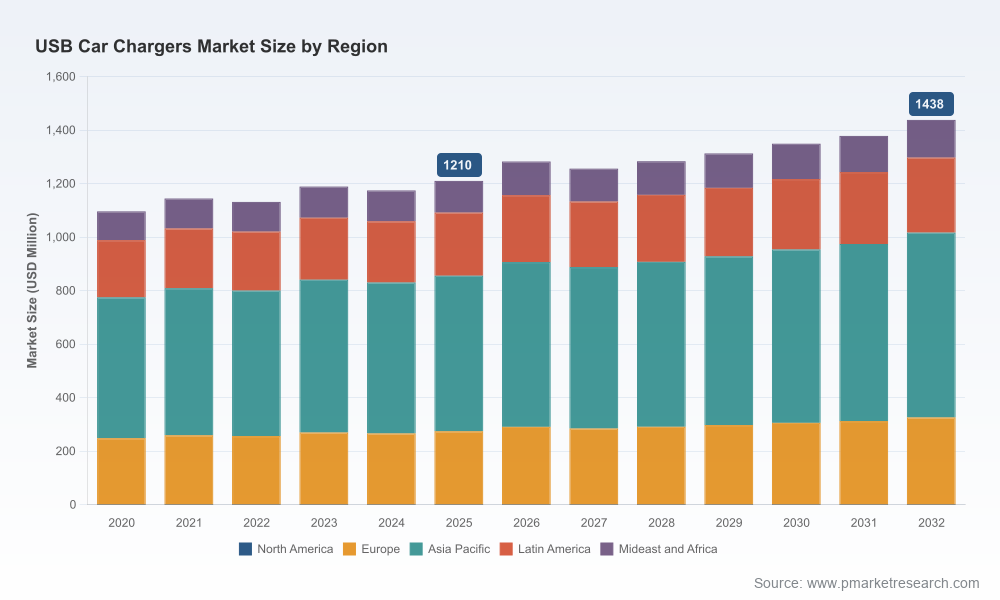

Scale and trajectory: The global USB car chargers market is a billion-dollar class industry. After modest volatility during 2020–2025, total market revenue sits in the low‑USD 1.2 billion range for 2025. Under a base forecast (2026–2032) the market is expected to expand at a compound annual growth rate of approximately 2.5%, reaching a mid‑teens‑hundreds of millions USD scale by 2032.

USB Car Chargers Market

Historical rhythm: The market has shown resiliency through macro cycles—recovering quickly after pandemic-related distortions and stabilizing into a steady growth corridor. That predictability is useful for capex planning and inventory cadence.

USB Car Chargers Market

Competitive structure: Concentration is low—top three players account for a single‑digit share and the top five remain well below one‑quarter of the market—signalling fragmentation, intense price competition in commodity cohorts, and abundant space for niche differentiation.

Portfolio prioritization: With steady overall growth, 2026 is the year to rationalize product portfolios: cut low-margin SKU proliferation, invest selectively in differentiated propositions (higher wattage, integrated cables, GaN), and accelerate SKUs that align with ecosystem trends.

R&D and tech bets: Small annual growth hides pockets of faster innovation-led traction. Executives should shift R&D budgets from incremental cost‑down projects to features that command premium mindshare—multi‑port power delivery, retractable integrated cable designs, high-efficiency GaN conversion, and embedded safety/thermal management.

Channel and distribution: The fragmented vendor landscape underscores the importance of channel leverage. Consider exclusive partnerships with Tier‑1 accessory distributors, bespoke OEM programs for vehicle manufacturers, and data-driven assortment optimization in e‑commerce storefronts.

M&A and partnerships: Low concentration and many small to mid‑sized innovators create attractive roll‑up opportunities for players seeking scale. Strategic M&A can accelerate capability acquisition (e.g., patent portfolios, proprietary retractable mechanisms, or regional distribution networks) at valuations that remain disciplined.

USB Type‑C migration and standards convergence: Regulatory and ecosystem shifts—most notably recent EU directives standardizing USB‑C across device classes—are accelerating adoption of Type‑C interfaces across accessories. For car charger suppliers, this raises both a demand opportunity and a compatibility imperative: product roadmaps must prioritize PD (Power Delivery) profiles, cable certification, and backward‑compatibility strategies.

Power and integration: End users increasingly expect higher wattage, faster charge cycles, and integrated cable convenience. The arrival of compact high‑wattage products (e.g., new retractable 75W and 160+W solutions) demonstrates a market that rewards compact engineering and thermal design excellence.

