Negative Pressure Operating Room Industry Report: Opportunities & Regional Analysis

Other |

2026-02-26 12:57:01

PW Consulting’s Commercial Small Batteries Market report (base year 2025; historical coverage 2020–2025; forecast period 2026–2032) delivers a focused, decision-ready picture for executives planning capital, procurement and product strategy in 2026. The global market reached approximately USD 14,580.0 Million in 2025 and is modeled to expand at a compound annual growth rate (CAGR) of 6.79% across the 2026–2032 forecast window, reaching roughly USD 23,107.7 Million by 2032. Market concentration is moderate: the top three suppliers account for just over 42% of market value, while the top five approach a near-59% share — a structure that creates both defensive positions for incumbents and fertile ground for fast-moving challengers and niche specialists.

Commercial Small Batteries Market

Cost pressure and raw-material volatility are driving immediate procurement and price-risk decisions across OEMs and distributors.

Commercial Small Batteries Market

Tighter safety and labeling rules in major jurisdictions require operational changes to product design, packaging, and extended producer responsibility programs.

Commercial Small Batteries Market

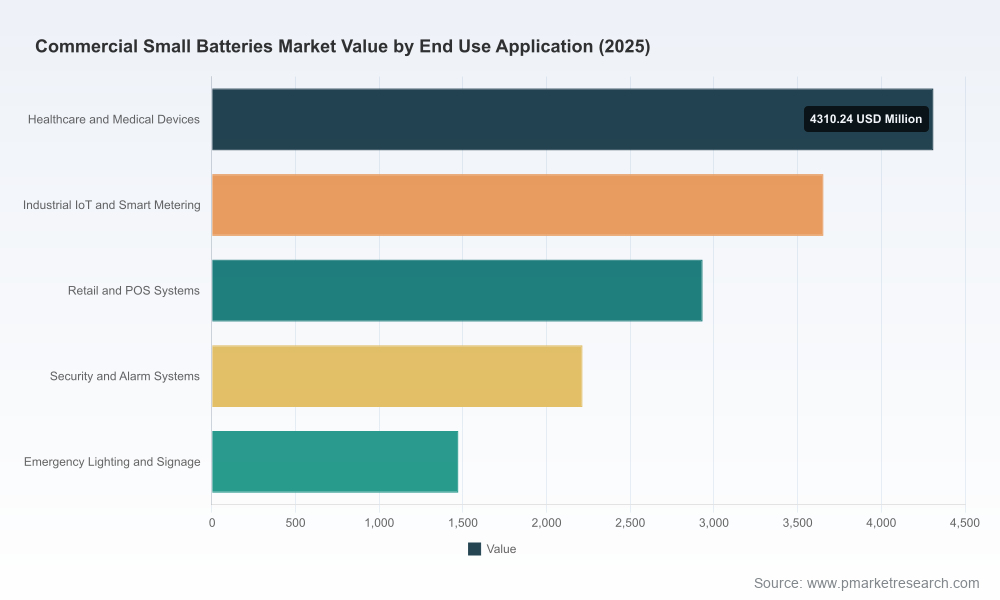

Technology choice (chemistry mix, form factors) is now a strategic lever — affecting lifetime cost, regulatory compliance and route-to-market for commercial applications such as healthcare devices, IoT endpoints and backup power.

Consolidation signals and targeted product innovations open discrete M&A and partnership windows for companies seeking scale or capability add-ons.

Granular market-sizing and validated forecasting (2020–2032) with scenario modules that stress-test commodity price swings, regulatory shock events and adoption curves.

Commodity and cost model: a transparent, sensitivity-ready model linking lithium carbonate and other raw-material price paths to manufacturing cost and margin outcomes.

Regulatory impact playbook: compliance checklists and retrofitting guidance for new EU Batteries Regulation requirements, UL and IEC safety standards, and country-level packaging mandates.

Competitive benchmarking and capability maps: bespoke scorecards for manufacturers, contract manufacturers and distributors covering product breadth, manufacturing footprint, quality certifications and channel coverage.

Go-to-market and commercial playbooks: segmentation-led pricing strategies, route-to-market matrices for healthcare/medical, industrial IoT and other commercial verticals, and channel partnership templates.

M&A and partnership pipeline: screened target lists, valuation heuristics and integration risk matrices tailored to acquirers seeking fast capacity, tech IP or geographic reach.

Operational playbooks for procurement and inventory: hedging strategies, supplier split recommendations and contract-clauses to mitigate raw-material and logistics shocks.

Executive briefings, slide decks and dataset extracts optimized for board presentation and commercial planning cycles.

