Кошелек MetaMask - основные достоинства и особенности

Other |

2026-01-31 07:29:25

As healthcare systems navigate increasing demand for durable vascular reconstruction solutions, the man-made vascular graft market has entered a phase of steady, structurally-driven expansion. PW Consulting’s latest market study uses 2025 as the base year, traces industry dynamics across 2020–2025, and projects performance through 2032. The market expanded meaningfully during the review period and — at a modeled compound annual growth rate (CAGR) of 5.5% through 2026–2032 — is forecast to continue growing as device innovation, regulatory developments, and shifting reimbursement economics reshape provider choices and commercial models.

Man-made Vascular Graft Market

Strategic timing: 2026 is a pivotal year for portfolio rationalization and go-to-market strategy refinement. With a clear multi-year growth trajectory, executives must align R&D, manufacturing scale-up, and market access efforts to capture landing zones where margin and adoption converge.

Man-made Vascular Graft Market

Capital allocation: Moderate, predictable market expansion favors staged investment strategies over all-or-nothing bets. Companies can structure tranche-based R&D and commercial investments to de-risk launches while retaining upside capture as clinical evidence accrues.

Man-made Vascular Graft Market

Regulatory arbitrage and access: Recent clearances, approvals, and regulatory enforcement actions highlight that regulatory posture and post-market compliance capabilities are now core strategic assets — not just operational functions.

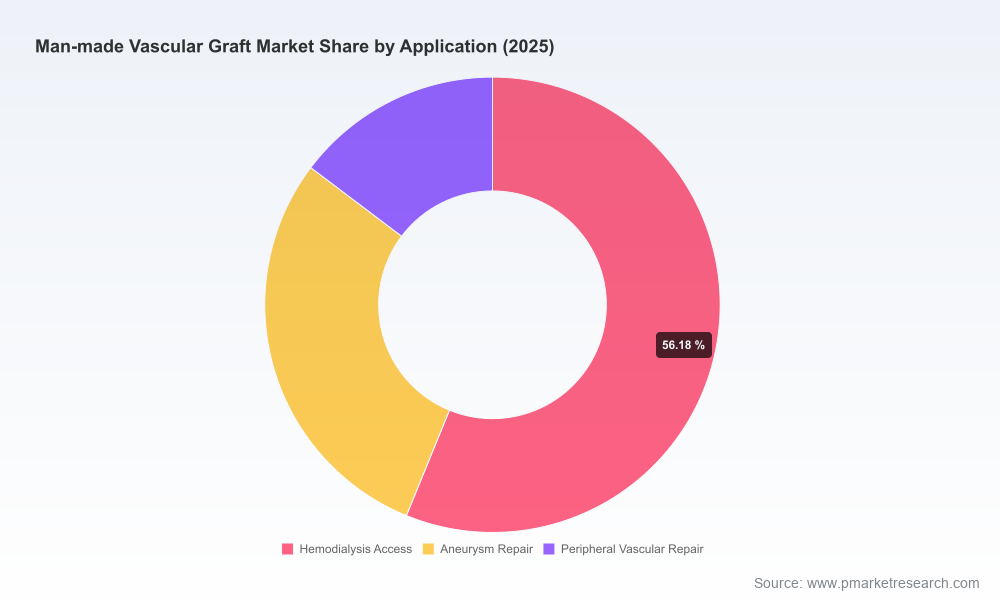

Following measured expansion from 2020 through 2025, the market reached a larger base in 2025 and is projected to expand further to a materially larger size by 2032 under the study’s forecast assumptions. That growth is driven by demographics, procedural volume expansion (including vascular trauma, dialysis access and peripheral bypass procedures), and the introduction of new biologic and biosynthetic options. Competitive concentration is meaningful but not prohibitive: the top three vendors account for a majority share, and the top five further consolidate market power — a structure that supports both incumbent advantage and targeted disruption by specialist entrants.

Clinical innovation: The 2024–2026 window has been notable for product refinements and next-generation grafts — including heparin-bonded ePTFE linings for improved patency and tissue-engineered acellular vessels for acute indications. These innovations change clinical decision trees and the value proposition presented to vascular surgeons and interventionalists.

Regulation and compliance: Regulatory outcomes have immediate commercial implications. Recent clearances and approvals validate novel materials and indications, while enforcement actions against sterilization and quality systems underscore the operational risks of scale-up. Organizations must treat regulatory and quality functions as forward-looking market enablers.

Reimbursement dynamics: The economics around complex vascular repair are significant. Recent publicized reimbursement data for extremity arterial injury repair and related infection management reinforce that payer recognition of high-cost care episodes can materially influence product adoption and hospital purchasing decisions.

Clinical evidence and adoption cadence: Early approvals and IDE expansions have created demand signals, but broad adoption will hinge on head-to-head evidence, real-world registry outcomes, and procedural workflow compatibility — factors that lengthen the commercial runway for many entrants.