Cost and component dynamics: Semiconductor availability, GaN adoption, and cable component sourcing continue to shape BOM economics. Margins can improve materially for firms who secure long‑term supplier agreements and invest in GaN integration expertise.

Aftermarket vs. OEM tension: Passenger vehicle electrification and longer vehicle life cycles raise demand for aftermarket upgrades, but OEM partnerships deliver scale and product validation. Winners will operate hybrid go‑to‑market models—selling both direct to consumers and through vehicle manufacturers.

The market is populated by a mixture of consumer electronics incumbents, mobile‑accessory specialists, and niche hardware innovators. The companies profiled in our study illustrate distinct strategic postures:

Anker (Shenzhen): A technology‑led challenger focused on premium performance and product engineering. Recent launches that integrate compact, high‑wattage designs with user‑friendly form factors indicate a push toward premium, higher‑margin offerings and stronger direct‑to‑consumer channels.

Baseus (Shenzhen): Fast product cycle and catalogue breadth are Baseus’ hallmarks. Notable introductions aimed at European markets demonstrate their dual strategy: rapid product innovation combined with aggressive regional market entries.

Aukey (Hong Kong): Offers broad accessory portfolios and leverages scalable manufacturing. Their value play and distribution relationships keep them competitive in mass channels.

Belkin (USA): Channel depth and certification credentials are Belkin’s competitive assets. They are positioned to win OEM and retail listings where brand assurance and compliance matter most.

Scosche (USA): A specialist in vehicle and in‑car accessories; strong product integration with automotive styling and user ergonomics differentiates them in vehicle‑centric segments.

Spigen (USA): Design and brand affinity—especially among premium mobile users—allow Spigen to command price differentials for aesthetically integrated accessories.

Union Power (USA): Smaller, more specialized players remain important sources of niche intellectual property and manufacturing flexibility that larger players may acquire.

Collectively, these vendors illustrate common strategic plays: rapid product updates, focus on Type‑C and high‑power solutions, and a mix of direct and wholesale distribution. Recent new product introductions underlie the trend: compact 75W integrated designs and multi‑cable retractable high‑wattage chargers have already reached the market, signaling where consumer expectations are moving.

Segmentation and demand analytics: Granular demand models across port types, connector technologies, and end‑use channels—modeled with scenario variants and sensitivity tests to inform SKU rationalization and inventory policy.

Price and margin benchmarks: SKU‑level pricing ladders, BOM breakdowns, supplier cost estimates, and margin waterfall to guide pricing strategies and product cost optimization.

Competitive intelligence: Strategic profiles, product maps, patent landscape summaries, and go‑to‑market playbooks for incumbent and challenger brands.

Regulatory and standards impact analysis: Assessment of current and forthcoming regulatory shifts (including EU standardization moves) and step‑by‑step compliance playbooks for product certification.

Channel and commercialization toolkit: Retail assortment recommendations, e‑commerce conversion levers, and templates for OEM partnership negotiation (including sample commercial terms and margin sharing models).

M&A and investment screen: A prioritized list of acquisition archetypes, valuation heuristics, integration risk checklists, and post‑acquisition value capture roadmaps.

Quarter 1: Conduct SKU profit‑pool review and immediately retire or reprice the lowest‑return SKUs. Freeze non‑strategic new product launches.

Quarter 2: Accelerate development on 1–2 Type‑C PD products with GaN and robust thermal design, and initiate supplier negotiations for cost stability.

Quarter 3: Pilot an OEM partnership or a targeted retail exclusive to test premium positioning and scale distribution without broad SKU proliferation.

Quarter 4: Reassess M&A opportunities and finalize integration playbooks for identified bolt‑on targets.

For executives making allocation choices in 2026, the optimal approach is selective investment combined with disciplined portfolio pruning. Back engineering and product design capabilities that yield perceptible user benefits (higher sustained wattage, safer thermal performance, cable integration that reduces friction) rather than competing on commodity price alone. Leverage partnerships for distribution scale, and treat standards/regulatory shifts not as compliance costs but as market‑opening events that raise the barriers to undifferentiated competitors.

This preview is intended to orient strategic decision‑making. The full PW Consulting USB Car Chargers Market report contains the segment‑level forecasts, tactical playbooks, and downloadable datasheets you will need to execute on the recommendations above. For access to deeper tables, scenario workups, and supplier matrices, please visit our report page and request the complete dataset and executive brief.

For detailed analysis of this topic, please visit the official page:USB Car Chargers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com