The commercial small-battery space is populated by diversified global manufacturers and focused specialists. Incumbent brand players and component specialists coexist: household names with broad portfolios compete alongside companies emphasizing micro-form factors, hearing-aid cells or sealed lead-acid backup formats. Notable firms covered in our analysis include Energizer Holdings, Duracell, Panasonic, VARTA AG, Maxell, GP Batteries, EnerSys, GS Yuasa, Power-Sonic, Murata, Renata and Toshiba. Each brings differentiated strengths — global distribution and consumer brand equity, engineering depth in coin/button cells, expertise in VRLA/backup systems, or tight vertical integration with electronics OEMs.

Key strategic notes from our benchmarking:

Energizer and Duracell retain strong brand and channel positions that protect premium pricing in multiple commercial segments; Duracell’s recent child-safety bitter coating innovation underscores how product-level safety features can be monetized and used defensively.

Japan- and Germany-headquartered suppliers (e.g., Panasonic, Murata, VARTA, Maxell) continue to invest in precision chemistries and micro-battery manufacturing excellence — a competitive advantage for medical and precision-instrument applications.

Specialist industrial vendors (EnerSys, Power-Sonic, GS Yuasa) dominate standby and UPS niches where form-factor and reliability are sale determinants — these firms surface as natural partners for enterprise and infrastructure OEMs.

Regional OEMs and Asian contract manufacturers provide low-cost scale and rapid capacity expansion, keeping margins under pressure and enabling quick response to short-term demand spikes.

Raw-material volatility: Lithium carbonate prices rebounded markedly in 2025 and are expected to remain in a wide range through 2026. Procurement teams must assume cost swings that materially affect small lithium-cell economics and plan contracts and hedges accordingly.

Regulatory tightening: Newer standards and regulations — including jurisdictional implementations of the EU Batteries Regulation, UL 4200A safety guidance and updated IEC standards for button cells — are increasing compliance costs and introducing specific testing and labeling requirements. These are not merely administrative: they affect product design, packaging and field-liability exposure.

Product-safety focus: Ingestion and physiological-hazard risks associated with coin and button cells are driving packaging innovations and safety-treated chemistries. Expect higher compliance and product-liability visibility in commercial procurements and tender specifications.

Innovation and capacity shifts: Public disclosures and trade-show activity in 2025–2026 signal both new entrants and incumbents expanding into adjacent small-battery formats and HEV/pouch segments — this will alter competitive dynamics in select subsegments.

Supplier-level cost pass-throughs: Monitor which manufacturers absorb raw-material swings versus those who pursue pass-through clauses; this will determine short-term margin leadership.

Regulatory enforcement timing: Watch the rollout cadence for EU labeling rules and ingestion-safety standards; procurement cycles should include compliance verification milestones.

Product-safety differentiation: Safety-treated coin cells and child-safe packaging will become minimum commercial requirements in healthcare and consumer-adjacent procurements.

Consolidation vs. specialization: Active M&A in targeted niches (micro-batteries, medical-grade cells, backup systems) will create acquisition opportunities for buyers seeking capability rather than scale alone.

Hedge raw-material exposure: Lock in multi-supplier agreements and consider financial hedges for lithium-related inputs; test contract language for pass-through triggers and force majeure clarity.

Diversify chemistry and supply footprints: Where feasible, pursue multi-chemistry product strategies (primary lithium, alkaline, nickel variants) to balance cost, regulatory and lifecycle trade-offs.

Prioritize compliance-driven engineering: Invest early in design changes required by new safety and labeling standards to avoid rushed redesigns and costly recalls.

Targeted M&A and partnerships: Use the moderate top-end concentration to scout bolt-on targets that add niche technical know-how, medical certifications or regional manufacturing capacity.

Commercial playbook updates: Update RFP templates to include safety test evidence, labeling conformity and EPR commitments; reprice product lines to reflect embedded compliance costs.

CEOs and CPOs will use the commodity scenarios and supplier scorecards to set 12–24 month procurement strategies and contract terms.

Product and engineering leads will leverage regulatory impact mapping and test-plan templates to prioritize design cycles for medical and IoT product lines.

Corporate development teams will apply the M&A pipeline and valuation heuristics to screen tuck-in targets and prepare integration checklists.

Compliance and legal teams will adopt the standards matrix and labeling checklists to close gaps ahead of enforcement milestones.

PW Consulting’s Commercial Small Batteries Market report is designed as a working tool for 2026 strategic planning — combining validated macro forecasts, scenario-ready cost models, and transaction-oriented competitive intelligence. This briefing surfaces the essential signals: a growth trajectory underpinned by steady demand, material-driven cost risk, tighter safety and regulatory requirements, and a competitive landscape that rewards both brand strength and engineering specialization.

To preserve the tactical value of our segmentation models, detailed regional and end-use splits, and company-level scorecards are reserved for the full report and accompanying datasets. For complete access to the segmented revenues, downloadable tables, supplier scorecards and bespoke consulting options, visit PW Consulting’s Commercial Small Batteries Market report page or contact your PW account lead to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Commercial Small Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com