Clinical program expansions: Notable IDE and trial enlargements during 2024–2025 have broadened clinical exposure for novel systems designed for complex aortic and peripheral indications — accelerating data accumulation and shaping referral patterns.

Regulatory wins: Targeted clearances for controlled-expansion graft systems and heparin-bonded linings have extended the clinical utility of established platforms, creating incremental competitive pressure on legacy devices.

First-in-class approvals: The arrival of acellular tissue-engineered vessels for specific trauma indications represents a material inflection for biologic alternatives to synthetic conduits, with implications for supply chain, sterilization, and commercial models.

Quality and compliance risks: Enforcement notices tied to sterilization validation and quality systems serve as immediate reminders that product issues can rapidly erode stakeholder trust and market access.

The market is populated by established medical technology firms with broad cardiovascular portfolios and specialist players focusing on niche biologic or hybrid grafts. Understanding capability differentials across product engineering, regulatory execution, and clinical evidence generation is critical to anticipating competitive moves.

Large diversified medtech players — with deep channels into hospitals and integrated supply chains — are positioned to extend legacy product lines into adjacent segments, leveraging clinical relationships and scale economies to defend share.

Specialist innovators and tissue-engineering firms are emerging as credible alternatives where autologous conduits are not feasible; their commercial success will rest on payer acceptance and procedural simplicity.

Strategic partnerships — between graft innovators, device manufacturers, and institutions running high-volume vascular programs — will be increasingly important for building real-world evidence and facilitating adoption in complex cases.

Market-leading material specialists continue to invest in heparin-bonded and controlled-expansion technologies that address immediate clinical pain points such as thrombosis and cannulation timing.

Global medtech firms with polyester and ePTFE portfolios focus on incremental product breadth (size ranges, handling profiles) and on commercial execution in high-volume geographies.

Newer biologics and biosynthetic entrants emphasize differentiated clinical pathways (e.g., trauma, dialysis access) and will test commercial models that blend capital and disposable economics.

Segmented investment strategy: Prioritize investments where technology advantage intersects with compelling margin potential and a clear pathway to reimbursement. Use staged funding tied to clinical milestones and reimbursement decisions to preserve optionality.

Regulatory and quality as strategic assets: Elevate regulatory planning and post-market surveillance capabilities into the core of product planning. Anticipate and budget for compliance investments upfront to reduce time-to-market risk and downstream enforcement exposure.

Evidence-generation blueprints: Align trials and registries with payer evidence requirements, not just FDA endpoints. Early diálogo with payers and health systems will shorten commercialization cycles and improve pricing outcomes.

Go-to-market choreography: Combine surgeon champions, specialty distributors, and hospital system procurement strategies to accelerate adoption. For biologic offerings, create implementation bundles that address OR workflow, sterilization, and inventory constraints.

M&A and partnership playbook: For companies that lack either scale or differentiated IP, targeted M&A or licensing can be the quickest route to market presence — particularly where incumbents demonstrate capacity constraints or regulatory burden.

A rigorous baseline and forecast model (2020–2032) that quantifies market growth drivers across macro and micro lenses, with sensitivity scenarios to stress-test strategic plans.

Actionable go-to-market guidance, including distribution archetypes, hospital procurement levers, and surgeon adoption playbooks tailored for distinct technology classes.

Regulatory mapping and compliance risk assessment that frames approval timelines, inspection risk, and post-market commitments — directly tied to commercial planning calendars.

Competitive benchmarking, consolidating capabilities across engineering, clinical evidence, and commercialization. This includes profiles of major incumbents and challenger innovators, plus tactical growth options (licensing, partnerships, M&A).

Reimbursement and health-economics synthesis that connects per-procedure economics to hospital purchasing priorities and payer levers — enabling pricing and contracting strategies.

Implementation templates and KPI dashboards that management teams can adapt for 90-, 180-, and 365-day launch milestones.

Run a portfolio decision day using our forecast scenarios to reallocate R&D and commercial resources against high-probability adoption pathways.

Initiate payer engagement pilots aligned to your preferred clinical indication to test reimbursement pathways before full-scale launch.

Commission a regulatory-gap assessment to ensure sterilization and quality systems meet the scrutiny leveled at peers and rivals — avoiding the disruptive impact of enforcement actions.

By 2026, the man-made vascular graft market presents a clear but nuanced opportunity: steady growth supports investment, yet clinical complexity, regulatory scrutiny, and payer expectations demand disciplined strategy. Incumbents can defend and extend positions through iterative innovation and execution excellence; challengers must solve for evidence and reimbursement rapidly or partner to scale. PW Consulting’s study synthesizes the macro trajectory, regulatory inflection points, commercial levers, and competitive options you need to make those trade-offs confidently.

This article highlights the strategic contours and practical imperatives derived from our in-depth study. For the full data tables, granular segment analysis, provider-level pricing benchmarks, and executable playbooks that underpin these conclusions, please consult the complete PW Consulting Man-made Vascular Graft Market report.

For detailed analysis of this topic, please visit the official page:Man-made Vascular Graft Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com